29/9/25 Prices

US wheat futures gave back the previous sessions gain, as did corn. The old saying “the bulls need feeding everyday” rang true. The market continues to struggle to sustain a recovery, instead slipping backing to support levels and sustaining a flat, range bound market, very boring indeed. Do we like boring, at $400/t yes, at $250 per tonne, definitely not.

International cash values were mixed. US values out of the Pacific Northwest leading the push lower, while both French and Black Sea conversions were closer to unchanged when compared to yesterdays conversion. Paris milling wheat futures did tend to reflect the negativity of the Chicago futures market, but in general international cash values were not as caught up in the selling down as futures were.

With the removal of export duties on Argentine grains and meat exports for a short period of time, it has resulted in some seriously good sales numbers. The initial decision on Monday was to reduce export taxes to zero and that to stay in place until $7Bn of sales was generated. $7Bn was sold in 2 days and duties then reinstated. Later in the day a presidential spokesman stated export taxes would remain at zero until October 31st. The market is still waiting to see if this is correct. China jumped on the deal pretty quick and are said to have booked around 40 boat loads of Argie soybeans during the window of opportunity.

Russian FOB wheat values continue to move higher. One might assume the opposite would be the case given the recent increase in Russian production estimates by both private and government analyst. The problem appears to be the location of the increase. Spring wheat has had a cracking season, but Siberia and the main spring wheat region is a long way from the Black Sea and major export terminals or consumption points. This does lead one to consider where this additional Russian wheat should appear on an S&D table. Possibly as extra ending stocks, stocks that are not likely to see an export market.

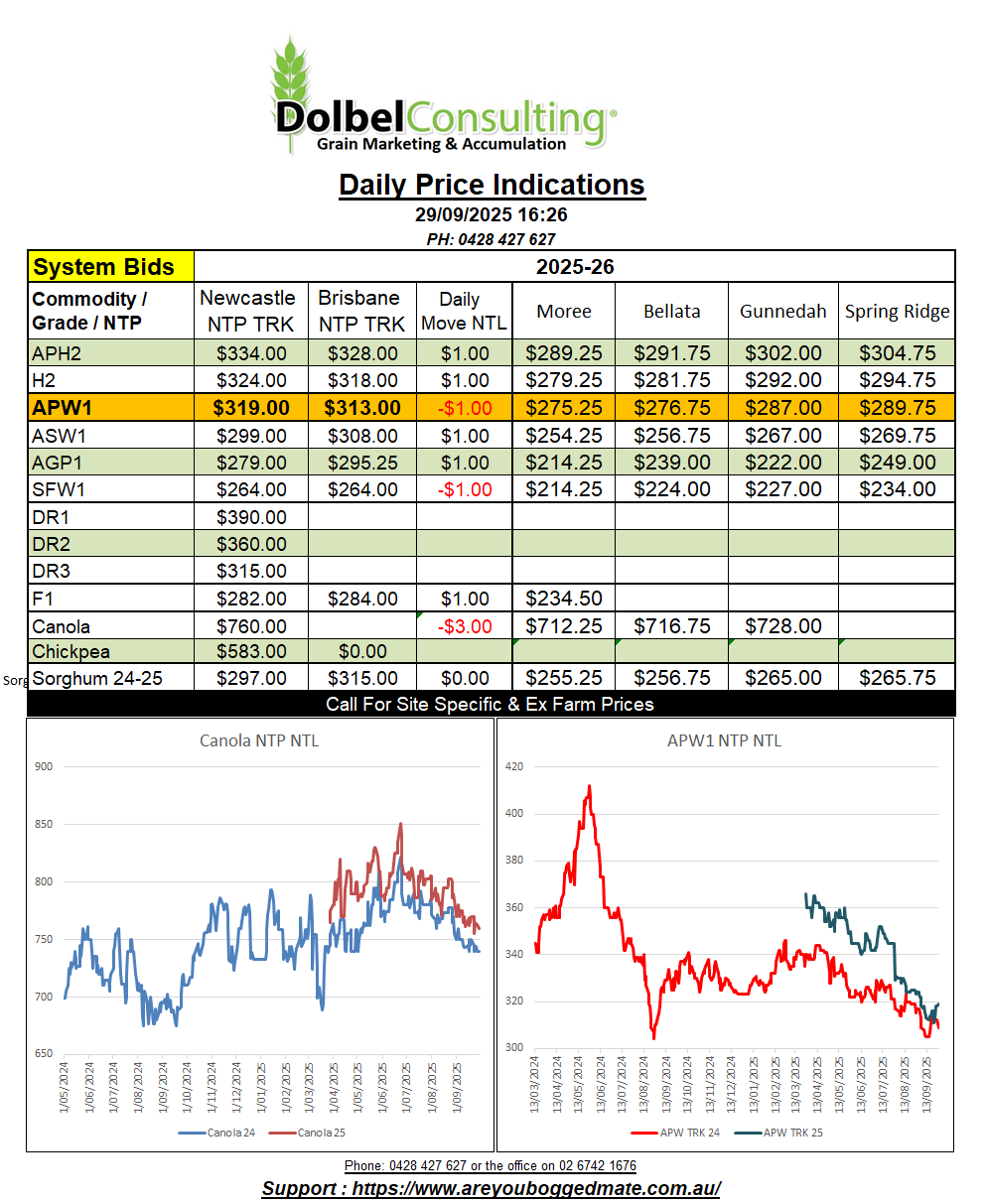

A little look at feed barley, the product otherwise known as poverty grass. According to my recent grower survey acreage on the Liverpool Plains is back significantly this year, almost 40% lower. With this in mind I can’t help but think that those who “need” barley may struggle to find it locally later in the year. Will barley still be worth nothing in July 2026, potentially yes, but there’s a lot that can happen between now and then. A good quality wheat harvest would benefit the local market greatly, from a sellers perspective.

Current pricing is not great. On the track we see BAR1 bid at roughly $281 NTP Newcastle. Site values will vary from a simple NTP less GTA deduction. For example the cash contract bid at Graincorp Quirindi is $253.50, a further $2.00 discount to NTP NTL less GTA site differential. This compares to an ASX feed barley futures contract delivered Graincorp Quirindi of just $238.17/t. Cash is a mile in front of ASX futures already. Yesterday new crop was bid at $278 delivered Caroona / Killara for Jan / Feb / March. That’s better than track or futures, but still shows a significant discount to what new crop is bid on the Downs, $302 for the same delivery window.

International barley values into the Chinese market are between US$230 and US$316 C&F China. Aussie barley from Western Australia remains the cheapest option for the Chinese, closely followed by Black Sea barley and then Argentina.

If you were to convert the current WA price C&F China, to an equivalent price delivered LPP track we come up with a number something close to $254, bang on the current system bid. Implying that current local cash barley bids are at export parity. One might expect to see the domestic market at least pay a slight premium to the export market, as they are on the Downs, but currently this may not be the case.