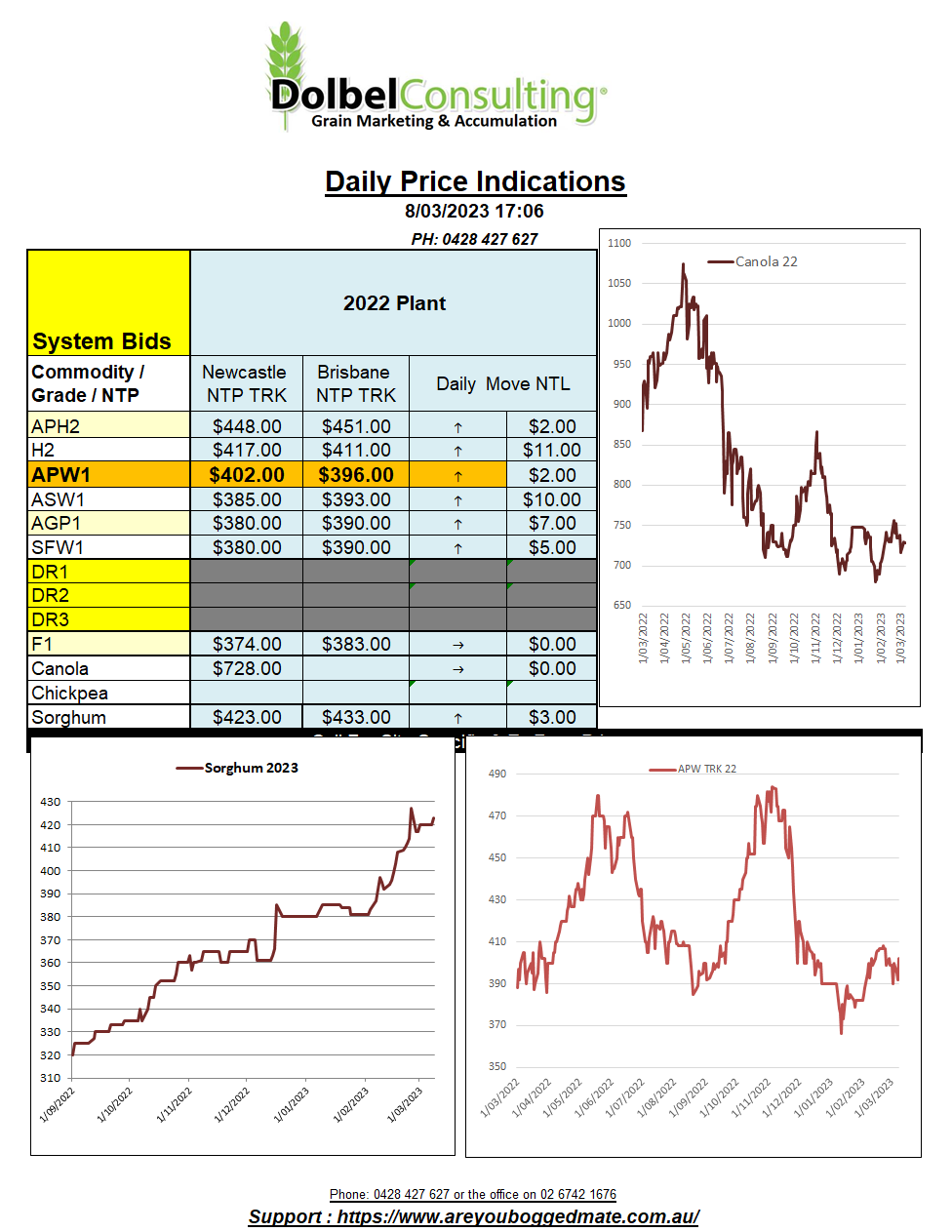

8/3/23 Prices

The move in the AUD will counter the sideways action in US markets. Fundamentally the trade is likely to wait this out to some extent and see what the USDA WASDE report has in store later in the week. The stronger US dollar may also put pressure on US futures markets. Recent reductions in US FOB values for wheat and corn had seen US grain start to make some inroads into Asian markets but the sharp increase in the USD overnight could bring all that progress unstuck this week.

Tunisia state grain agency has announced a tender for 100kt of durum wheat. Canadian exports have been brisk, even during the winter months when port access is limited. In this week’s Saskatchewan Ag report visible supplies were reported at 545.7kt. A little low considering this is usually when exports start to pick up for Canadian durum. The lack of a viable alternative from Australia has helped Canadian exports.

New crop durum in France is rated at 92% G/E, 9% better than the 5-year average condition for this time of year. Some punters are suggesting this is a big call given the current dry conditions in much of France. It is early days yet but the latest 7-day outlook from World Ag Weather does indicate that much of France could see 20-50mm, this unfortunately leaves some credibility to the rating.

Algeria will also close a 50kt durum tender tonight. Algeria will often buy much more than what the tender volume is noted as.

Jordan picked up 60kt of wheat at an average price of about US$315.30 for LH August arrival. Ameropa were the cheapest on offer by far, many other offers above US$320 and the highest at US$326.25 from Viterra. The winning offer equates to an Aussie ex farm price here on the plains equivalent to something close to AUD$330 – AUD$350, so Aussie wheat was never going to feature.