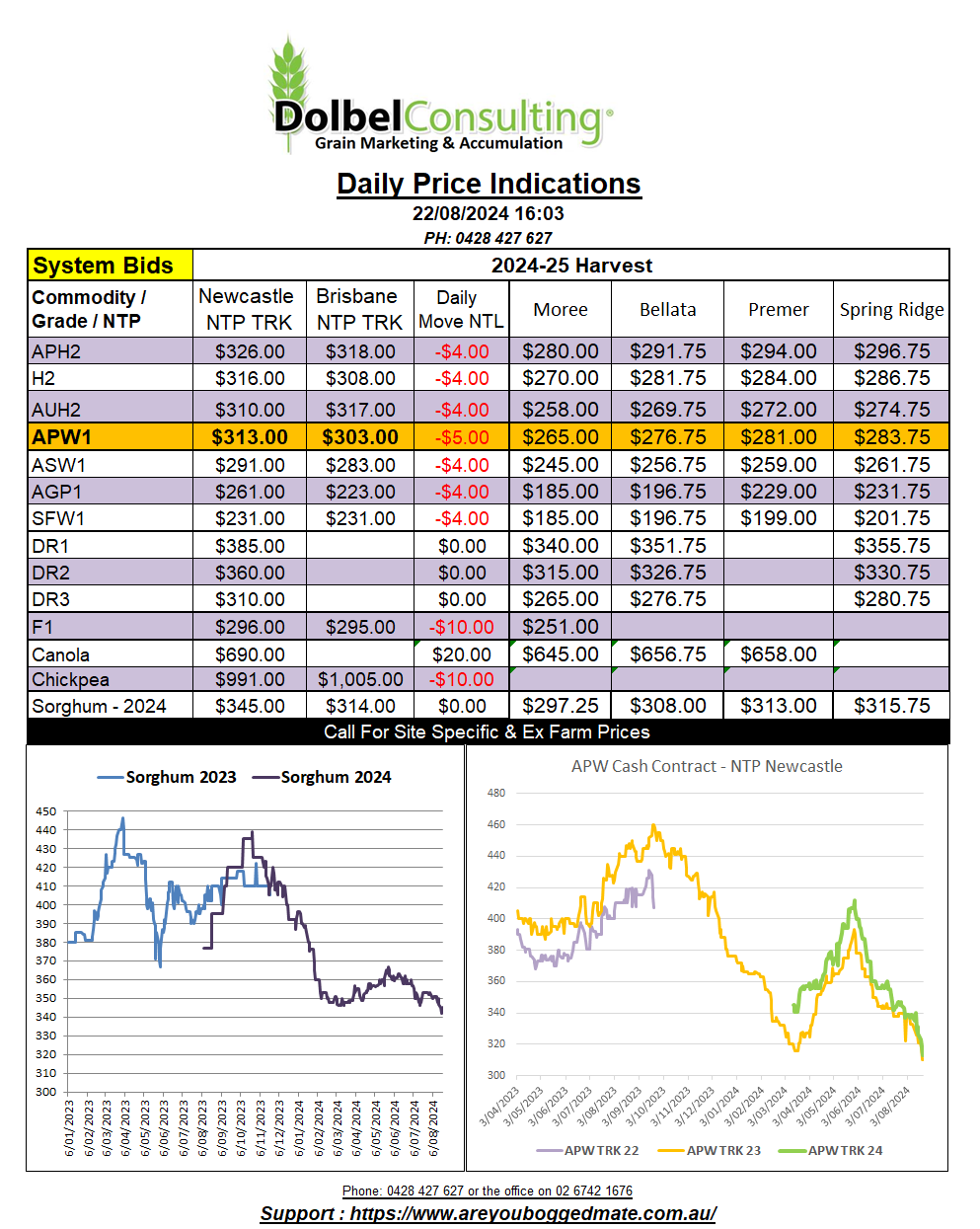

22/8/24 Prices

Paris rapeseed futures and Winnipeg canola futures had a nice bounce last night. Although Chicago soybeans were higher, the +5.5c/bu increase in the Jan25 contract doesn’t really indicate that canola / rapeseed futures were spurred on by the soybean market.

The general oilseeds S&D continues to indicate that a significant recovery in the sector is unlikely. Looking closer at the segment, canola / rapeseed in particular, shows a tighter global S&D due to the poor season in the EU, mainly France.

As the price of these two oilseeds falls lower, on the back of outside pressure from the general oilseed market. The viability of using canola as a feed stock for bio fuels becomes more realistic, adding further demand to the consumption side of the equation. At some point the additional demand will have a positive impact on values, and low prices will fix low prices, but it will also create some demand destruction if it rallies. This could potentially create a round bound market in the short term.

At the moment the downward pressure on canola values is generally outside influence. On the grower side we also see Canadian farmers happy to unload good volume. The marketing year for Canadian canola is just 1 week old and already the data shows disappearance at 665kt vs 320kt the same time last year.

This may just be growers and the trade getting stocks on hand / moving prior to the anticipated rail strike though. So we may need to take a little longer view on this data before we read too much into it. The rail strike, depending on how long it lasts, may produce some short term upside, but longer term stocks still need to move to market and the S&D doesn’t vary much, just the execution window. More stocks hitting the market in a smaller window is less than ideal.

Canadian canola production is estimated at 20mt, not a small crop. The EU estimate is just under 18.4mt, 500kt lower than the June estimate and 1.3mt lower than last year, but still higher than the long term average.

The price of canola is more likely to continue to be closely linked to soybeans, but also to EU demand in the mid term.