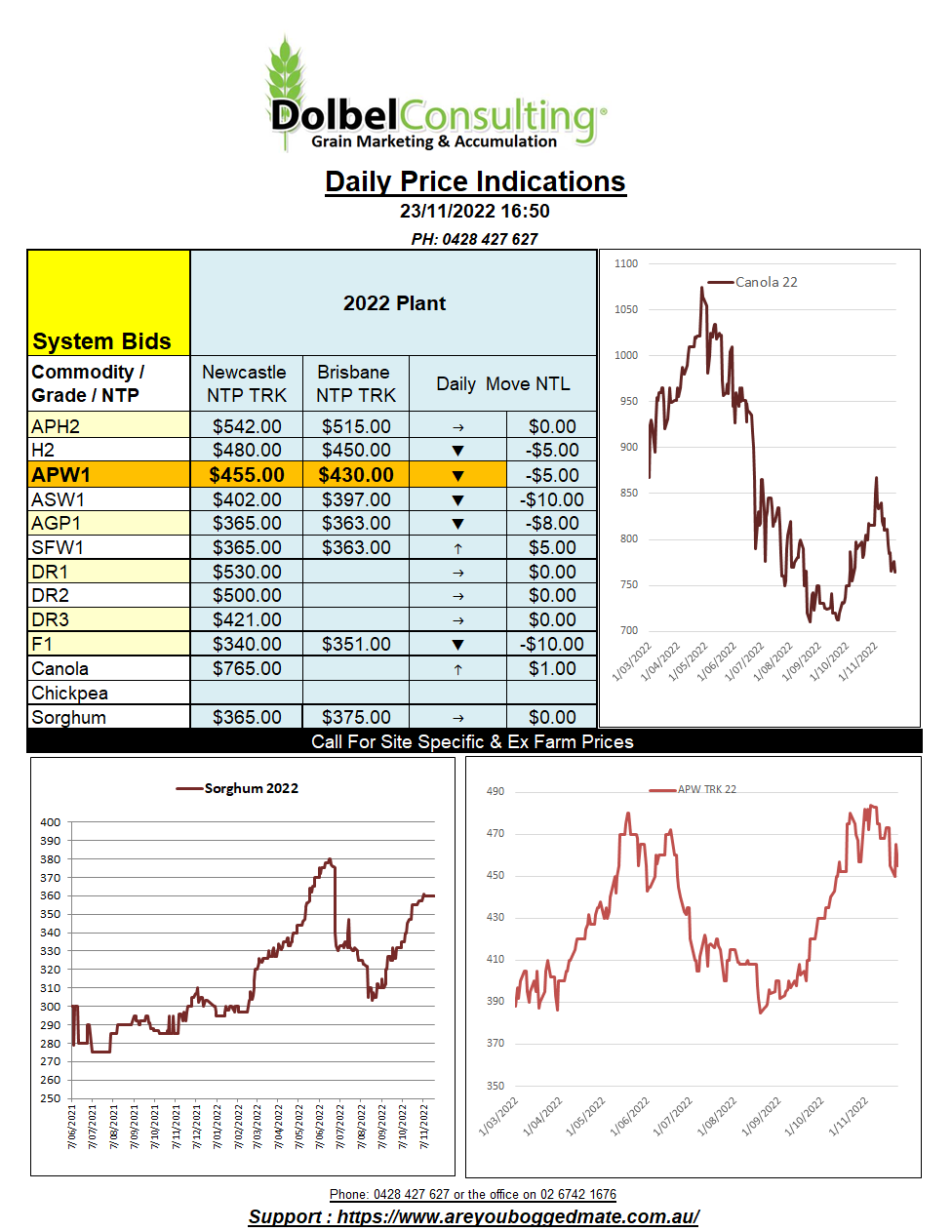

23/11/22 Prices

Chicago wheat futures and Paris milling wheat futures continue to move in opposing directions. Overnight all three US red winter wheat grade futures were slightly lower.

The US market seems to be getting comfortable with a winter wheat crop that’s rated just 32% G/E and is 87% emerged. This is a very poor start to their winter crop season, and they will need everything to go in its favour in their spring if it is to compensate for the poor start. The HRWW states are still the worse off with vast swathes of Kansas and NW Texas seeing little to no rain over the last two weeks. Nebraska and much of the Mississippi Valley can be bundled into that category as well.

US weekly wheat export inspections were 279,904kt, a nice increase from last week. Hard red winter wheat made up just 34% of loadings while white wheat attributed to 43% of total loadings. This is interesting as white wheat values out of the PNW were actually firmer last night. When taking the AUD into account WW moved close to AUD$5.00 higher.

Kansas topsoil moisture now rated at 43% very short, 32% short.

Meanwhile in Europe the MATIF milling wheat contract continues to climb, up AUD$4.26 by the close for the December contract. The March and May slots were also a little firmer.

US fertilizer prices continue to fall, now at US$500 for Urea NOLA.

Ocean rates are now lower, close to pre covid values. Container rates from China to the US are even lower. Is the China zero COVID policy hurting them more than they are letting on. Or have we seen significant supply and demand changes.