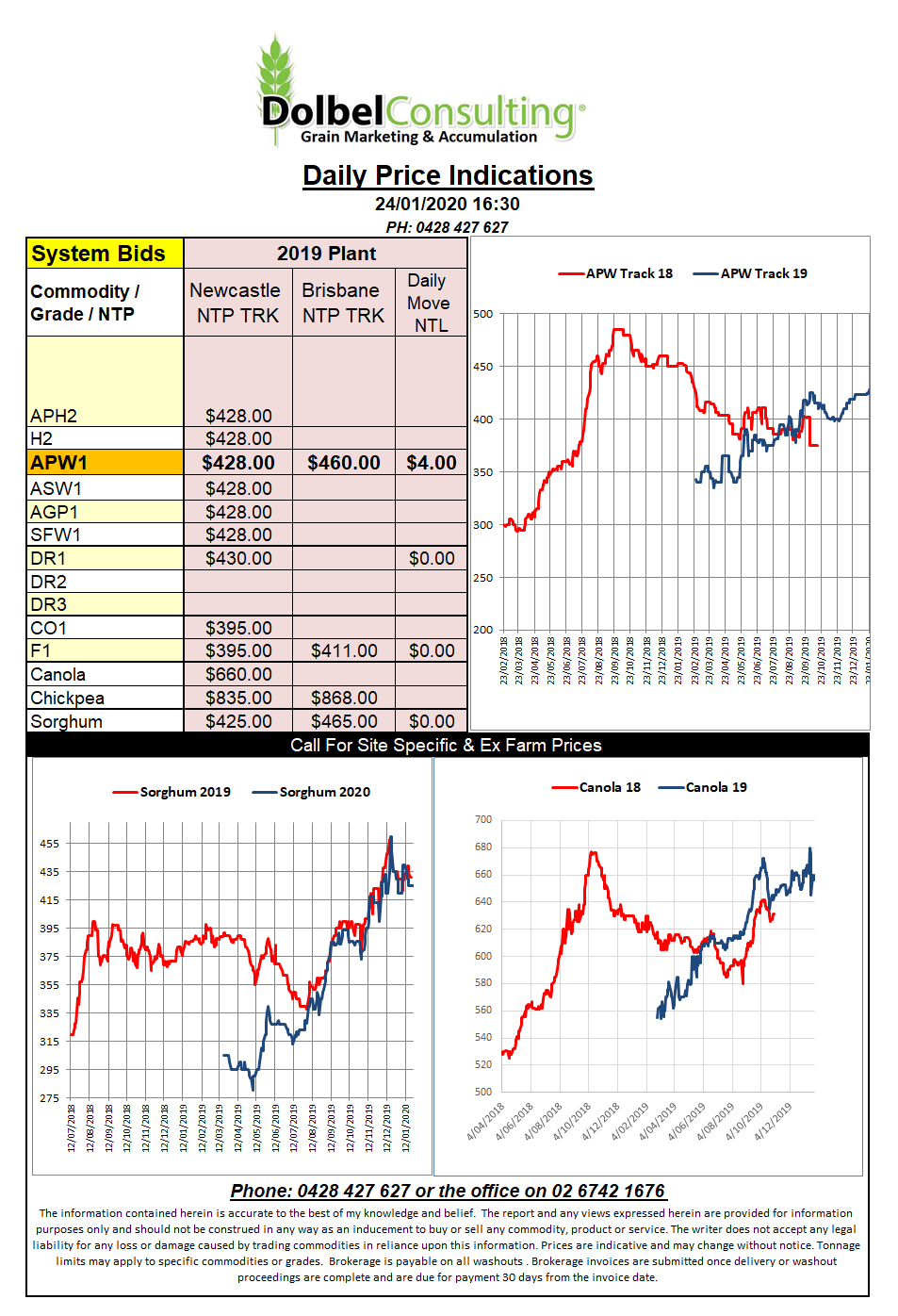

Prices 24/1/20

Chicago corn futures closed 5c/bu higher lending support to wheat values. Soybeans, thus canola and rapeseed, were both lower. The lack of a big Chinese purchase of US product is starting to weigh on soybeans at Chicago. Technically Chicago beans are oversold to buggery so don’t be surprised to see a substantial jump if or when a decent Chinese purchase is announced.

Talk of better than expected yields in the early S.American soybeans isn’t helping US price at present either.

US corn is cheap enough to compete into Asian markets but at present buyers there appear to be happy to pay a slight premium to pick up the better quality corn out of the Black Sea. The USDA said around 300kt of sales were reported yesterday, this has led some punters to assume that weekly US corn sales could be as high as 1.2mt, big call.

The IGC cut world wheat production 1mt to 761mt, unfortunately they also reduced consumption by 2mt, now pegged at 754mt. In order to keep prices moving higher we need to see a problem in one of the big three, Russia, the USA or the EU this spring. The EU had their “drought” recently but it’s been a while since we saw a major hiccup in Russian tonnage.

Japan picked up 108kt of wheat from the US and Canada in its weekly tender. This included around 20kt of US white wheat.