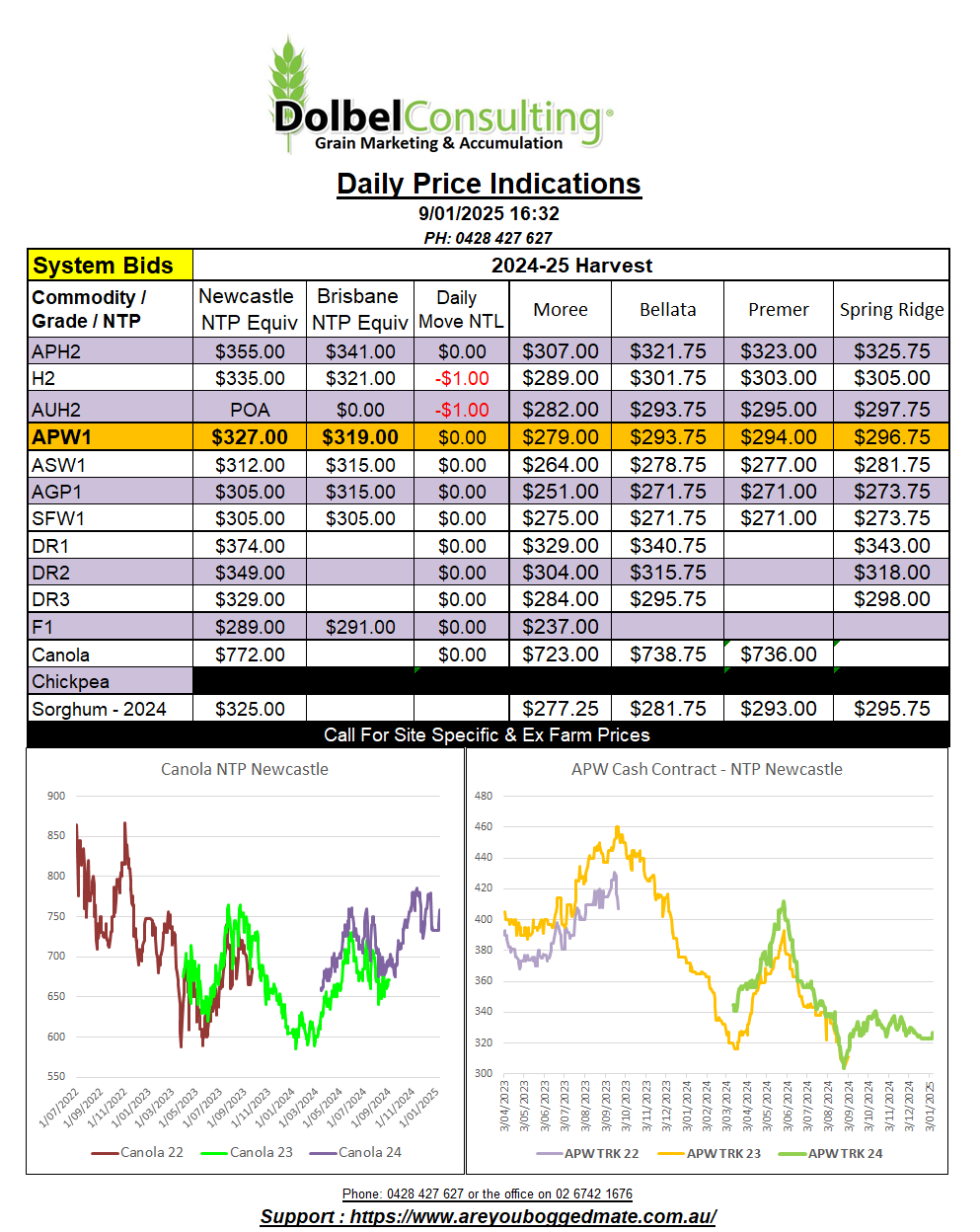

9/1/25 Prices

US wheat, corn and soybean futures all gave up value overnight. The stronger USD did not help US export values. Paris milling wheat, corn and London feed wheat futures were mixed, either side of unchanged, but generally a touch lower nearby. Paris rapeseed was again the biggest winner, putting on €8.00/t nearby and €7.75 in the May slot. New crop rapeseed futures were also higher, the Nov 25 slot gaining €4.00 / tonne. Strength in the Paris market spilt over into the Winnipeg canola contract. The nearby January slot and the March slot there closing C$6.80 higher, the May contract up C$7.80 /t by the close. In summary US futures did it the hardest due to the stronger USD while other markets saw less of an impact.

Global cash wheat values were generally mixed to stronger. EU wheat was stronger once converting to an Aussie equivalent compared to yesterdays conversion. Black Sea wheat was also a smidge higher when compared to yesterdays conversion. Argie and US cash wheat offers were lower. Out of the Pacific Northwest US spring wheat values were hardest hit, shedding roughly the equivalent of AUD$3.50/t compared to yesterdays conversion comparison into the Asian consumer. HRWW was lower by just under a couple of dollars per tonne equivalent.

The bargain hunters left the wheat pit at Chicago triggering a round of technical selling and profit taking. Fundamental news remains hard to find with conditions across the northern hemisphere benign, as is often the case in the middle of winter. We’ve seen some big export sales made over the last few weeks. The timing of these purchases couldn’t have come at a worse time to create some volatility though. Christian countries generally on holidays. With these big buys behind the market now it does tend to feel very sideways for the mid term, at least until the thaw in the north, generally referred to as the “silly season” in the grain markets.