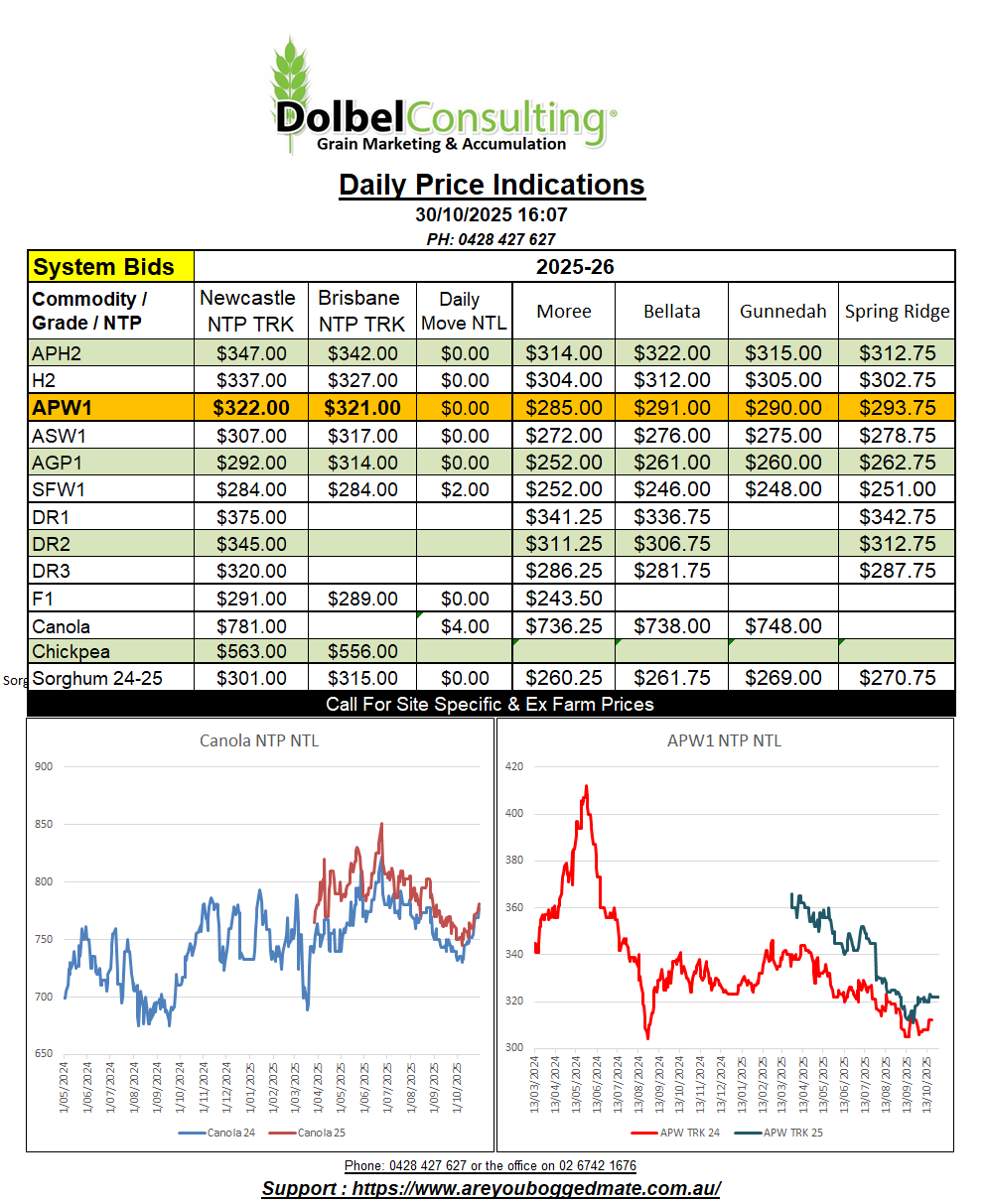

30/10/25 Prices

Canola out of the US / Canadian Pacific Northwest showed good gains overnight. The day to day conversion comparison indicated gains in excess of AUD$15.00 / tonne. The FOB gains were not backed up with higher values across SE Saskatchewan where canola for a December lift only improved by CAD$2.50/tonne. French values, FOB Rouen, were also sharply higher, the day to day conversion comparison improved by more that AUD$17.00 / tonne. These greater gains in AUD/t value are helped a little by the lower AUD this morning. The AUD input is less than $2.00 though.

