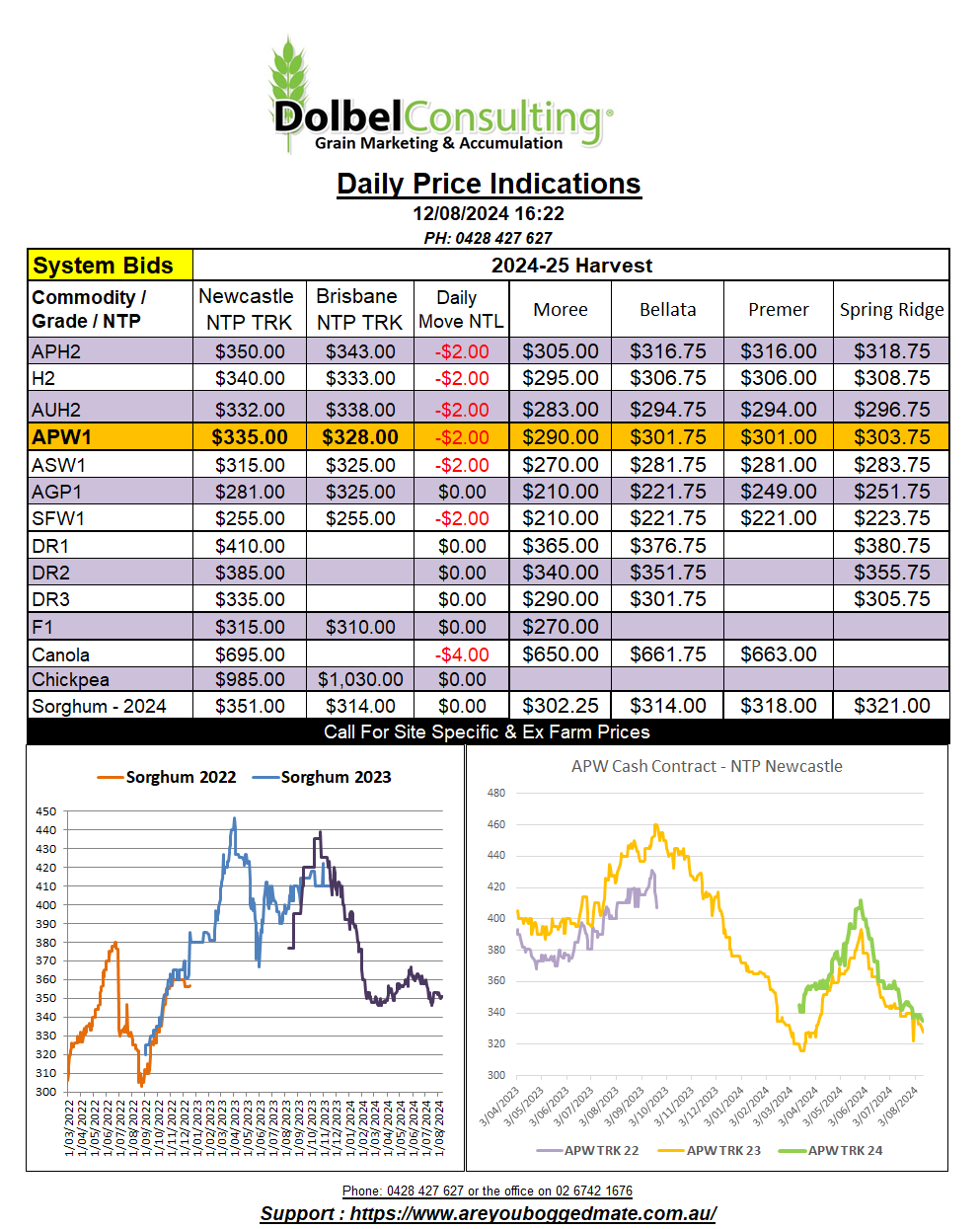

12/8/24 Prices

Week on week international barley numbers are mixed. The conversion from last week to AUD per tonne ex farm LPP equivalent price for many major exporters into both China and S.Arabia is loosely trending a little higher.

French and Ukraine values on an FOB basis are just over AUD$5.00 higher. Looking at values into the major consumers we see the average Chinese CiF value is mixed, from as much as AUD$7.00 lower to AUD$2.00 higher. Australian feed barley continues to be the cheapest option for the Chinese buyer. Values into the S.Arabian market were also mixed as Black Sea values showed some strength.

The best point of origin for the Saudi market appears to be Russia by a long shot. Australian and French barley are the next best, Australian barley now much cheaper than the French product and probably much better quality too.

Converting these barley values back to ex farm LPP equivalent values is a bit of an exercise in depression though. To remain competitive into these markets values would need to be well under AUD$300 XF LPP. WA farmers will continue to see discounts to eastern states for their barley no doubt.

Chicago soybean futures closed in the green, just. The same can’t be said for the Paris rapeseed contract or the Winnipeg canola contract, both exchanges shedding value, Paris after a couple of days of positive closes.

US wheat futures were a tad higher, nothing to write home about. The funds are still short and we have a USDA WASDE report out early next week. As is the Aussie cash bid, the US market also appears to be range bound. At least that gives us some confidence that the lows may well be in if nothing else. Fingers crossed that any potential move in US stocks and global production is now factored into the futures market.

No further news on the Egypt tender apart from we should hear something on Monday, what will be the biggest influence, the WASDE or Egypt news.