4/11/25 Prices

Rumours that China are also in for some US wheat kept the bulls fed on Monday. China is expected to buy their average volume of US soybeans but are now also expected to pick up some US wheat along the way. There’s unconfirmed talk that China is about to suspend levies on agricultural products from the USA. This might keep the wheat market in the US humming along a little better than it has been but the removal of import tariffs on wheat, and possibly sorghum, may hurt the new crop sorghum value here a little.

I’m not 100% convinced it will hurt it a lot, unless the trade try to make it hurt. Prior to the implementation of the tariffs sorghum values here were stronger than US values would have otherwise indicated. The implementation of the tariffs did see a slight increase in local prices but not to the full value of the tariff. The major issue Aussie sorghum will face is more likely to come from Argentine product which is currently worth about US$258 C&F China. Current Aussie bids would place Aussie sorghum at US$248 C&F China, so still competitive at this stage.

Back to wheat. The bulls may quickly discount the Chinese demand news unless we see confirmation of some US sales. This is a little harder to confirm now the US government is in shut down and there’s no reports on US export shipments or sales getting published, very convenient. This may, as a result of the delay of this information, create quiet a lot of volatility in the market once the USDA reports do come out, especially if there’s a few hidden gems in the data.

According to some reports US wheat exports continue to push along nicely, some 21% ahead of last years export volume for this time of year. US soybean exports are terrible, about 40% below this time last year and corn continued to move out at a record pace, US exports now pegged at 64% bigger than the same time last year.

Conditions in China had improved a little over the last couple of weeks after very heavy rainfall continued to hurt summer crop harvest and delay winter cereal sowing. The 7 day forecast model is showing that the reprieve may well end this week, with 30-100mm predicted across parts of the N.China plain.

