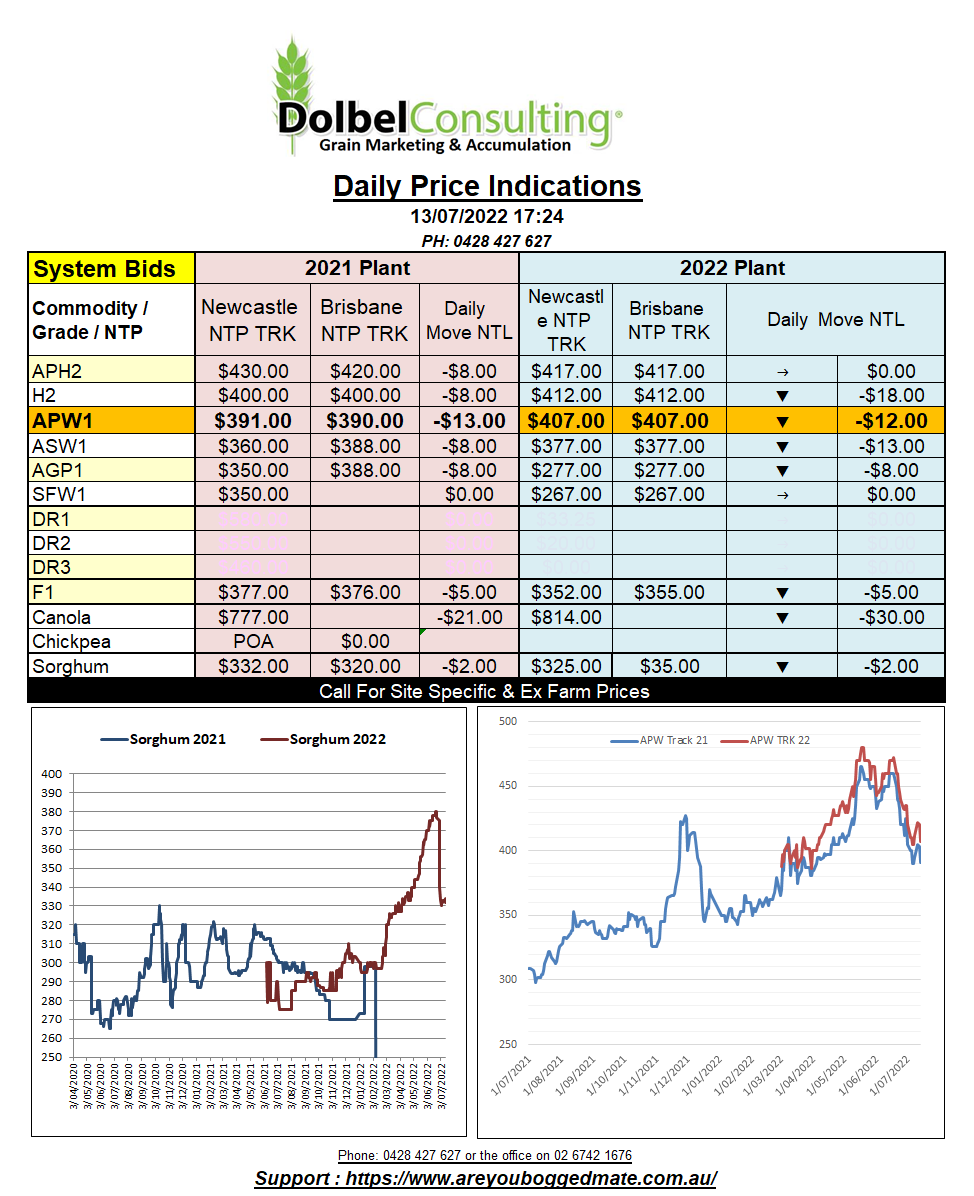

13/7/22 Prices

It was WASDE night last night and it appears to have flushed out the bears. Wheat, corn, and soybean futures in the US were all sharply lower. Let’s have a look at the wheat side of the report and see what the USDA have thrown in the pot.

First of all, we see global wheat production is lower, now estimated at 771.64mt versus 773.43 last month. Beginning stocks were increased by 700kt but the critical part is the reduction in domestic consumption, I find that a little interesting, but the high price of wheat does make alternatives look cheap in many locations. The net result is an increase in the ending stocks of 670kt. An adjustment worthy of a 40c / 50c per bushel move lower in futures, I don’t think so. It’s not bullish, that’s for sure, but worthy of a 6% move in values, that’s questionable.

Some of the more interesting numbers for wheat are. US production increased 1.21mt, Argentine production reduced just 500k to 19.5mt, Australian production was unchanged at 30mt. Both Argentine and Aussie production could have easily been reduced 1mt each. Canadian production was increased 1mt to 34mt, big call. EU production was actually reduced 2mt to 134.1mt, looks about right. Russia was increased 500kt to 81.5mt, according to all the reports coming out of Russia this also looks about right. Russian ending stocks were increased 500kt though. Ukraine productions was reduced 1mt to 19.5mt, their ending stocks also reduced by 770kt. Ukraine exports just 10.2mt as opposed to 18.8mt last year and 16.85mt the year before.

On the consumption side of the equation there’s not a lot of change even after the buying spree some of the major consumers went on over the last couple of weeks. Chinese imports were left unchanged at 9.5mt, SE Asian imports were increased 200kt to 26.23mt and N.Africa imports were increased 200kt to 29.4mt. Chicago soybeans were a big loser overnight, the weakness spilling over to both the ICE canola contract and Paris rapeseed. A slight improvement in the AUD will not help. Sharp reductions in corn futures may spill over to further weakness across the global feed market.