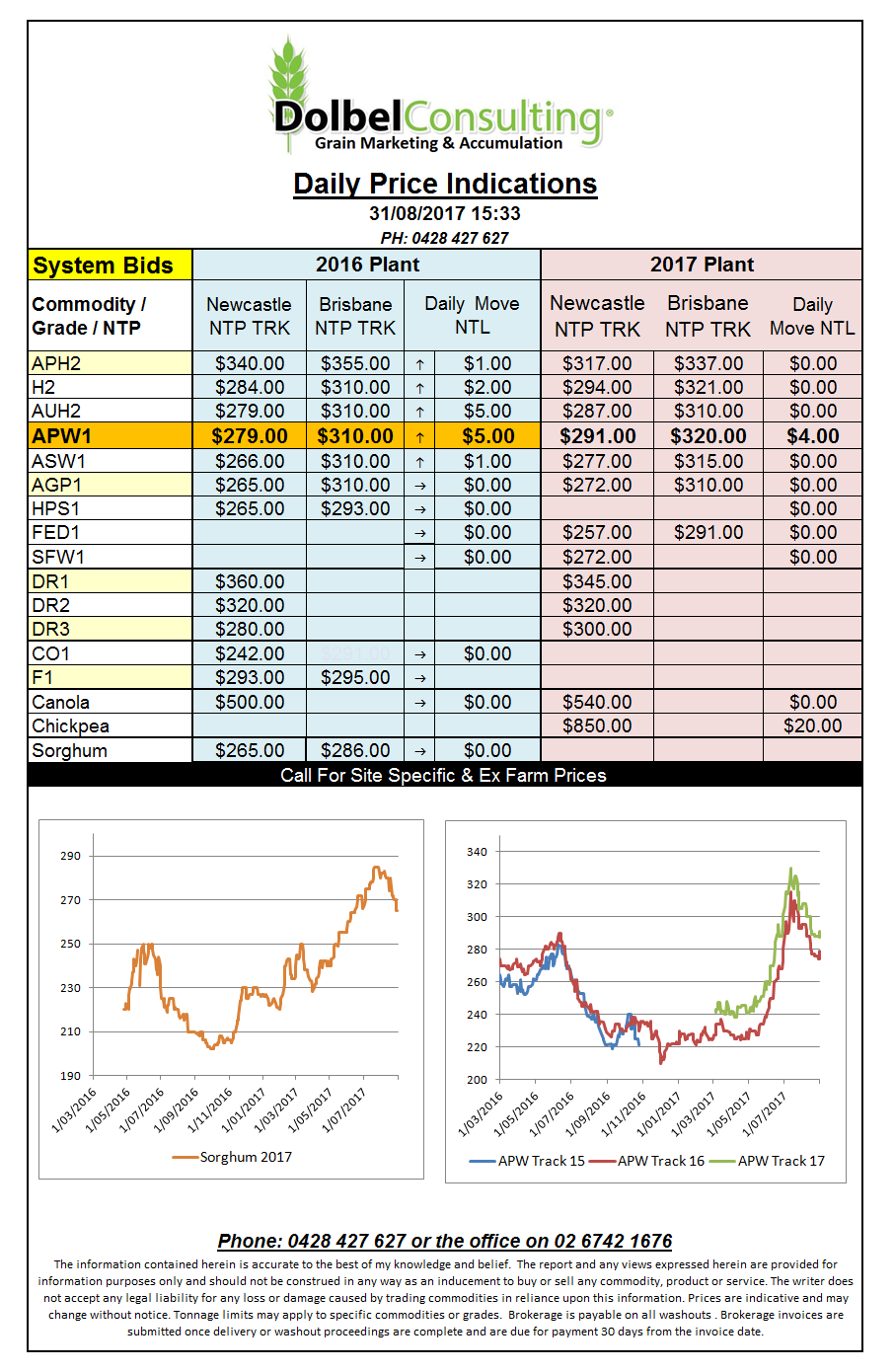

Prices 31/8/17

The USDA have Russia pencilled in to export 31.5mt of wheat in 2017-18. We all know Russia won’t have an issue producing this number with a record 80mt crop coming off presently but some believe that export capability will be the cap.

The marketing year started in July, during which Russia shipped 1.4mt of wheat, this was 1.2mt shy of the total wheat need to be shipped on average per month to achieve 31.5mt.

Simple maths will tell you the average pace needs to be 2.625mt to complete the task. The IGC have Russia pencilled in at 32.5mt, 1mt higher than the USDA. Unless the pace picks up considerably we may well see world carryover building yet again. In the short term though the export limitations may well become beneficial to wheat prices.

In this week’s tender from Egypt Russia once again dominated with the lowest price coming in at US$186/ tonne FOB. The cheapest offer from France was almost US$10 higher than this. The tender average US$187 / tonne, is the lowest valued tender this season into Egypt.

In the US wheat prices were mixed. Soft wheat was flat to higher, HRW higher and spring wheat lower in the futures market but higher in the cash market for protein above 14.5%. Harvest pressure continues to see US durum values slip away to AUD$350XF. The lack of demand from major importers is also evident but is usual for this time of year as they consume domestic product prior to importing.