22/10/25 Prices

Chicago soybean futures retreated from setting a short term high, back 1.5c/bu in the January slot. News that soybean sowing is progressing well across Brazil wouldn’t have helped the sentiment in the US. Sowing progress is estimated at 44% complete in Mato Grosso, 7pts ahead of this time last year. This is a little above the 5 year average but not the fastest sowing we’ve seen there. WorldAgWeather.com shows rainfall over the last fortnight hasn’t been excessive with 20-50mm falling across much of the Brazilian summer crop country, probably perfect. The forecast calls for conditions to dry down a little for the week ahead, with falls of 5-20mm still possible for much of the area being sown.

The good pace in Brazilian soybean sowing and little prospect of any major delays will weigh a little on the oilseed complex in the days ahead. The US continue to have trade issues with China. Soybeans and corn appear to be wearing the brunt of this but corn export sales are still very good. Although we don’t have a lot of official data to back this up just now. The US gov is still shut down.

Canola values across SE Saskatchewan were generally a dollar or two higher ex farm. The average ex farm bid for a December lift was at CAD$563.91/t. This would roughly transpose to a delivered EU market value of something close to US$530 C&F. Compared to an Australian C&F value, which would be closer to US$590. The biggest unknown, and major variable to the canola market remains both Chinese demand, one would assume for Australian canola, and the domestic crush volume for Canadian canola. Both have tentative numbers factored into the global S&D and a movement of 1mt one way or the other on either of these numbers will have a big impact on the market.

International milling wheat values in AUD/t, when compared to yesterdays conversions, are roughly flat to AUD$2.00/t lower out of the US Pacific Northwest and a dollar or two higher out of the Black Sea and Europe, the net change in average world what values is negligible. Interesting to see French durum slipping a little while Canadian values were firmer by CAD$4.01/t XF SE Sask for a December lift. Yet to see some definitive durum grade splits for Canada.

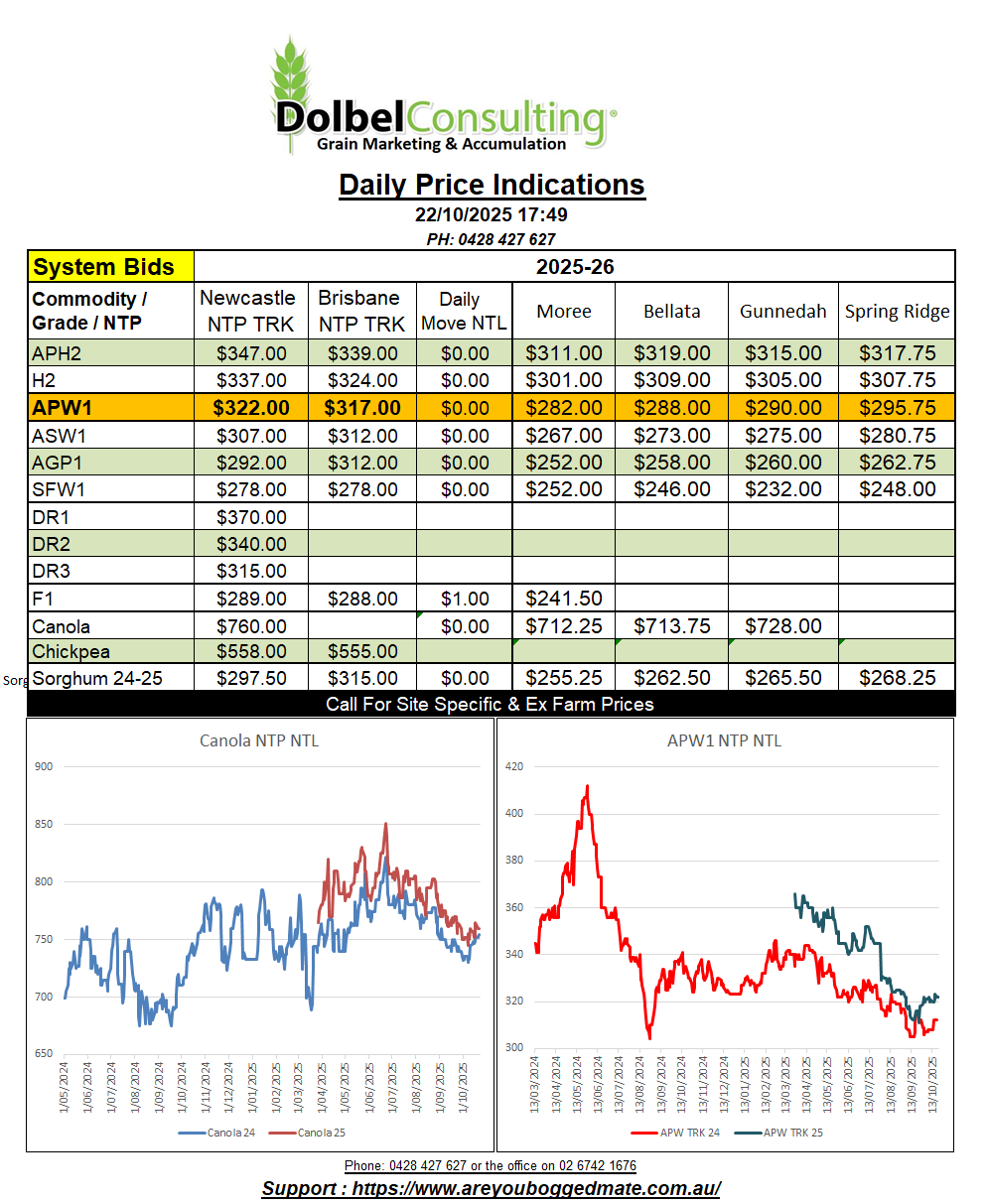

Seeing site specific, grade specific, pricing playing out more now that a few headers are going in the north. This applies to all grains too, not just wheat. In the case of domestic feed grains like barley this is understandable given the potential road execution capacity from the Graincorp site and what it costs to get that grain to market.

Take barley for example, Moree site was bid at $240.50, that’s a Free On Truck (FOT) number of roughly $267.44. The Downs end user market is bid at $302 delivered, leaving $34.56 to get that grain from Moree to the consumer. Goondiwindi silo was bid at $253 delivered site, an FOT price of roughly $280.03 / tonne, leaving $21.97/t to get this to the end user, a difference if $12.59/t to Moree. Depending on the negotiated road freight difference, it would determine if the buyer bid higher at Moree or Goondi.

I noticed that canola also had some site based premiums or discounts yesterday when comparing the NTP Newcastle price derived from adding the GTA differential to the site price at Werris Creek silo. Narrabri and Bellata was +$2.00, Moree was +$5.00, Premer was +$1.00.

There’s a little canola starting to be picked up on the lighter country to the north of Gunnedah now.

Track wheat saw a few more adjustments to grade spreads, APH spread softening a little. H2 into the local track market, say Spring Ridge was bid at $307.75. Although there were no official public bids for H2 delivered into the port yesterday, bids were indicated at $350 +/-. A $307.75 number is equivalent to $332.50 FOT, +$40 freight to port = $372.50 port equivalent, possibly indicating that rail freight is a heap less than road, or port by road values are too low.