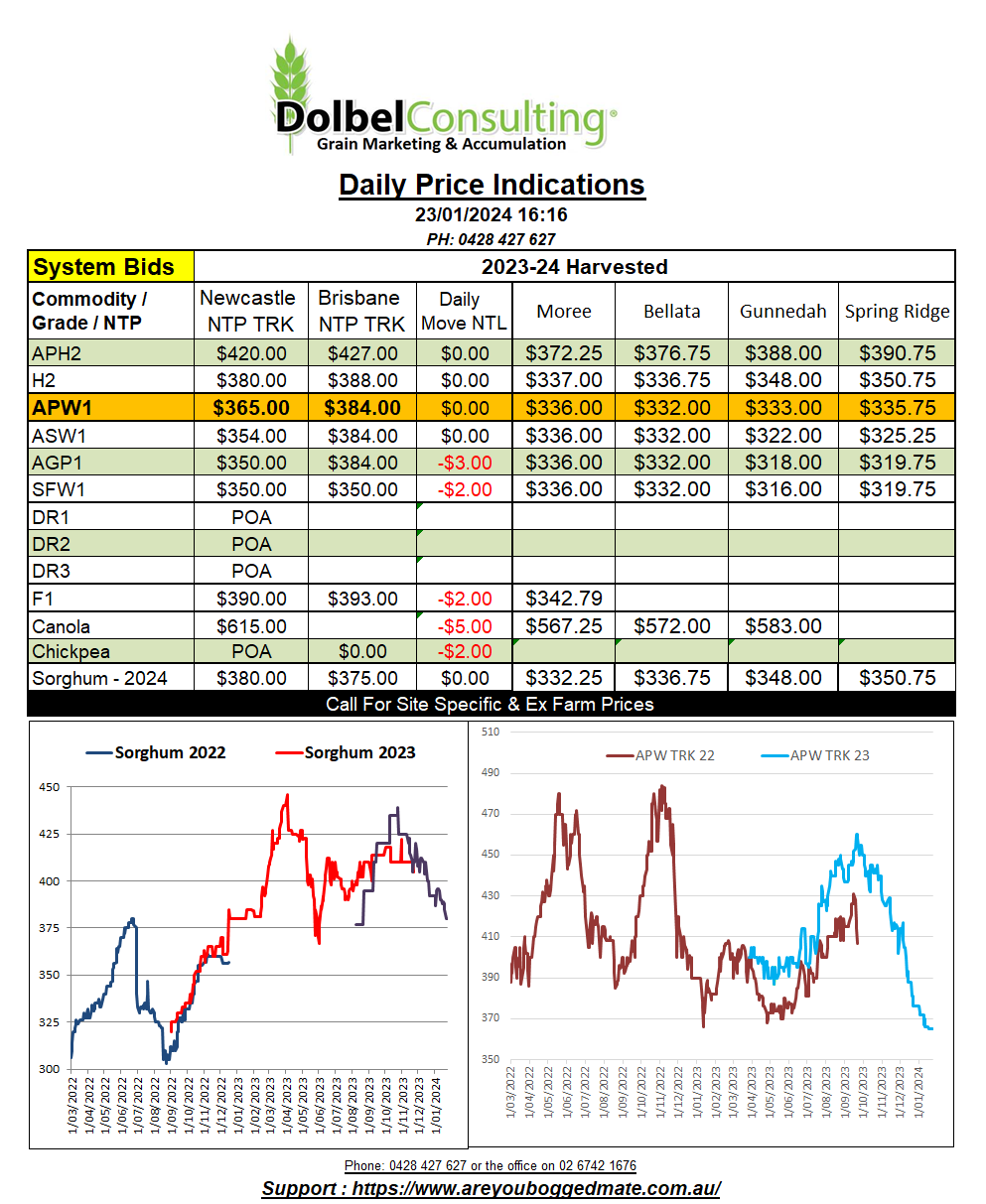

23/1/24 Prices

US grain markets were a bit of a non event last night. Wheat and corn futures remained generally flat, while soybeans were 10-11c/bu higher by the close. The stronger close in soybeans at Chicago rolled across to a better close for Winnipeg canola futures, up C$8.00 on the nearby and C$6.30 in the May24 slot. The March25 slot for Winnipeg canola futures closed at C$648.60, just C$12.30 better than the nearby, that’s poor carry. Paris rapeseed futures did not follow the US soybean futures or the Winnipeg canola market higher. Paris rapeseed shed E2.25 in the May24 slot, the Feb 25 slot slipped E4.25. Paris milling wheat was also a little softer on the day, shedding E1.50 in the May24 slot.

The thought that the early, rapid start to corn harvest in Brazil could lead to an increased area of second crop corn weighed a little on US corn futures. Until this thought is either confirmed or refuted, it may continue to cap any further rally in corn at Chicago, and could weigh a little on sorghum values too. With corn values as low as they are, this may influence producers in both Brazil and the US come spring more than the season.

The MARS forecasting team through a little fuel on the speculative fire for EU winter cereal production. After a wet sowing period the crop generally went in the ground in close to ideal, if not a little wet, conditions. Initial wet weather in France may have reduced acres more than expected, while dry weather in some other regions is now said to be becoming a concern. It’s yet to be seen if the sudden freeze early in the winter, when there was limited snow cover across some parts of Denmark has resulted in excessive winter kill. Black Sea conditions are also pretty good, but are currently very cold.

It’s probably still very early in the year to start speculating on northern hemisphere crop losses. We are better off keeping focused on the demand side to drive these markets in the short term. S.American exports, issues in the Red Sea and values out of the US PNW the major key indicators this week.