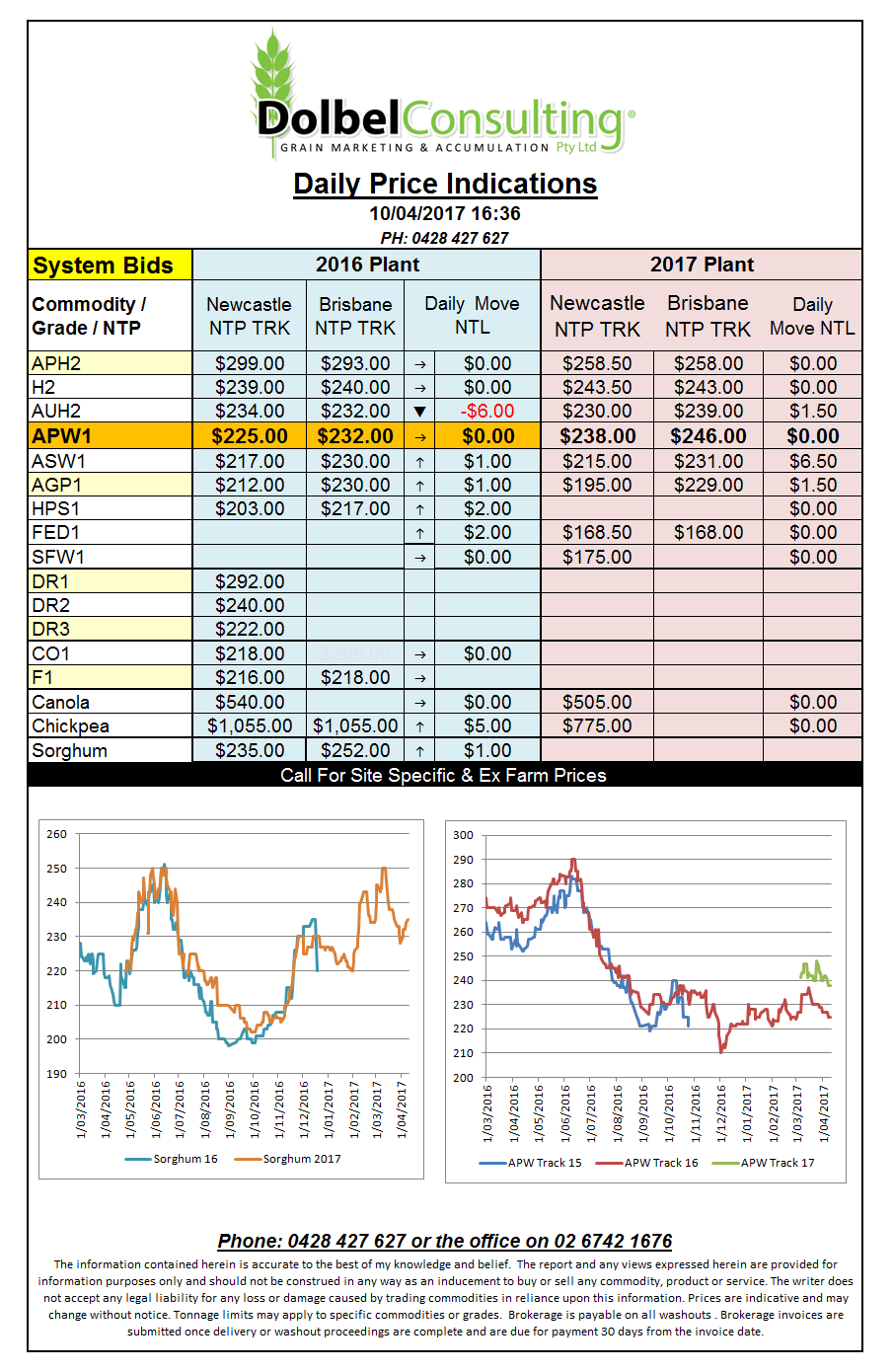

Prices 10/4/17

US markets are stagnating under the weight of fund liquidation of May contract longs and the continuation of good weather across most of the US major grain growing states. Next week’s WASDE report is expected to paint a slightly gloomy picture with ending stocks expected to rise for wheat, corn and soybeans.

Algeria picked up 570kt of wheat overnight, it was bought on an optional origin basis so not sure who the major supply countries are at present but there is some talk of US wheat getting a taste this time around. The general opinion is that France, the favoured supplier to Algeria, will get the lion’s share. The grade looks to be about H2 spec and prices were said to be between US$198 – US$198.50 / tonne C&F. If this is the case the price works back to roughly $40 under current H2 bids here. Algeria as a rule does not report tender details other than tonnage so it’s just trade speculation at present.

Soybeans are interesting. China has a huge number of outstanding sales with the US, about 2.3mt, that’s compared to 109kt this time last year. One might also assume that these outstanding sales are at higher values than what are currently being offered. China aren’t the only ones with big unexecuted sales, Mexico is also there for 1.13mt. Is Donald about to upset the apple cart would it be possible these “sales” might begin to struggle to be executed under all this rhetoric, oilseeds are getting interesting.