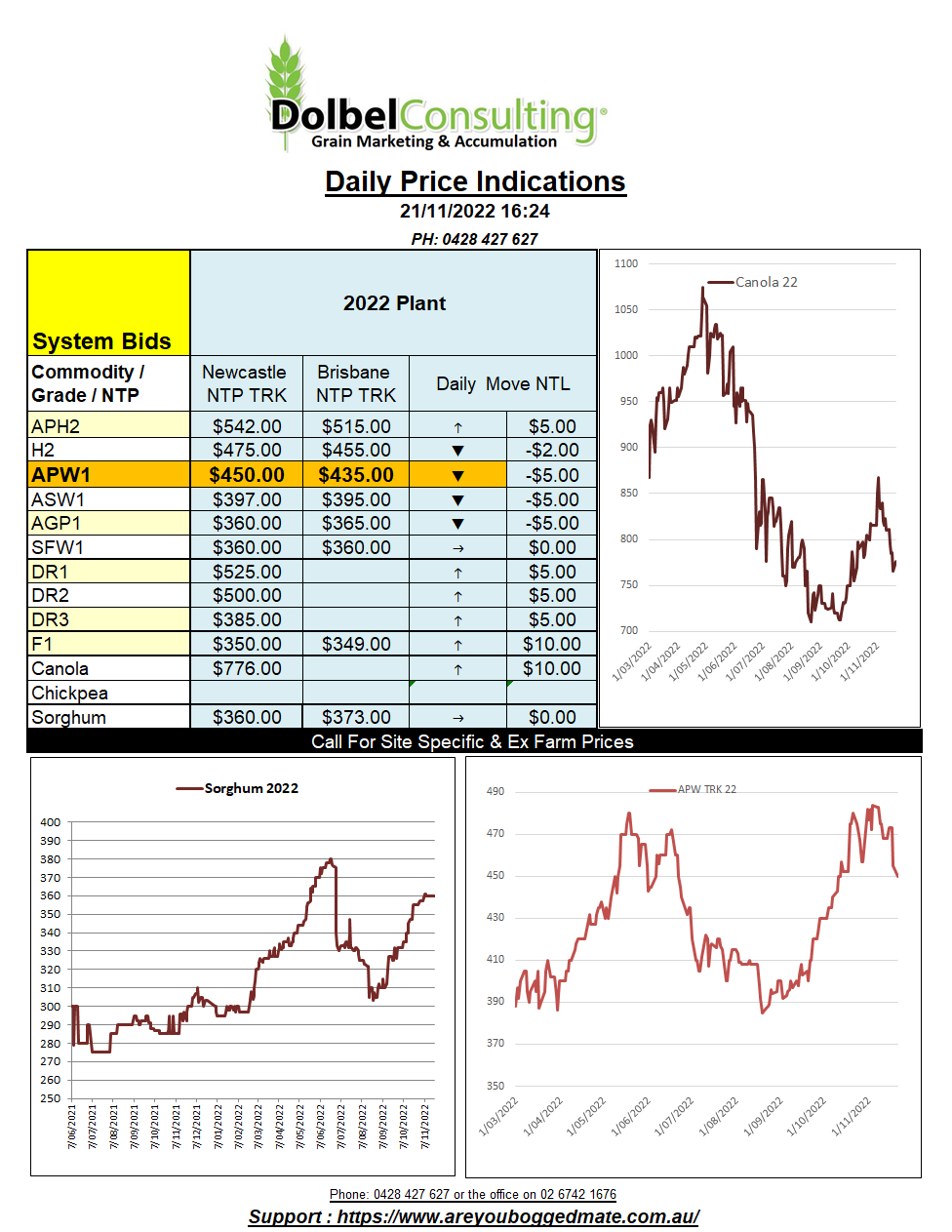

21/11/22 Prices

Chicago SRWW and HRWW futures closed lower again in overnight trade. Technically these two grades of US wheat look very oversold and are looking very likely to have at least a technical correction in the near term.

Fundamentally wheat is probably seeing as much positive news as it is bearish news. Australia is having some serious issues on the east coast. Quality looking very poor and potentially there will be a sharp decline quantity as the test weight of wheat ready to harvest is also slipping.

The bearish news is on the table, the continuation of the grain export corridor for Ukraine wheat was the major one.

Overnight Ukraine wheat offers out of the Black Sea were lower. Ukraine feed wheat was valued at US$273 FOB Black Sea. On the back of an envelope and using Asia as an end point this would roughly convert to an ex-farm LPP price of something close to AUD$400. The current bid into Newcastle of AUD$410, less road to the LPP, roughly AUD$355 XF LPP, does compare well and we shouldn’t see the Ukraine price pressure local feed wheat values. Ukraine milling wheat is valued at roughly US$350 CiF Egypt. Potentially rendering many exporters to expensive, including Australian H2.

US soybean futures found some support from bargain buyers and dry weather in Argentina. Strength in soybeans rolled through to a stronger close in Paris rapeseed futures but ICE canola at Winnipeg struggled to reflect the move and closed a fraction lower. A potential record soybean plant in Brazil continued to weigh over the oilseed market. There is also talk that the Argentine government will have another go at the soydollar to encourage exports. This gives the soy seller a better exchange rate than the spot rate…… that doesn’t fuel inflation at all does it.