20/11/25 Prices

Chicago SRWW and HRWW futures pushed lower by AUD$5.55/t. The weaker AUD has countered some of the decline in the conversion to AUD/t. The move in the dollar roughly equal to 5c/bu, or about +AUD$2.59/t, resulting in net change of about -AUD$2.78/t in Dec SRWW futures.

The move in US futures was reflected in the FOB offerings out of the US Pacific Northwest. Day to day conversion comparisons for HRWW saw values there fall roughly AUD$2.97/t. Spring wheat futures were lower by less than either SRWW or HRWW. Cash values for spring wheat out of the Pacific Northwest saw a little downside in USD/t but the weaker AUD easily countered that weakness, turning the day to day conversion comparison into an increase of AUD$3.00/t for spring wheat. 10.5% White wheat out of the PNW improved in value by roughly AUD$6.00/t compared to yesterday. US club white wheat is roughly equivalent to US$270 C&F Japan, roughly the same as our H2 wheat. Compared to Aussie APW1, US WW may struggle to buy Asian demand.

The latest Canadian data confirms some quality issues in the Canadian durum crop this year. Both fusarium and sprouting causing downgrading to CWAD3 and CWAD4. 33.4% of the Canadian durum samples contained 0.3ppm to 1.0ppm DON content, 4.22% of samples contained greater than 1.0ppm DON. Falling number count was above 351 seconds for 58.6% of the samples and below 250 seconds for 17.5% of samples.

Italian demand for durum remains high. Currently Australian DR1 values indicate that Aussie durum should be competitive against both the best of EU and Canadian product into Italy. The softer AUD counters any negativity to the day to day conversion comparison, in fact it helps increase the comparison for both French and Canadian values by roughly AUD$2.50/t.