The improvement in AUD/t in both canola and rapeseed futures was not as good. Paris rapeseed daily price comparison gaining just AUD$2.90/t.

Gains in international cash wheat values were not as good as seen rapeseed or canola. FOB origin values were mixed, some grades and origin ports higher, some lower. The US values out of the PNW have been the ones we’ve been tracking more closely, as they work the best into the Asian markets. White wheat out of the PNW was back about AUD$1.46/t compared to yesterdays conversion. While HRWW was up AUD$2.40/t compared to yesterdays conversion.

Black Sea wheat was generally softer, Ukraine values sharply so, now lower than Russian values not only on a FOB local port basis but also on a delivered Asian consumer basis. Ukraine wheat is still US$25.00 more expensive than US wheat C&F Asian consumer, but is very comparable to Aussie wheat in price to the Asian consumer, but probably a maybe grade difference, even if protein is similar.

French milling wheat futures continue to fail to break higher resistance levels. Cheaper Black Sea wheat caps the rally every time, as it should. French milling wheat is valued at roughly US$218 FOB, versus Ukraine wheat at US$215 FOB. If they are both competing into the same markets Black Sea wheat will continued to make it a hard slog for EU exports to improve. Global wheat S&Ds are telling us this market continues to find little to justify a rally, but at the same time good demand should be stopping values from falling any further. Wheat is cheap, a fall from these values will hurt production in 2026.

Canola direct into the Newcastle crush market continues to draw a premium for the Feb / March slot versus the Nov / Dec slot, not as much as it was a couple of weeks ago, $790 vs $805, but it does represent more than the cost of carry so is worth considering if you don’t need the cash flow immediately. With both the AUD lower and Paris and Winnipeg futures a little higher overnight we should see canola values remain unchanged, or potentially creep a smidge higher this morning.

If looking to book November delivery into the Newcastle crush market it may pay to contract as soon as possible to ensure a timely allocation.

Canola bids into the local track market were steady yesterday. Some buyers are still bidding site specific, preferring and paying a slight premium for Narrabri north. This premium is back on where it was a couple of weeks ago and is now more like a dollar or two compared to the $5.00+ it was.

For those producing good test weight but lower oil content canola the flat price market into Tamworth or Newcastle feed mills may be a better option. With Tamworth bid at $745 delivered yesterday it basically represents about the same ex farm return as someone delivering into Emerald Hill track. Once oil P&Ds are considered, when oil content falls below about 43.5%, the Tamworth option becomes more viable, especially when considering the discount table for impurities too. Yesterdays comparison tables attached. Again cash flow and oil will decide whether to worry about chasing flat price or not.

Bids for milling wheat remain focused on track accumulation by the trade at present. Track appears to be the lowest return to the producer, as opposed to the delivered market to port of mills. Grades in the north continue to show a good slice of H2 coming in, similar to last year. SFW spread continues to narrow.

Storms are active across western South Australia this morning, ahead of weak low cell pushing east. There’s a high cell closely following this low, both appear to be expanding to fill the widening gap between the next system approaching from the west and the system that produced the recent rain here. It’s like a case of Claytons weather, the weather you have when you are not having some weather.

The most interesting development of this system is that the low cell currently pushing into SA is expected to track in a more NE direction. This may not only produce some storms across the southern half of NSW but may also see storms develop along a shallow trough line expected to pass across the NWSP late Friday or Saturday.

The BOM expect the area of low to weaken once it moves across NNSW, potentially being taken in by a deepening area of low pressure over central Australia. A high moving east across the Southern Ocean will encourage the area of low pressure over central Australia to drift SE and into western NSW on Sunday. Airflow from the NE will mix with airflow from the SW across western NSW on Monday, the trough line will push NE across the state producing storms predominately across the central and southern half on Monday but also here on the plains either very late Monday or on Tuesday morning. Rainfall here on the plains is expected to be minimal but the SW and far NE of the state may see some higher recordings under storms around Inverell and Condobolin on Monday evening.

Storms here on Friday will be mainly to the south, Coolah and the Upper Hunter, but may spill onto the bottom of the plains.