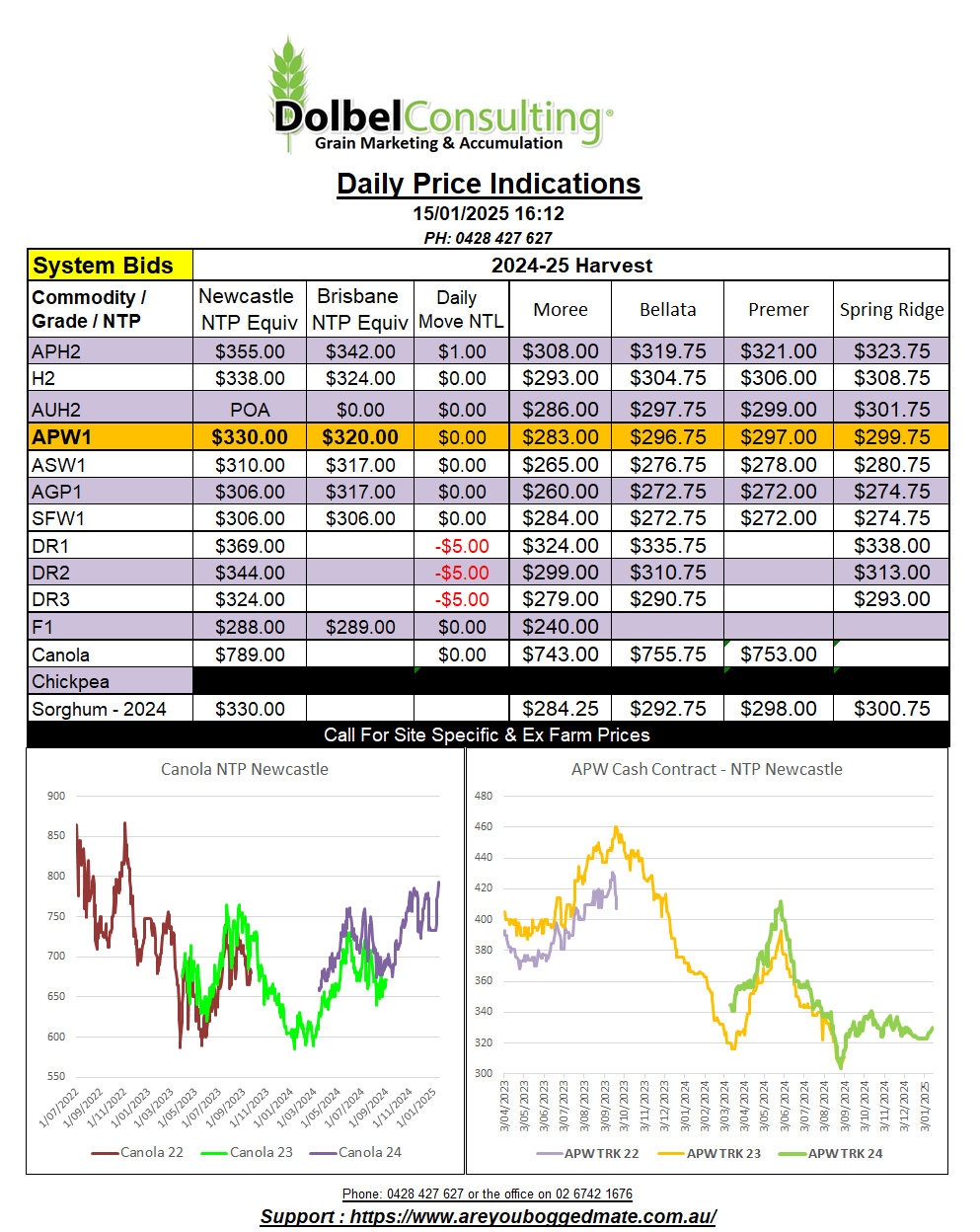

15/1/25 Prices

Technical trade dominated the US futures markets overnight. Profit taking was a feature in the corn and soybean pits while wheat was dragged along for the ride, generally trending lower in the milling grades. Paris milling wheat was softer, shedding €2.75 / t in the March 25 slot, and €2.00 / t in the December 25 slot. Paris corn and rapeseed futures were also lower. Rapeseed back €4.00 / t on the nearby and €3.75 / t in the Feb 26 slot. Winnipeg canola was a follower of both Paris rapeseed and Chicago soybeans. Falling as much as it gained yesterday, down C$6.10 / t nearby and -C$2.10 / t for the Jan 26 slot.

The AUD is at 61.92 this morning, trading to a high of 62.01 very early in the session before slipping away and then mostly climbing back towards the opening value late in the session. Some analyst are calling the jump in the AUD a dead cat bounce, time will tell, but there are no underlying economic improvements to speak of that are fueling the AUD recovery at present. The next question I guess, is will the RBA cut rates in Feb as most think they will, it’s not a given.

World cash grain values were mostly flat to lower. The AUD is having as big an impact on conversions as what any move in origin currency grain values is having. US Pacific Northwest cash values were generally back AUD$2.00 to AUD$4.00 compared to yesterdays conversion. With local markets shedding AUD$7.00 worth of basis yesterday there’s no real reason for local prices to follow this move lower. Since when has that stopped a good slaughtering of cash bids though. Russian, Ukraine, French and Argentine bids, in AUD / tonne, compared to yesterdays conversions, are all lower by a couple of bucks or less.

There are no fundamental issues that are likely to have a major impact on world wheat values between now and next months USDA report. The short term looks very sideways with more influence from currency fluctuations and political intervention, or should I say political interruption, in the grain market.