18/11/25 Prices

International futures markets are mostly higher this morning. Chicago SRWW and HRWW futures saw double digit gains. Minneapolis spring wheat was a little more subdued, but did see some good gains in nearby values. Chicago soybean futures were sharply higher, gaining 32.75c/bu (AUD$18.55/t) in the January slot, lending support to both Winnipeg canola and Paris rapeseed futures. Soybean products were also firmer with meal and oil closing in the green. Palm oil futures were not as influenced by soybean as what canola & rapeseed was, palm oil gaining just AUD$2.22/t in the Jan26 slot.

International cash grain conversion comparisons against mid last week are firmer, with good gains in both wheat and oilseeds. 10.5% white wheat out of the US Pacific Northwest, when compared to values mid last week, is up roughly AUD$8.91/tonne. Hard red winter wheat and spring wheat out of the US PNW are also up +/-AUD$8.00/tonne when comparing today’s values C&F Asian consumer mid last week to last night, then converting that value to an AUD/tonne equivalent price ex farm LPP.

Last weeks US export inspection data continues to show very good international demand for US corn with shipments exceeding the highest trade estimate prior to the reports release. At 2.054mt it’s right up there, and almost 600kt higher than last weeks volume, which wasn’t too shabby. US corn export shipments for the marketing year stand at 15.839mt, some 73% higher than the same time last year. Although US weekly wheat shipments were below even the lowest trade estimate prior to the report, the 247kt shipping number takes MY shipments to 12.363mt, +19% on this time last year.

Russian winter wheat sowings are all but complete and the season seems to be handing over to winter in almost ideal conditions. Rainfall across eastern Ukraine, central Russia and most of the Volga Valley has been very good, 110% to 125% of average rainfall over the last 30 days.

spent most of yesterday on the road in and out of service. The few calls to merchants I did have indicated that not a lot had changed since mid last week. Looking at the movement in US futures and the AUD this morning, one could assume that we may well see any weakness that was seeping into the market late last week evaporate today.

