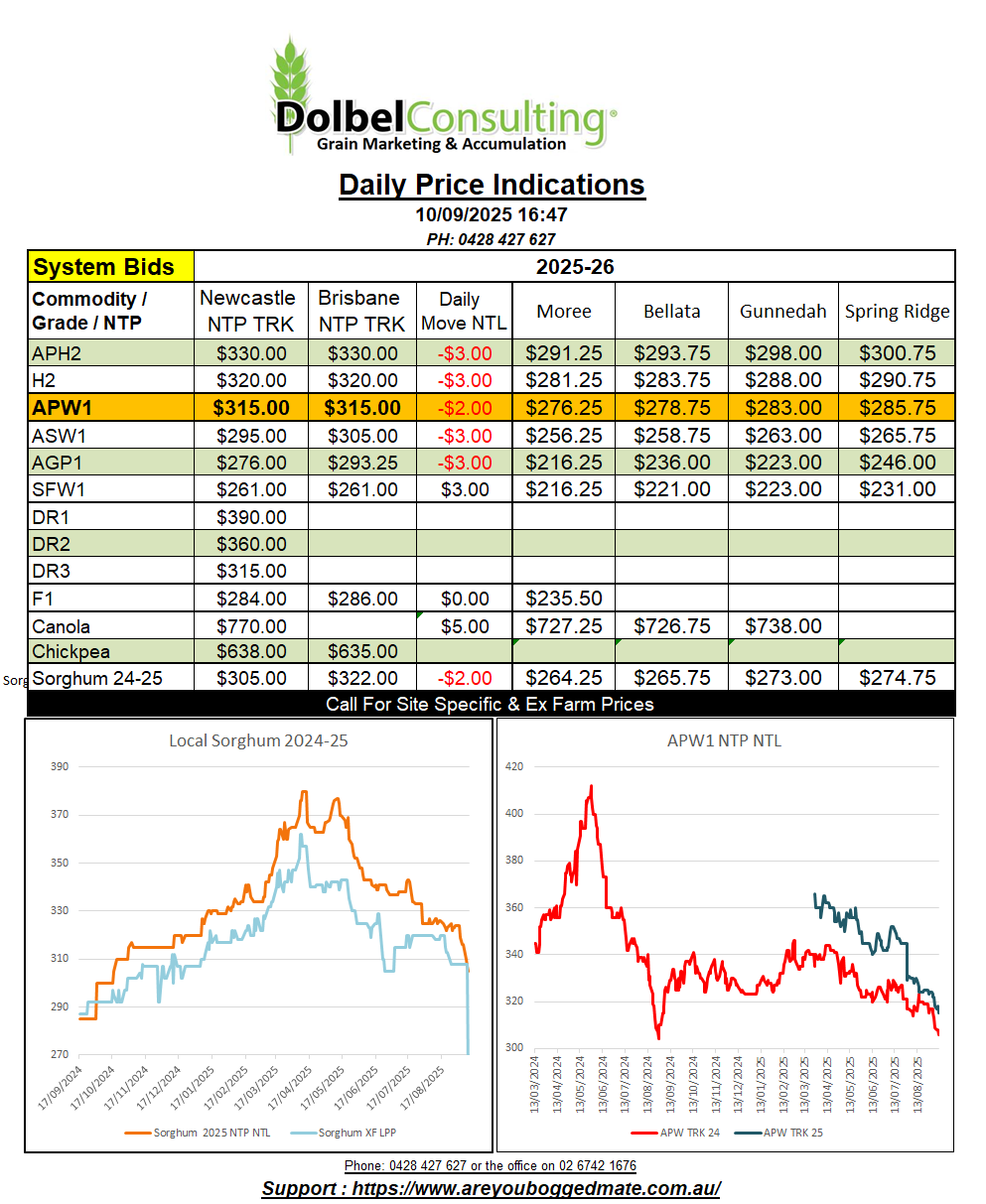

10/9/25 Prices

The AUD was a smidge lower in overnight trade. This did help counter some weaker numbers from the futures markets and other major grain exporters, but it may not stop local bids here from drifting a little lower today. Mind you the risk of a frost across a lot of the eastern wheat belt of NSW and Victoria on Saturday morning may have a slightly positive impact on basis over the next couple of days.

International milling wheat values were mostly lower FOB origin. Black Sea values appear to have bucked that trend though. Russian wheat saw a day to day improvement in the conversion to an Asian consumer in AUD/t of roughly AUD$4.00. The Ukraine conversion was sharply higher, I’ll refrain from quoting that change in case it is a simple reporting anomaly for now.

US Pacific Northwest values are generally AUD$2.00 to AUD$4.00 lower while white wheat out of the PNW was a smidge higher. US HRWW into the Asian market continue to be roughly US$8.50 less than Australian H2 wheat. Asian buyers should be seeing this as a huge bargain for Aussie wheat Q1 2026.

With northern hemisphere wheat harvest starting to wind up across many countries we may start to see the harvest pressure on values recede. Yes the world has produced an ample supply wheat. The international stocks to use ratio is not going to change significantly year on year, thus nor should values in US dollar terms at least. Last year we started October with the AUD at 0.6885 and finished in December at 0.6268. During that time Dec SRWW futures went from 660.5c/bu to 598.5c/bu, a fall of 62c/bu, the fall in the AUD buffering over AUD$30.00 of a AUD$33.00 fall in futures. With the SRWW contract now at 520c/bu does the US futures market have the potential for such a fall again this year, probably not. Does the AUD have the potential for a similar fall this year, also probably not. This leaves one looking at demand to trigger higher prices. One would assume at these values this shouldn’t be an issue.

Local milling wheat values were flat to firmer yesterday, while canola took a hit.

Aussie canola may have two major homes to work with this year, the EU and China. Looking at the EU first our major competition will come from the Canadians who have recently lost exports to China. Currently we see Canadian canola bid at roughly CAD$565 ex farm SE Saskatchewan. This would make its way to port and onto a boat, landing CnF France for something close to US$531 per tonne.

Looking at Aussie bids at AUD$765 Newcastle port, this canola would end up CnF France for something close to US$578. A good premium (+US$47.00) over Canadian canola. Does this indicate a potential decline in EU bids for Aussie canola.

The next major destination could be China. Using the same math against port bids to calculate a CnF China price we end up with a value of US$552 CnF China. If the Canadians are not going to be our major competition who will be. Let’s not muddy the water with oilseed substitution. Will the competition come from Ukraine. Probably not, Ukraine appear to be having a few other issues and have currently stopped rapeseed exports. Hypothetically though, Ukraine rapeseed would work out to be something close to US$618 CnF China.

The conclusion seems to point towards good support at current values but the canola market will not be immune from moves in the vegie oil complex. Pressure from both soybeans and palm oil may occur, as well as pressure from outside markets like crude oil to a lesser extent.

The punters are talking the AUD higher as the US dollar weakens further. The currency market isn’t for the faint hearted at present though. The US FED was also quoted as saying that the impact from tariffs wasn’t as bad as they had expected it to be. If this proves wrong US rates may stay higher, for longer.