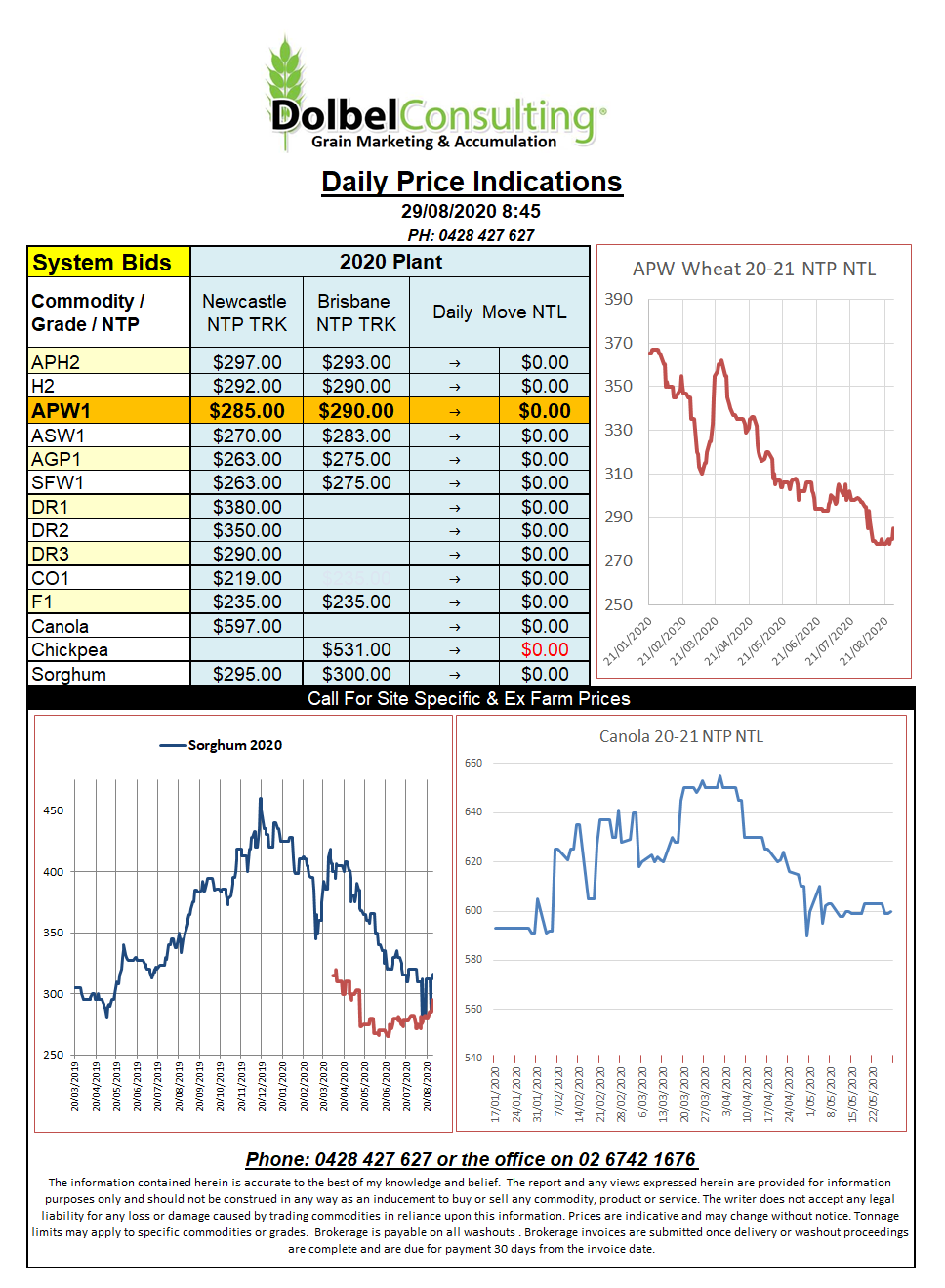

28/8/20 Prices

Indian chickpea values have pushed higher this week with the outer months firming by over AUD$30 / tonne. The Indian government continues to put in place supply / support programs during the COVID19 pandemic. These programs include supplying 1.5mt of chickpeas to both the community and the migrant work force. Additional chickpeas will also be supplied to the army. This is expected to lead to a big draw down on stocks, possibly leaving the government with little to no carry over by March 2021.

Lower production of Kabuli chickpeas this year will also see the larger peas in high demand but Indian consumption has also been back a little thanks to COVID restrictions on eating out.

In the USA funds were mostly buyers in the grain pits. Corn found support from continued speculation on the size of the US crop and what final yields will be across Iowa after the storm a couple of weeks ago. The USDA reported weekly corn sales at 1.45mt, this was towards the higher end of expectation. There were also reports of another sale of a 750kt US corn to China overnight.

State owned corn auctions in China continue to be well subscribed with confirmation the latest auction cleared almost 4mt last night.

Soybean futures were the big winners at Chicago with double digit gains on the back of good old / new crop sales of 1.9mt, this is a significant volume. US sales volume will need to pick up if they are to meet USDA projections.

Wheat futures, although mostly a follower of the row crops, did put on some healthy gains. US sales were better than expected at 765kt.