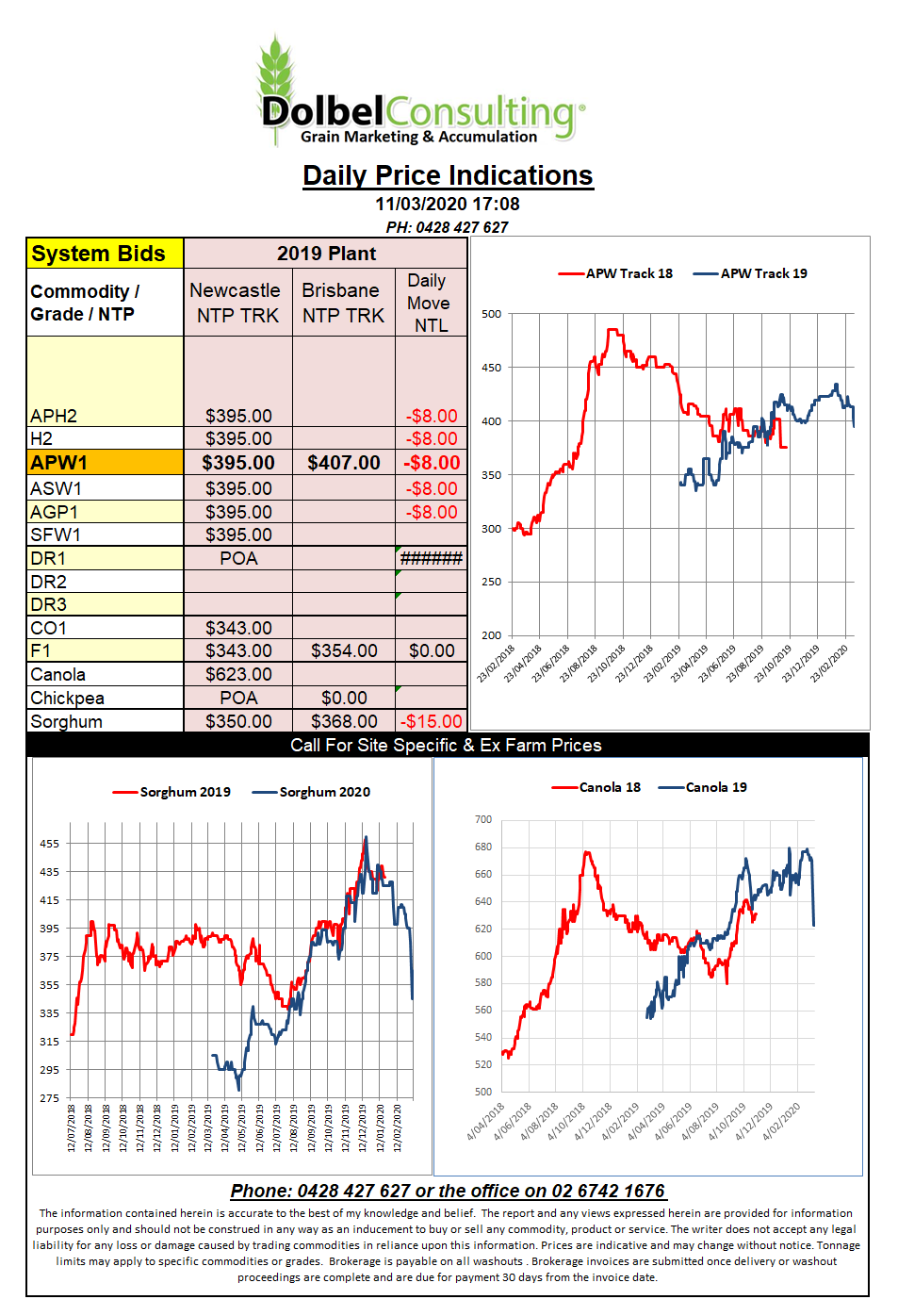

Prices 11/3/2020

A quick look at the USDA WASDE report that came out last night. Projected world wheat ending stocks were reduced a tad from 288.03mt to 287.14mt. They reduced Aussie production from 15.6 to 15.2mt and also reduced exports from Australia by 200kt, thus ending stocks slipped to 4.01mt, still dreamin.

Russian production was increased 110kt to 73.61mt but exports were increased from 34mt to 35mt seeing ending stocks coming in at just 7.4mt. There was a slight increase in world demand, mainly Asian, that’s getting harder to believe but with grain this cheap it may keep the order books full. World wheat production is pegged at 764.49mt which is the bur in the sock that everyone is trying to ignore. Increases is India and Argentina capped the market. This report leaves the trade looking towards the March 30th report for guidance.

US grain futures were influenced by the outside markets last night, predominately the oil and equity markets as the punters rush back to the States to park their US dollars. Crude oil made a US$3.50 / barrel recovery to US$34.53 / barrel. This lead both soybeans and corn higher and wheat tended to follow along. The charts also show wheat as a good buy and we should see further support throughout the rest of the week. With the Canadian dollar softer and support rolling across from soybeans the ICE canola contract closed higher. A combination of a weaker AUD and the rally in ICE canola futures would value the recovery at about AUD$13.00/t here. Paris rapeseed also closed higher but only E$1.50 on the Feb 21 slot.