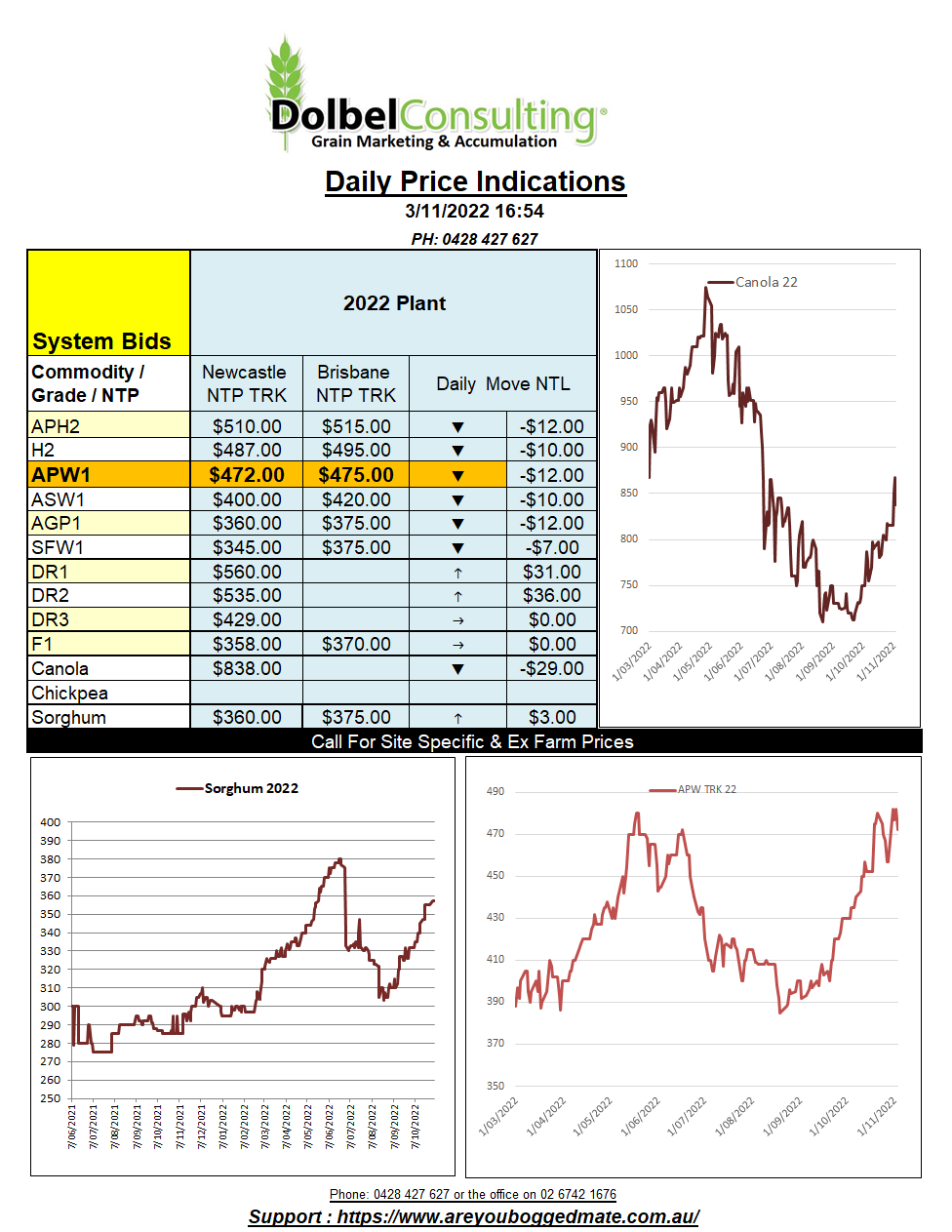

3/11/22 Prices

I can see Putin at the office now, “I’ll show you guys how to make some money on wheat options, watch this”.

So the grain corridor deal is back on again. As you would expect the news hit the market prior to the open at Chicago and wheat futures were smashed from the beginning of the session. Chicago soft red winter wheat futures for the December slot slipping 56.5c/bu (AUD$32.55/t). We are now seeing a carry in this US futures market out to Dec23 (can’t help but think that the trade is ignoring the US winter wheat crop rating somewhat).

To say that some traders are becoming a little jaded by all of this may be an understatement. It’s not just the impact it has on futures, the physical markets are not as reactive now as they may have once been either. Corn for instance was the main grain affected by Monday’s decisions to stop Ukraine exports, yet it was mainly reflected in wheat. Could this be the modern-day example of the boy who cried wolf, makes one wonder who the actual wolf is though, or are we dealing with BabaYaga.

A decision will be made after November 18th on the Russian involvement and the continuation of the grain corridor. Let’s see how the option traders gather on the days leading up to that “negotiation”.

The Pakistan government has agreed to purchase 300kt of wheat from the Russian government, a gov to gov deal. Pakistan will become a major importer of wheat over the next twelve months. A number of factors reduced Pakistan wheat production in 2021-22 but the major cause of the reduction was flooding, which was said to have swept away many stores of wheat. It’s hard to be bearish wheat, the Black Sea “Deal / No Deal” game is muddying the water, the drought in the US and Argentina and floods here are major events that in their own right are market movers.