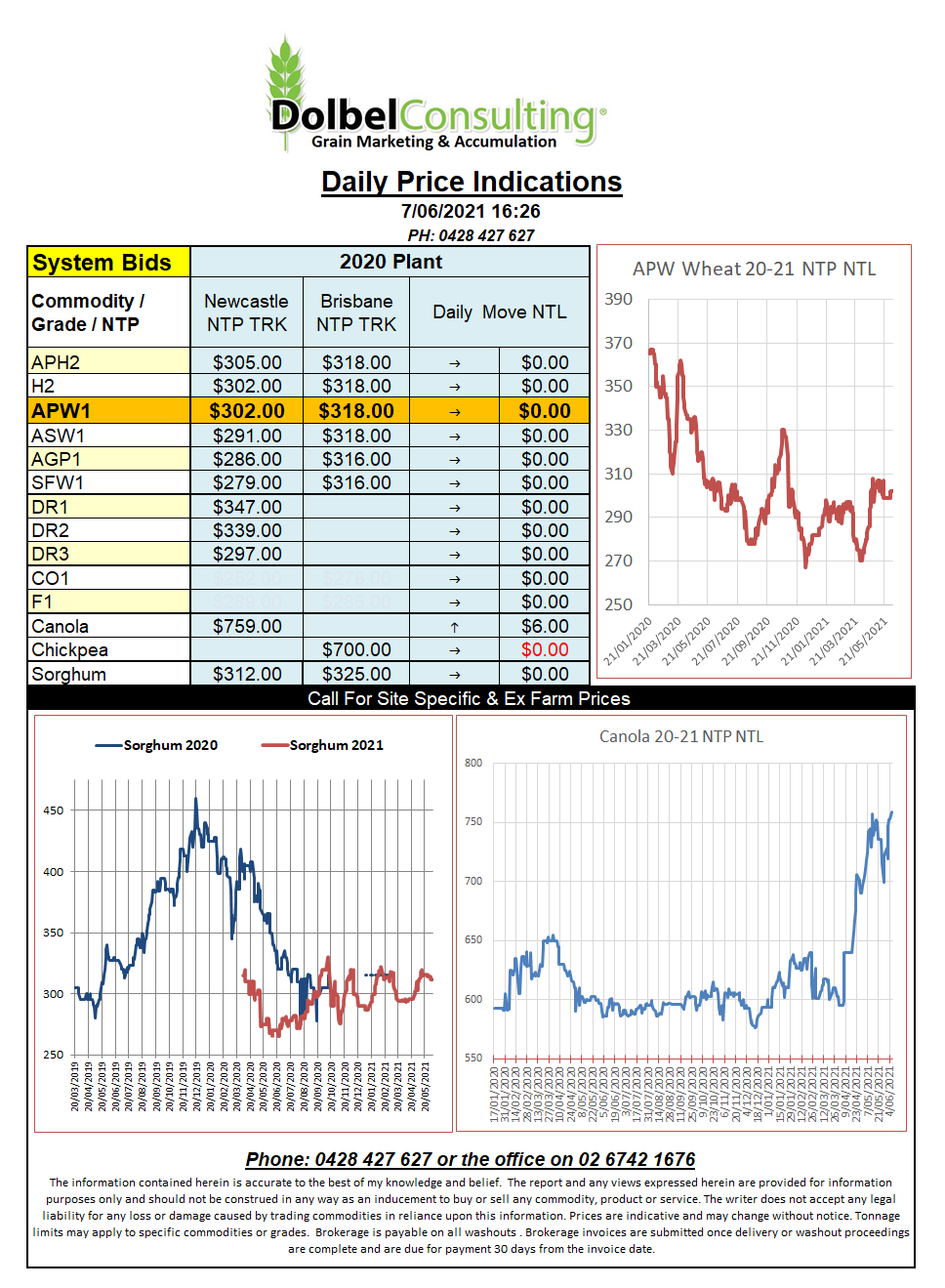

7/6/21 Prices

Traders took a last look at the US / Canadian weather map on Friday and realised things ain’t great in the northern plains. Temperatures over the next couple of days are expected to get into the mid to high 30’sC across the Dakotas and into MN. In some locations this would represent a deviation of around 10C to the average for this time of year. Combine this with a 7 days rainfall forecast for little to no rain and we are starting to see why spring wheat is now leading the race in US futures volatility.

Cash bids across SE Saskatchewan were mixed, spring wheat up by as much as C$11 to C$12 / tonne while durum continues to stall, remaining flat to softer and now at a C$13 discount to spring wheat for a Dec 21 lift.

Cash bids for canola saw some big moves too, up C$21.90 for a Dec 21 lift to C$736 / tonne. On the back of an envelope using Europe as a home this would equate to a Aussie port number somewhere around AUD$856 / tonne. Yesterday new crop cash at the port was AUD$778, so there’s still plenty of fat left in forward contract values for those looking to lock in a little new crop. Local basis here went from -$30 to -$14, anything negative for a forward contract this time of is a bit hard to swallow.

Cash bids for US spring wheat out of the PNW were sharply higher, up 33c/bu for 14%, averaging out at US$9.20/bu for a Sept lift. Inland on the Lakes cash bids were actually flat to softer but still very high. Executing the PNW product and using Japan as a consumer we would come back at a rough port equivalent at Newcastle of about AUD$400. This is off a nominal freight rate to Japan of about US$50 which is probably a little high too.