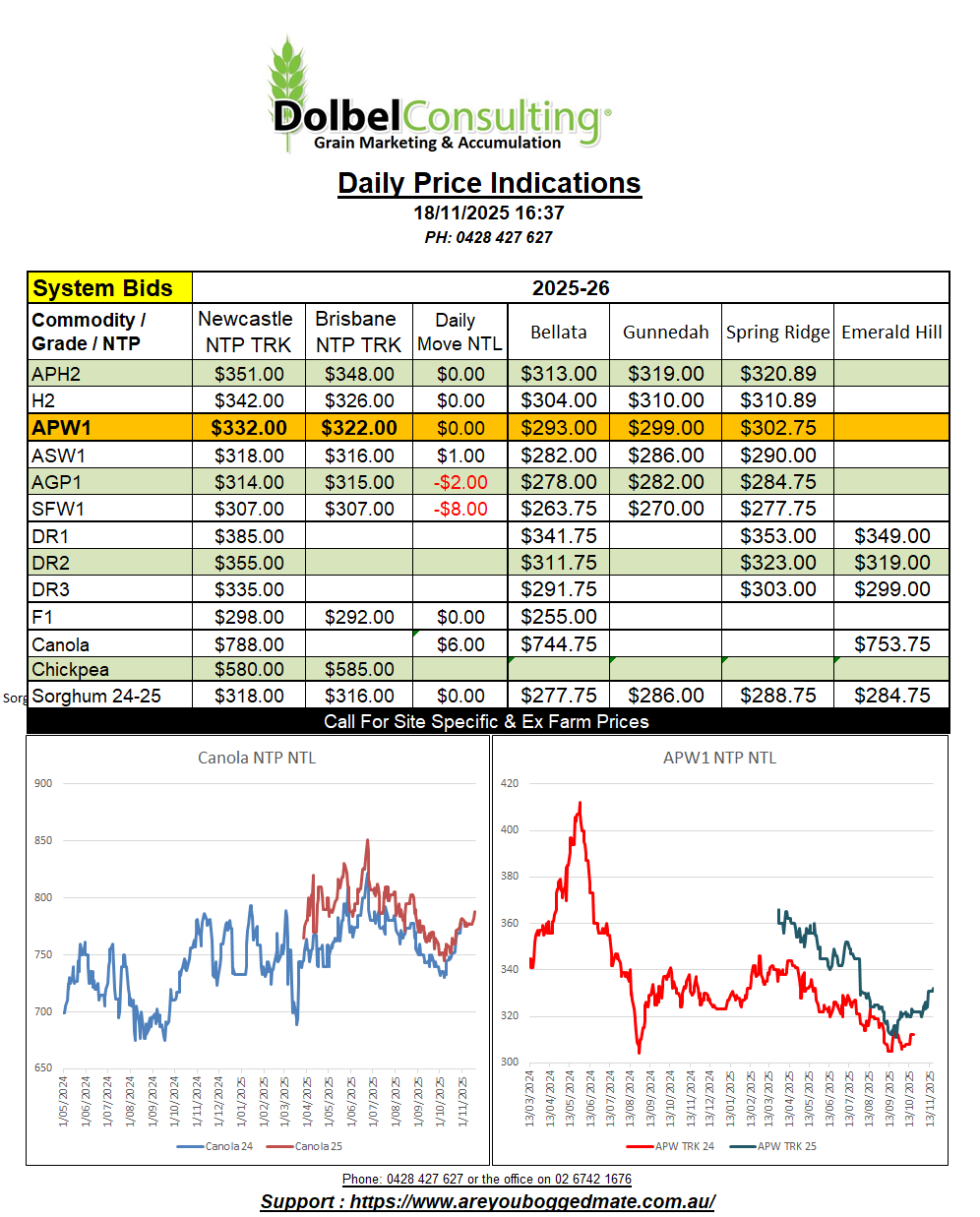

The trade continue to seek SFW1 into both the LPP and Hunter Valley markets and ASW into the Biada consumption market here on the plains and into Newcastle. There’s limited demand for H2 / APH2 into the port, most buyers currently happy to direct harvest sellers to the central storage system. H2 at Spring Ridge closed the day bid at $312.75 / tonne. H2 direct to port saw indicative bids of $355 to $365 delivered Dec / Jan, buyers call.

SFW1 was bid at $290 ex farm, with grower offers not falling below $295 for prompt pickup. There’s continued demand for 500-1000t of SFW1 per week available to ex farm sellers for the Nov / Dec period at present. Keep offers high today, maybe start at $300 XF. Soft sellers will be your competition.

Seeing some screening issues in the Premer Valley, grain suffered from the dry finish and failed to fill the head, producing screenings to 25% and reduced test weight in some samples. If this grain can squeeze into HPS1 grade, it was bid $290 delivered Manildra Gunnedah yesterday. There were reports of HPS1 trading at $265 ex farm SW LPP. Personally I’d be grading this wheat and selling the gradings and grade out as two different parcels. It might cost $20 to grade but if the end result is a 50/50 split APH / FED, at least half of it will be worth $340 / tonne XF, the FED half maybe $260 – $270 come Q2 next year.

Both Paris rapeseed and Winnipeg canola are firmer this morning. Combine this with a weaker AUD and we have some good upside potential for canola today.

Storms are active across the north west portion of the WA wheat fields this morning. A low cell off the coast of Geraldton is pushing moist NE airflow onto the coastal fringe and creating a few storms. There’s a low cell further to the north that is expected to weaken over the next couple of days, but the cell to the west that is creating today’s showers between Geraldton and Northam, is expected to intensify and push SE across the WA wheat fields from Wednesday night through to Friday.

Here on the east coast our weather will be greatly dictated by a slow moving high cell off the east coast of NSW and another high cell tracking east across the Southern Ocean towards Tasmania. Neither are inducive to rainfall but we could see a shallow trough line develop as the airflow from the two systems merge over NSW late Thursday and Friday.

The development of these troughs may see some thunderstorm development along the western edge of the Newell on Friday evening, possibly tracking east across the plains late in the day or early evening. These storms are likely to be more severe across the eastern edge of the plains between Narrabri and Moree, and towards Inverell late in the evening. Storms may also push east across the Upper Hunter late Saturday night.

Storms here on the LPP are likely to be more intense to the south of east of Goran Lake or closer to the ranges to the south and east.

There’s a remote chance a surface low will develop over central NSW on Sunday but should move east and off the coast quickly.

Keep an eye on the low cell near Darwin, there’s a good chance it will be our first cyclone on 2025-26.