8/9/25 Prices

The Aussie dollar is stronger against all the major currencies this morning bar the Yen and Euro, which it was only fractionally stronger against. The move in the dollar puts a lot of pressure on the conversion of international grain prices, cash and futures.

For the conversion of SRWW futures out of Chicago the move in the dollar is worth about -AUD$ 1.74/t, more than the -AUD$0.70 / tonne the actual futures move was worth.

This rolls across most grades and grains, the higher the value of the commodity the greater the impact the move in the AUD will have. Chickpeas for instance gave back a bunch in native currency last night, closing 55Rs/Q lower. On a flat AUD / Rs this would have been equivalent to a decline in the conversion of roughly AUD$8.35/t, including the drop in the AUD into the conversion results in a day to day change closer to -AUD$14.09 / tonne, an addition AUD$5.74/t of negativity thanks to currency.

I’m no currency expert but all I’m reading this morning is accrediting the move to technical trade. An oversold AUD finding support from the punters. There was better than expected growth Q2 GDP, mainly attributed to the housing market, we all have a view on that right now, but a 1.8% year on year growth number can’t be considered that bullish surely. The devil is in the detail, as usual, household savings falling from 5.2% to 4.2%, everything still costs too much.

That’s enough of the real world. Canadian durum producers continue to see lower prices, avg bids out of SE Sask average were back CAD$7.77/tonne this week. The fall coinciding nicely with some good harvest weather. French values also closed the week AUD$7.00/t also taking daily currency moves into account. Across SE Saskatchewan, 1CWAD13 durum is still pulling a healthy CAD$41.70/t (AUD$46) premium over 1CWRS13.5 spring wheat. Not all is perfect for the Canadian durum product though. There are a lot of green tillers after recent rain and early heads are weathered in many locations.

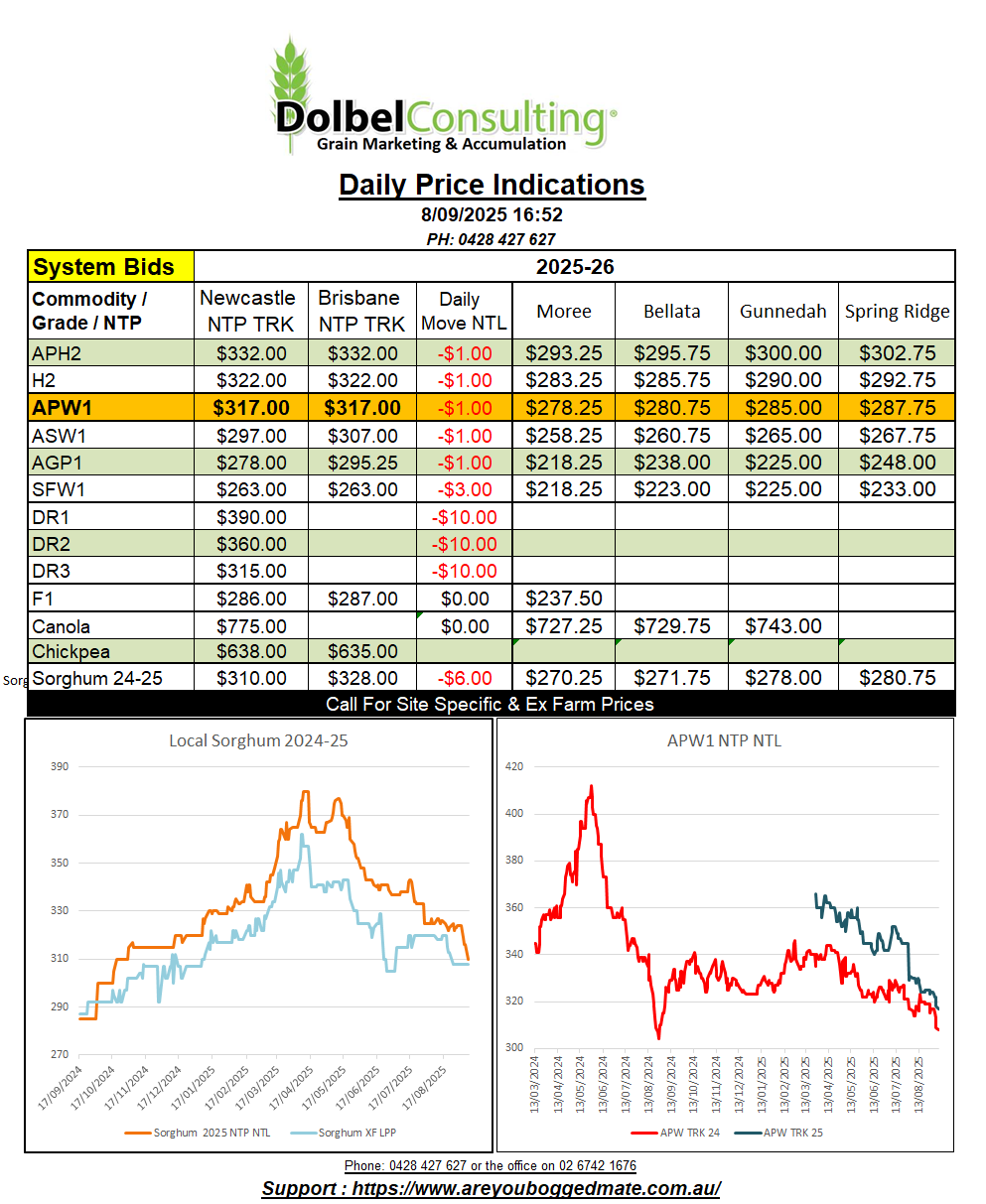

Local new crop wheat prices moved lower across the board, all grades slipping more than either local or international futures, and more than international cash values did, the night prior. This saw some basis erosion for APW over Chicago SRWW futures. The trade continue to talk grains lower, “the world is awash with wheat”, “Russian exports are slow, meaning competition for Aussie wheat later in the season”, “US wheat is heaps cheaper”, “local demand is poor”. All the usual negative cliches are there, and rightly sow I guess, but the market has all this factored in already.

Has there been a time in this marketing year that a grower could look back at and say “wow I wish I had of locked some wheat in then”, I hope not. Yes the high in APW track values was $48 ago, but at $366 NTP Newcastle, $334 delivered Gunnedah silo, roughly $320 ex farm, that high was no better than what many had just sold SFW1 for just a few months earlier. Were new crop multi grade spread worth locking in, when you could, not really. Yes $48 is a bitter pill to swallow, but as my accountant once told me “it’s not a loss until it’s realised” in other words unless you sell now it’s not a $48 loss. The only thing selling now, or lower, does is lock in that loss and lock out the potential to sell higher. Unless you sell and buy a call, you have no upside potential.

From a consumers perspective they are looking at great supply, again, and low prices, their favourite combination. The only way a grower can change this is to limit supply, short term by holding grain out of the market, longer term by sowing less of it. Still keen to see a few more acre reports too.

Just remember it’s September, the end of the Northern Hemisphere harvest, the world is awash with wheat, for now. The local long term weather forecast is volatile. My clunky old analogue rainfall prediction model agrees, the chances of a wet harvest is higher than average. it’s predicting a 75% chance of a wet September 80mm, October 75mm and December 95mm. A prediction I hope is not 100% accurate.