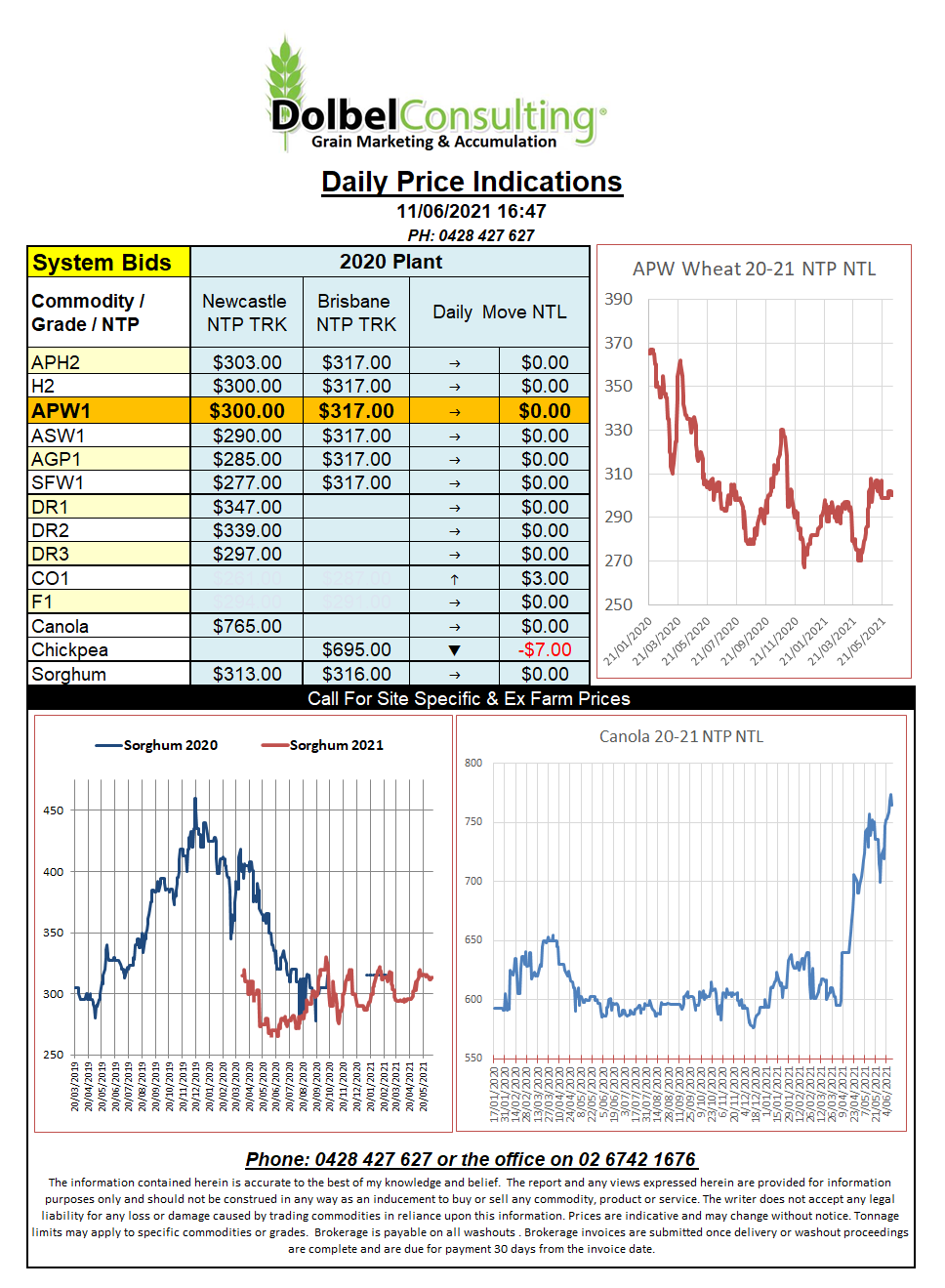

11/6/21 Prices

The USDA World Ag Supply & Demand Estimates report was out overnight. It was a bit “smoke and mirrors” when you get into some of the data. Corn seemed to be a winner, I’m not 100% sure why really, the data isn’t that bullish. The only real change to the 2021-22 numbers was the carry in, reduced by 2.93mt. This simply rolled through to a decrease in carry over as production and demand estimates were all left unchanged. The main change to the carry in was the reduction in US carry in by 3.81mt lower and once again no adjustments to their domestic production or demand / export estimates, bizarre really considering the shopping spree China has been on. I guess the big question is “was the 3.81mt reduction in carry over enough”.

Wheat carry in was also reduced a smidge with 1.19mt removed from mostly US carry in stocks and a few minor adjustments to Australia, India and Russia. Interesting to see both Canadian and Australian wheat production estimates left unchanged at 32mt and 27mt respectively. The net result for global wheat wasn’t really positive at all, in fact carry-over stocks were actually increased by 1.84mt to 296.8mt and production was increased from 788.98mt to 794.44mt, that’s 5.46mt higher.

The punters are technically over-bought wheat, if I was long Dec21 wheat futures I’d tend to feel a little nervous. Mind you this data could on the face of it be 30 day old data and not reflecting the unravelling of production potential in some locations like N.Dakota, Montana, and much of the Canadian durum belt. From the outside one might be able to offer fundamental support from this perspective but it may in time become an unsustainable argument. A put option if nothing else may offer some form of sleeping pill.