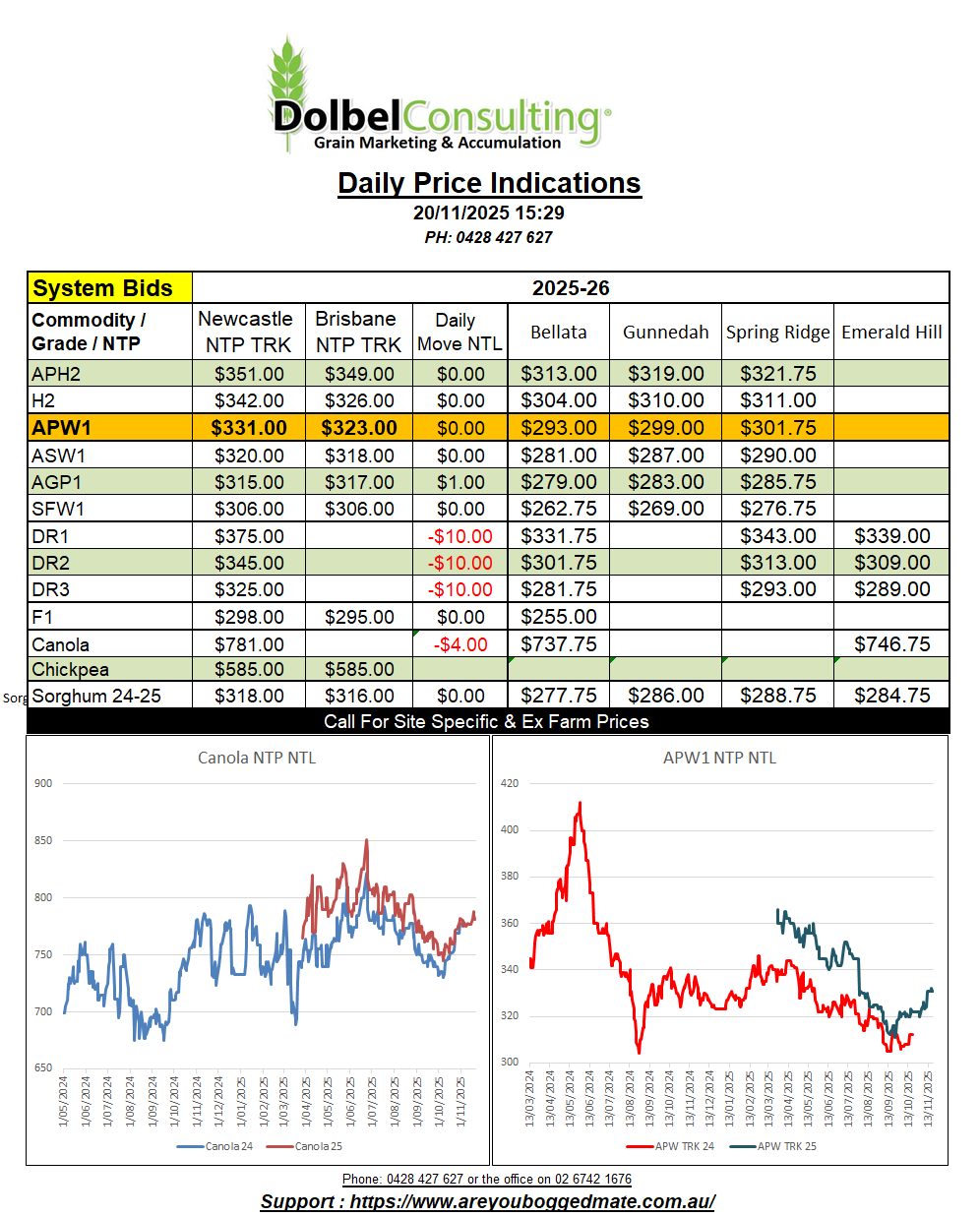

French rapeseed futures were flat. FOB Rouen values were lower by roughly AUD$5.70/t compared to yesterdays conversion. Canadian canola works into France at roughly US$545 C&F compared to an Aussie value closer to US$585, the gap has shrunk a little and may continue to do so.

Activity yesterday was on track wheat and canola and delivered feed barley.

Feed barley moved into the Liverpool Plains consumer market at $295 delivered prompt as it comes. These immediate slots are getting harder to find, most consumers now covered by the trade, and the trade are also covered, generally not bidding for anything closer than December / January. Barley quality on the plains is variable but most earlier samples are making BAR1. BAR1-2-3 segregation are open at some Graincorp sites.

Track wheat was softer late morning. The leading bids were stronger than the next buyer by a fair margin, and with some of the major track consumers pulling back out of the market on the day this left the trade mostly reluctant buyers. Site specific pricing came into play, and some sites fell $3.00 to $4.00 for some grades, while other sites, lesser volume on offer sites, remained unchanged.

H2 into the Graincorp site at Spring Ridge was bid $310.89, down $2.00 from last Thursday which was the best price available at that site for H2 since mid July. H2 into the delivered port market struggled to find a bid without an offer to flush a bid out. Last bid was $360, that was against a $370 offer. Sentiment has weakened a little on wheat, as is often the case mid harvest and mid N.Hemisphere winter. Fundamentals were also more bearish than bullish wheat in last weeks USDA WASDE report, but not bearish enough to have producers selling wheat for less than it costs to grow it. Mid to longer term the trade generally expect to see lower world production for 2026-27, possibly helping prices in Q2-3 next year. Low prices fix low prices. Short term the market looks flat, the trade have been absorbing much of the potential volatility in basis changes, presenting very few “good” opportunities to price wheat in a rally.

Cloud associated with a large area of low pressure over central and southern Western Australia is drifting slowly SE and should move across South Australia over the weekend.

An unusual synoptic chart shows the mainland generally dominated by low pressure. The pinnacle of which is a cyclone off the coast of Darwin that is expected to make landfall there on Saturday night, before tracking SW back into the ocean and along the northern WA coast line. By mid next week the cyclone is expected to breakdown as it moves further SW away from the WA coast.

Our weather will be mostly affected by a weak ridge of high pressure pushing across the Bight and into the Tasman. This high pressure ridge will create mostly east to north east airflow over NSW and QLD between today and Saturday. Feeding moisture inland an towards a shallow trough line developing along the western edge of the Newell.

An area of low pressure is expected to develop over the NE corner of S.Aust on Saturday. The models do not expect this to develop into a cut off low over the inland but we may see a surface low develop over central or south east NSW on Sunday as the low leaves the NSW coast around Tathra. Airflow into the surface low will become more NW on Sunday, feeding little to no moisture into the system.

Friday still looks to become stormy from early to mid afternoon, mainly towards the west, possibly along the eastern edge of the Newell. Storms more general on Sunday but again heavier to the west of the Newell initially but tracking east across the LPP overnight Saturday. Storms are possible again Sunday arvo.