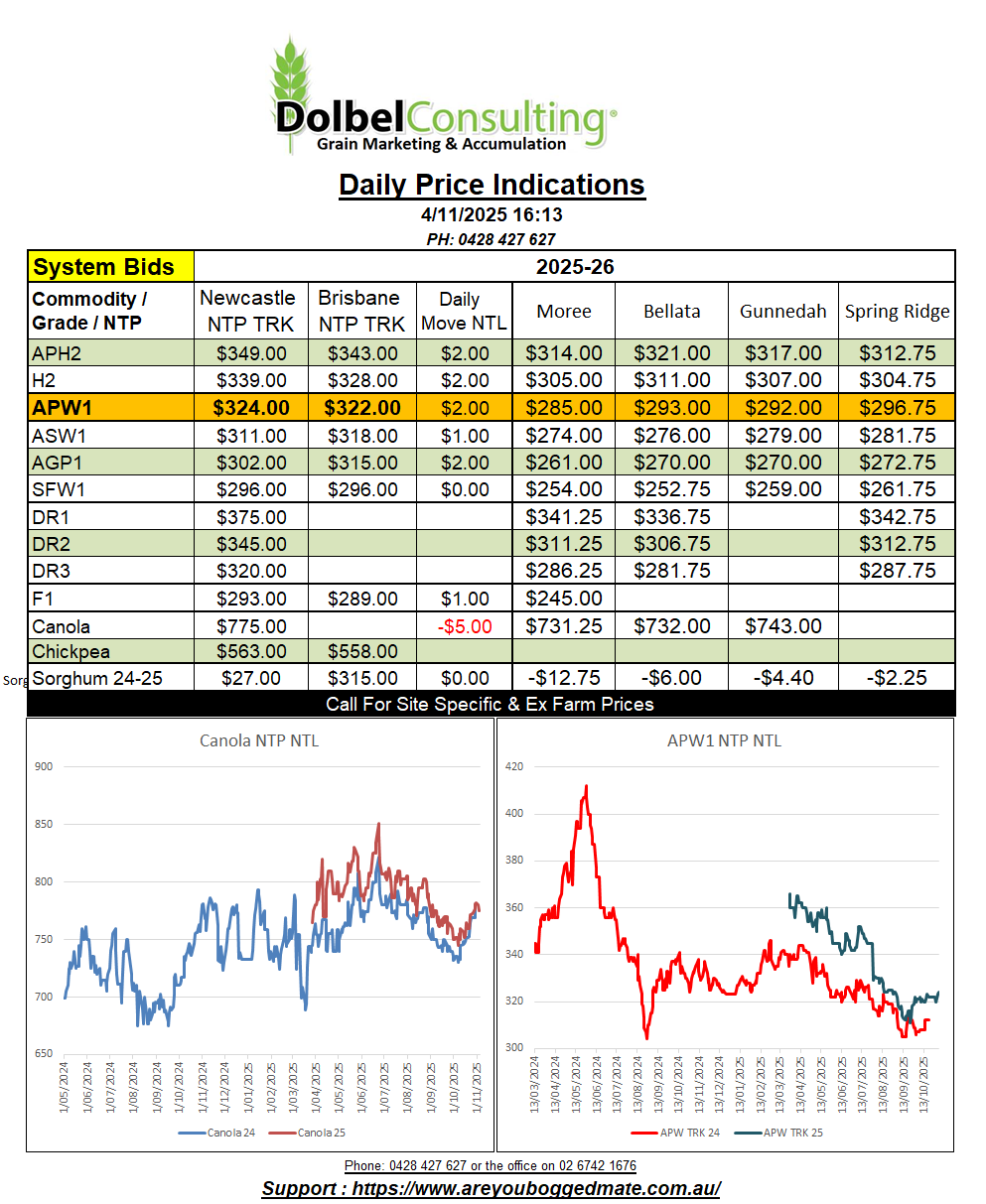

Local canola bids done well to shed just $2.00 yesterday. Basis improving as the weather outlook for much of the canola producing regions in Australia continues to be less than ideal. Overnight Paris rapeseed futures were a little lower while cash values out of Rouen France were in AUD/t terms a smidge higher. Canadian canola values were sharply higher, taking back much of the fall on Friday. The average price for canola XF SE Saskatchewan followed the futures market at Winnipeg, which showed a gain of AUD$10.35/t on the day to day conversion comparison.

Although Paris is weaker day to day in AUD terms, we do have a sharply higher Canadian product. The margin we had over the Canadian product was $70 on Friday, plenty of room for shrinkage in Aussie values or increases in Canadian values. To see the later is encouraging.

Locally there’s more canola coming into the system now but weather is limiting. Oil content remains a little low. Sub 42% does incur dockage when delivering to either the local system or the crush market in Newcastle. The ISCC “premium” will also need to be deducted from local bids for those not happy to sign up for a possible audit.

The local stock feed market is flat priced but has limits on test weight, this market does suite the producers with low oil, good canola. But demand is limited and can be covered easily so this is often not a suitable option for harvest movement off the header, but does suit short to mid term storage ex farm.

Wheat basis to Chicago was lower, falling from +47c/bu on Friday to +42c/bu. This could be viewed as a win for the trade but at the same time local cash prices for H2 wheat on the track improved $4.00/t. The fall in basis is equivalent to about -AUD$2.80/t.

Lots of of hail over the weekend, from CQ to the LPP and up and down the coast. Crop losses are often limited by the size of the storm thus regional losses are often insignificant, unlike localised losses.

The main front is now well to our east creating showers east of the ranges and across the Inner Downs and CQ this morning. The secondary front is unlikely to produce storms this far north this mornings but the likelihood of storms south of Dubbo remains higher today.

The BOM synoptic analysis shows the low cell off the west coast of Tasmania drifting SE during the day, pulling the secondary trough line south as it does, hence the storms will be more prolific across the southern half of NSW and Victoria today as the system pushes further SE. Storms are likely to persist across the Downs but should clear tomorrow.

The next change is due through on Saturday. An intense area of low pressure is expected to push across the Great Southern on WA, the heart of the WA wheat belt tomorrow. The low cell is expected to be 998hPa when is crosses the coast between Geraldton and Perth tomorrow, not ideal on a ripe wheat crop. The low will leave the WA coast in the Bight of Thursday and move east towards Victoria before passing across Bass Straight on Friday night. The trough associated with this low will move across the NSW wheat belt on Friday night / Saturday producing storms producing non severe storms.