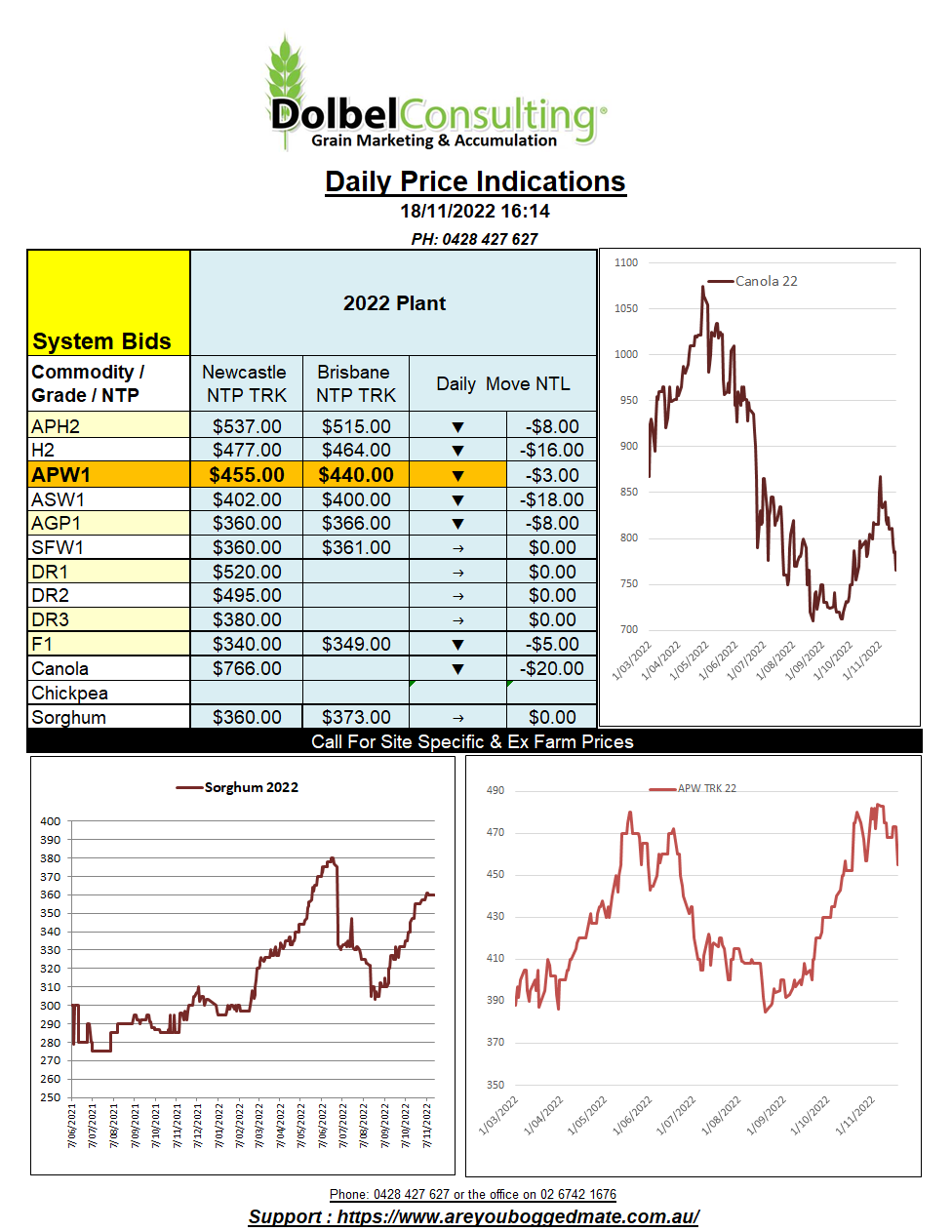

18/11/22 Prices

The grain corridor deal between Ukraine and Russia has been extended another 120 days (March 19th). This news was generally expected and appeared to have minimal impact of the MATIF milling wheat contract, which rallied AUD$7.36 per tonne on the December contract.

US wheat futures pushed lower after the announcement triggered a few sell orders. Consensus before the announcement was that it was a done deal and most traders and punters expected the extension, possibly with a few new provisos. The dip in futures, is considered by some, a buying opportunity.

Chicago soybean futures fell away, dragging both ICE and MATIF futures lower. Paris rapeseed slipped E16.75 on the nearby contract, that’s almost AUD$26. ICE canola futures at Winnipeg were also lower, back C$20.70 on the nearby contract, that’s about AUD$23.22. Weakness in the US soybean market came from expectations of a larger Brazilian crop thus increased export competition.

US weekly export sales for soybeans were huge at just over 3 million tonnes, China taking almost half of that total. Not exactly a reason to push a market lower on the nearby one might think.

Pakistan is tendering for another 500kt of wheat. The tender will close on the 28th.

The International Grains Council had their monthly stab at a world S&D sheet this week. Wheat production was reduced 1mt to 791mt, carry-over stocks were reduced 4mt to 282mt, still too high. The reduction was mainly attributed to the drought in Argentina. Quality concerns for the Aussie crop… doh.