23/10/25 Prices

There were some big variations in the international canola / rapeseed market overnight. Paris rapeseed futures gained €7.25/t in the Feb slot. This move was backed up by increases in the cash port values for French rapeseed as well. The day to day conversion comparison increasing by roughly AUD$18.11/tonne. Canadian values were not as volatile. Cash bids XF SE Saskatchewan were actually down CAD$3.46/t for a December lift. While Ukraine values were unchanged. The reports appear focused on the higher production estimates for Canada and lower close at Winnipeg than the sharp gain in Paris futures.

There had been talk that India was going to supply much of China’s rapeseed oil after China implemented a 100% import tariff on Canadian meal and oil. Yet today we read that Indian vegie oil production is expected to decline sharply, and all this while world demand for vegie oil is expected to continue to climb. This comes about as world sunflower stocks decline and international governments continue to increase their requirements for biofuel.

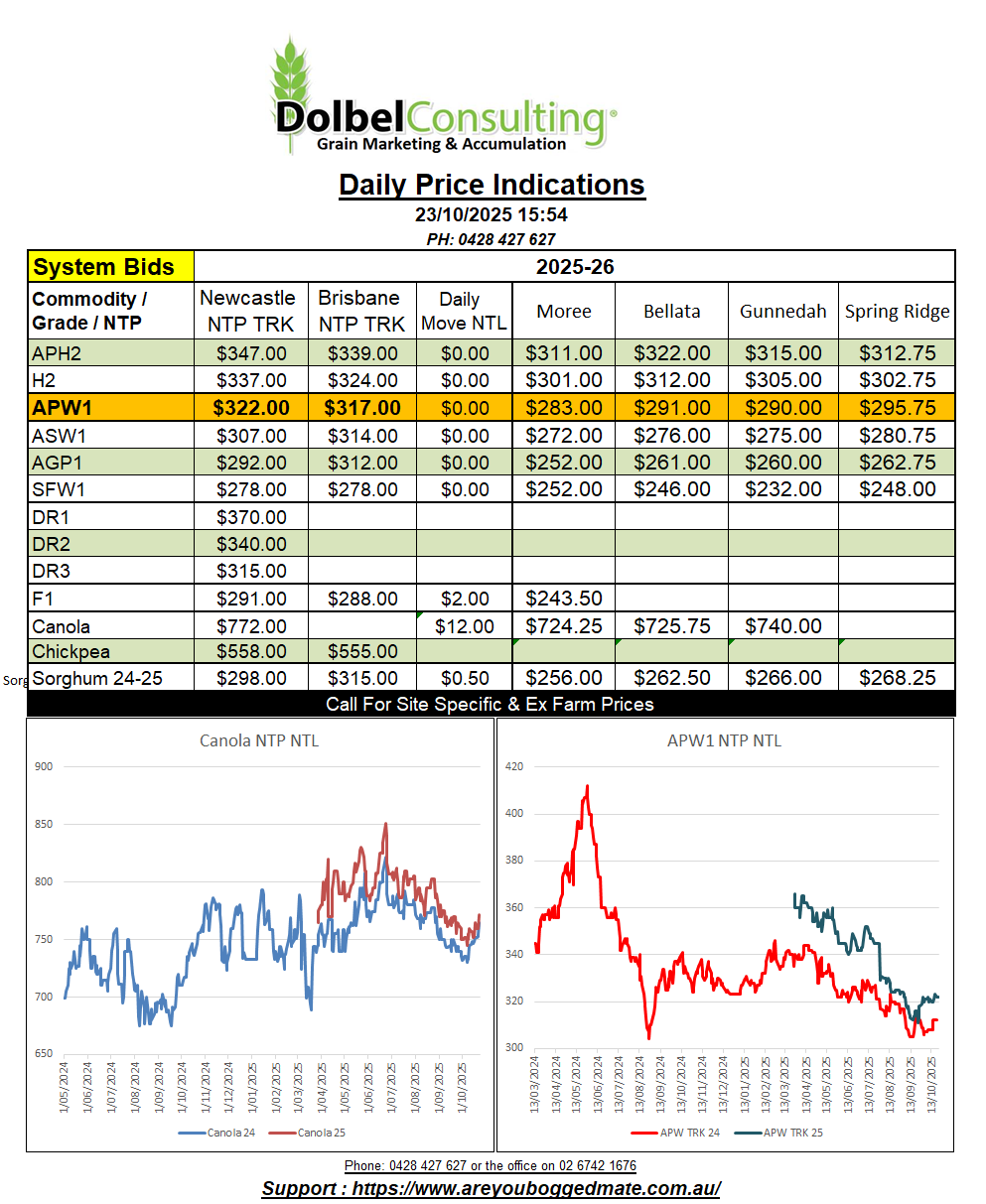

Aussie port price basis to Paris rapeseed futures is roughly about where it was leading into harvest last year, Oct 23rd 2024 -70.71, yesterday, -72.24. We should keep in mind that by 2nd of December 2024 that basis had blow out to -82.2 and to -120 by mid December. Will this year be a repeat, only time will tell but lowering basis as grain is accumulated is common. The question to ask, is will cash prices increase at a rate that will counter the decline in basis. Last year cash price NTP NTL on Oct 23rd was AUD$756, Dec 2nd AUD$741, by mid Dec $780. Paris futures moved sharply higher during the first two weeks of December before falling back to similar values as the beginning of the month by the time Christmas arrived. This presented a short window of opportunity for both the flat price seller, and for the basis trader, who at the time could have picked up greater margins not only in basis improvement but also in the lower AUD/Euro during that window. Can the past predict the future, sometimes, will it this year. I feel there’s a lot more at play now that China has entered the game, basis may not be as volatile unless we see another collapse in the AUD.

I’m not sure how relevant this is to the grains industry but I find it very interesting. BHP from Q4 2025 will settle 30% of it’s iron ore sales to China using the Yuan not the USD as the currency of settlement. This comes as part of the settlement agreement between BHP and China to settle a previous dispute. The deal is valued at an estimate of US$8-US$10Bn annually. It may manage any possible value manipulation from changes in the exchange rate of the USD.

In 2005 the Chinese government overturned their policy of pegging the RMB to the USD, but it remains a government fixed rate currency, floating in a very small range associated with a few international currencies.

