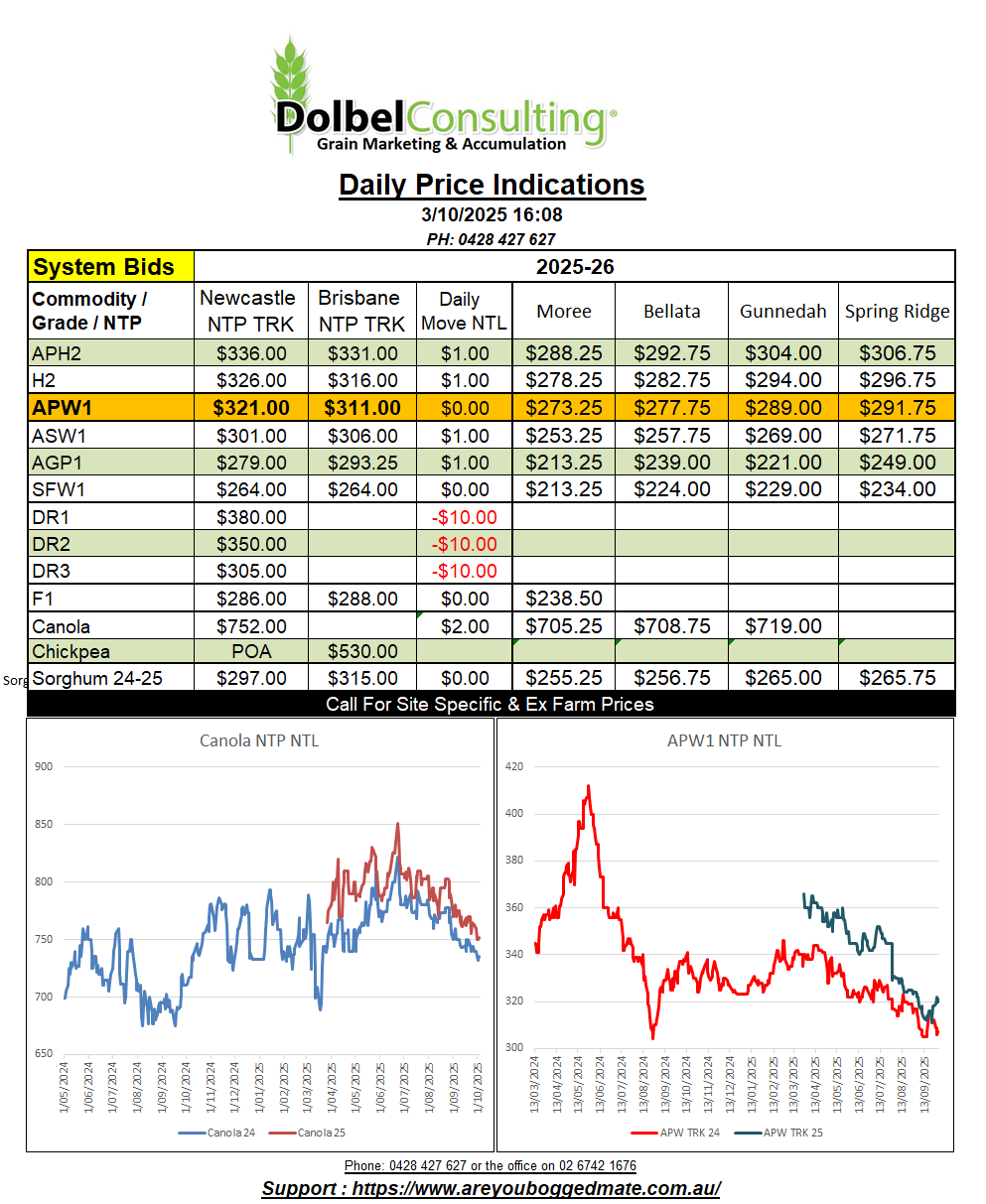

3/10/25 Prices

The US government shut down is / will eventually spill over into crucial market data services. Obviously these data services, or lack of, will have a much larger impact on Americans that the rest of the world but failure to release data that is often seen as crucial. Weekly export inspections, weekly sales, United States Dept of Ag WASDE or FAS data services, ethanol production reports, aid funding to US farmers and foreign entities, are all disrupted.

The closure also has the knock on affect for those employed by the US government and are not getting paid. This may include certain non government projects being government funded or NGO workers that are relying on government funds to exist.

Will it stop the sale of grain, no. Will it stop the export of grain from the US, no. It will have no impact on physical grain, just the reporting. Last time this happened and it dragged out for a month, it created a lot of speculation on sales and export volume. Once the data became available there were later adjustments, and accusations that data was wrong, it created volatility in the futures market.

Argentine winter crop condition remains very good. A wet winter has the current estimate for wheat production being increased to 22mt, just 400kt below the previous record set in 2021-22. WorldAgWeather.com shows much of BA saw 50 to 100mm of rain over the last two weeks, the falls also pushing west into Cordoba and Santa Fe, both major wheat production regions. The 7 day forecast calls for slightly less rain, but falls of 15-50mm are possible across much of their major wheat grower area.

Argentine summer crop sowing is being delayed in some cases but it’s early days in the summer crop window and the additional subsoil moisture is generally being seen as more beneficial than harmful at present. Argentine sorghum production is generally across the central and northern wheat production zones and has also seen very good rainfall this winter / spring.

Local markets were generally flat to firmer yesterday, apart from chickpeas which are struggling to recover from a slip lower last week. The Delhi chickpea market price remained indicated at 5801Rs/Q, roughly equivalent to AUD$991.37 / tonne, no change from Wednesday.

The weaker AUD will add roughly AUD$1.89/t to yesterdays Delhi conversion value.

Talk of the potential of import tariffs by India continue to keep the trade on edge, and the spread between Indian domestic prices and bids here in Australia comparatively high. Using a simple conversion to determine what Delhi values might be equivalent to at the Narrabri packer gives us a rough number of about AUD$652/t. Currently bids, when available, are closer to AUD$480 / tonne.

There is also speculation that due to the low prices, both Aussie and Indian 2026-27 area will decline. India is currently sowing or preparing to sow chickpeas. Indian traders have noted a decrease in projected Indian area may see a supply shortfall in Q3-4 2026. Something that may not play out in values until after the Indian harvest in March / April 2026. It’s not often we see better prices for chickpeas in the middle of the year following our harvest unless we have a drought, but if Indian area does slip and their demand stays constant, Q2-3-4 2026 values and 2027 values, may well increase above current estimates.

US futures are higher, cash values out of the US Pacific Northwest are also higher. The white wheat conversion is +AUD$5.49 / tonne compared to yesterdays conversion. Both HRWW and Spring Wheat values also improved by roughly AUD$4.30/t. Canadian spring wheat values followed US but were not as strong, closing to +AUD$3.30/t. Spreads between Canadian CWAD1 and 2 grades remains narrow as quality is an issue in some durum samples.