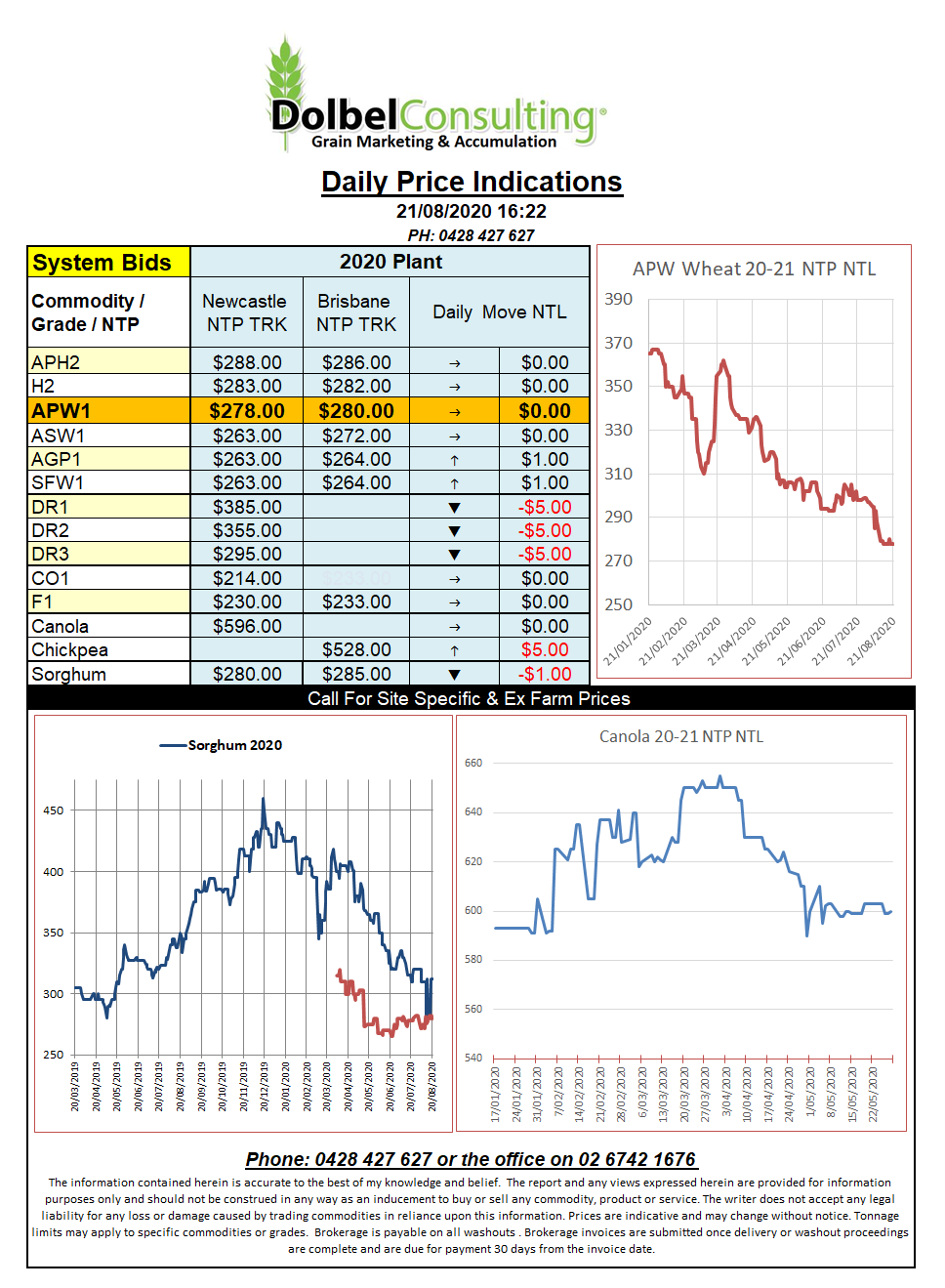

21/8/20 Prices

The question canola growers are asking themselves is “where does canola or rapeseed price itself out of the ration”. Currently we see canola markets well supported by good European demand and lower production across much of Europe and Canada. Although China is not taking much canola seed from Canada the demand for oil remains high thus the crush margin in Canada is good as canola oil heads offshore to China, tariff free. Europe, who looked east to Ukraine to fill the short fall last year may not find as much low hanging fruit in 2020. The Ukraine rapeseed crop is smaller. This should enhance the opportunities for Australia, currently this does seem to be the case with forward contract values at AUD$600 port +/- a few dollars indicating a great basis over ICE futures.

It does bring other oilseeds into the price matrix though. For instance this time last year the EU had imported 408kt of rapeseed, currently this stands at 216kt. Soybean imports are up 9% and sunflower seed imports are up 104%. In Europe rapeseed oil is trading at a big premium to soy and sun seed oil.

With Ukraine expected to harvest a record 17.5mt sunflower crop and Russia also producing a healthy 13mt of sun seed in 2020 the competition and thus the potential to cap the rapeseed / canola market may well come from the Black Sea region yet again. The Black Sea crops will hit the market around Sept / Oct, we may need to monitor local basis here leading up to that time, any reduction maybe a trigger for further sales to lock in what is now a very handy basis.

If US futures are a guide today, look for yet another sideways day, potentially firmer but factoring in Friday discounts, more likely flat.