Producers continue to prepare for the winter crop harvest and near completion of the summer crop sowing where moisture hasn’t ran out.

The marketing strategy for wheat isn’t rocket science this year. Volatility remains low so the chance of a rally between now and April next year is low. With international values trading at a very low level the consumer is looking at both low prices and good supply, not a recipe for a rally. This basically leaves a couple of options for the flat price seller, which makes up about 90% of farmers. Do you sell as soon as possible, as the basis over US futures is high and one might assume would slip away as the trade pick up tonnage moving through November / December.

Or, do you hold onto stock, dribble sales out to meet monthly cash flow, while hoping for a production issue in the northern hemisphere winter wheat crop as it comes into the thaw period in March / April / May next year. Both strategies have paid off in the past. The later strategy creating enough cash flow to get through to summer crop harvest, sell that, then sell winter grains here in Q2-3 the year after harvest. Cash flow may be your deciding factor this year.

The BOMs new radar presentation is, to put it lightly, rubbish. As I wrote on their “was this page useful ?” section yesterday…. “the new design is like driving a Leyland P76 after getting out of a modern car, yes it’s a car and does things a car should do, but is it the car we want, NO”. The old view was better, and actually worked. It’s bad enough that the BOM can’t predict the weather, now they can’t even supply what is happening in a decent format.

At the chance of getting more cranky about the radar debacle I’ll stick to a basis analysis. Cloud from yesterdays change is now off the east coast. A look at the satellite image shows a large area of raised dust across much of SW QLD and the Downs this morning. Do I have hay fever after a two day reprieve, yes.

Air flow is being generated by a high cell in the Bight, pushing S-SE air across the SE corner of the continent and into NNSW. Another cloud band is moving east ahead of the high cell, if I could access a decent radar image I might be able to tell you how much rain, if any, is falling from this cloud mass.

The synoptic charts are still legible, nothing changed there yet. As the high cell moves east and airflow persist from the S-SE there’s a chance a few showers will develop across the SE corner of NSW and eastern Victoria. By this evening showers should be cleared.

The system to watch continues to be the area of low pressure developing over WA today and tomorrow. As the area of low pressure moves east and consolidates it should arrive at the eastern states as a decent system on Sunday, storms should become active across the plains late Sunday.