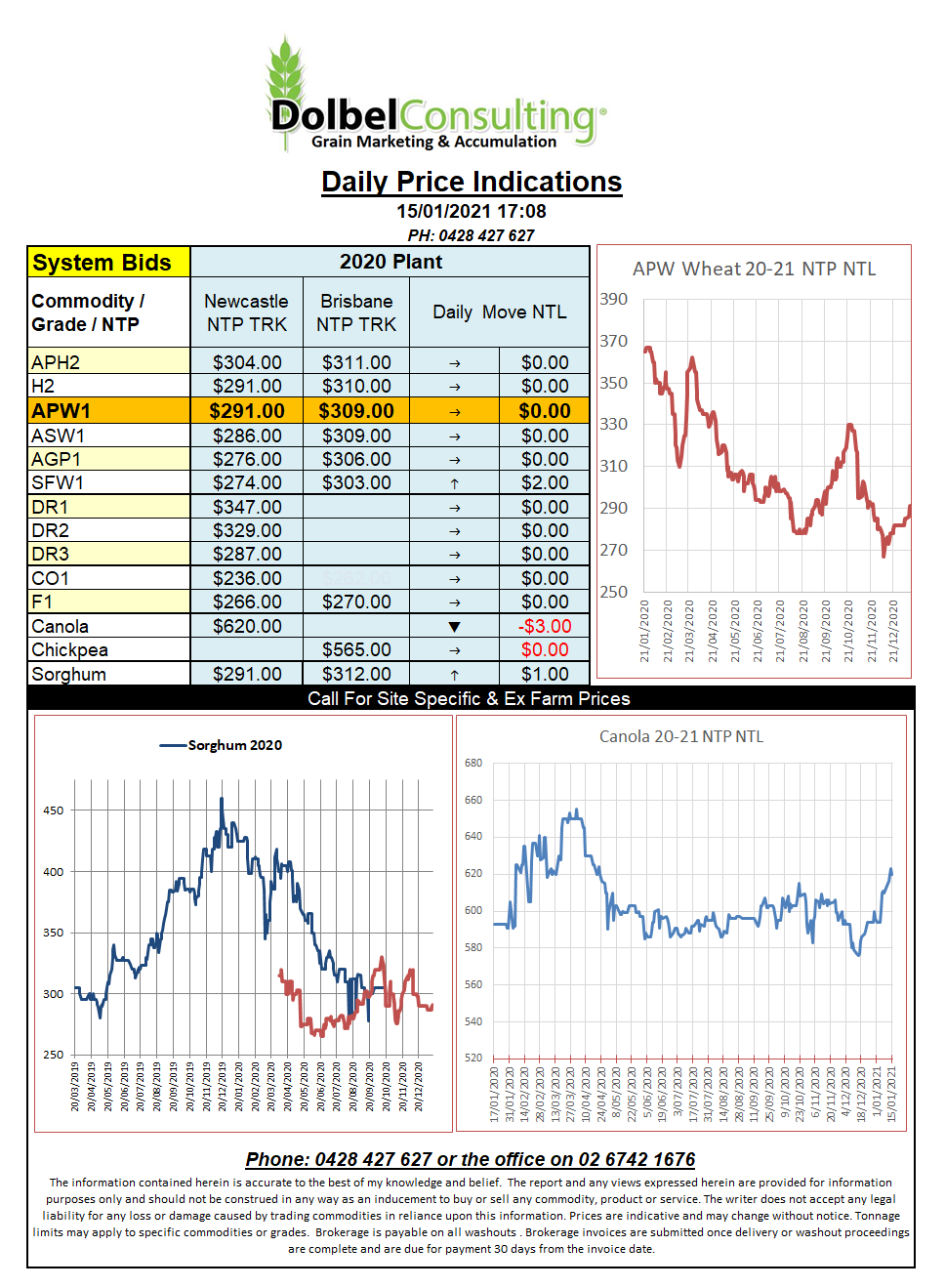

15/1/21 Prices

The International Grains Council, IGC, joined the list of analyst calling for smaller ending stocks for corn. This revived the rally in Chicago corn futures and at one stage had the May contract trading at 540c/bu. This might not sound that impressive but US corn futures, for the nearby, have rallied 115c/bu since this time last month, about AUD$58 per tonne at today’s money. All the while Australian sorghum values have fallen $10, and local corn, well you are still flat out giving it away but just maybe it’s time is coming.

Still on corn, world ending stocks are expected to drop to about 269mt. Just to put this into perspective China will own about 175mt of that ending stock, leaving just 94mt of corn stocks prior to the new crop coming in. That’s just under 4 months’ worth of consumption, so you can see why things are a little supportive for corn. If the China number is wrong, god forbid, or there is a (any more) major production hiccup, this time next year corn stocks could become very, very tight.

US weekly corn sales were 34% above the prior 4 weeks (holiday season). At 1.43mt this was better than any trade guestimates leading up to the report’s release. No prize if you guess who the No1 weekly export destination is, that’s right, China.

Wheat futures were dragged higher by the row crops at Chicago, I don’t know about being dragged kicking and screaming, there was a degree of technical support that saw all three US grades close in the green. US weekly sales were poor, they haven’t priced themselves out of the game so this may just be a Christmas hangover. US cash bids out of the PNW were sharply higher for club white wheat and soft white wheat. This should translate to better cash bids here today, it is Friday though so it’s a 50/50 bet if the local trade will follow this wheat rally.