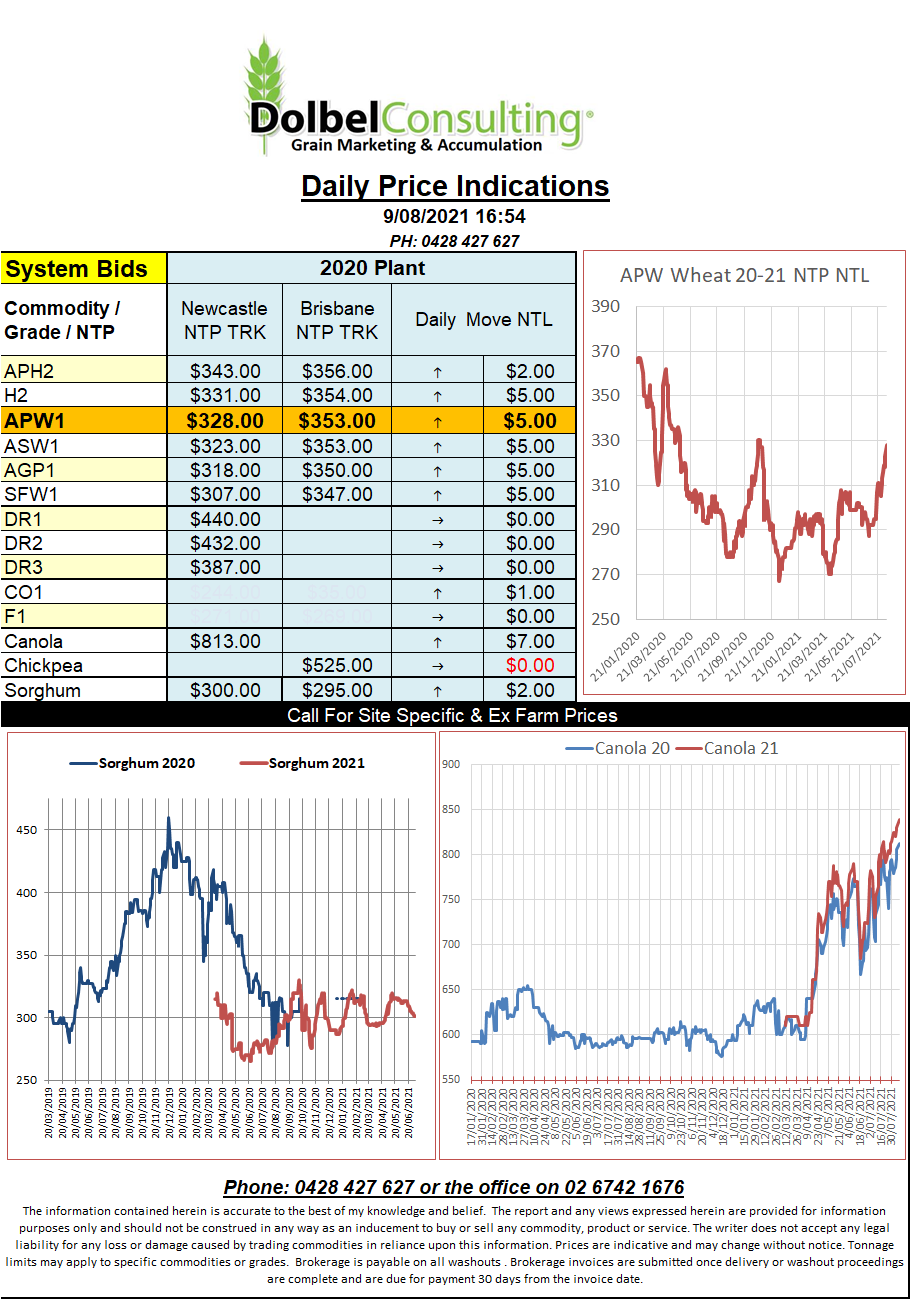

9/8/21 Prices

After a couple of days of lower closes technical traders push back into the US wheat futures market as buyers, now deciding that fundamental strength is the guide after a number of major producers reduced production estimates during the week.

Locally we see Australian production remain strong with some analyst projecting wheat output at 32.756mt. Quite a lot considering the cold, wet winter has stifled tiller development in a number of locations. The constant wet also saw fewer acres sown than hoped in the summer crop belt as well. So I guess what I’m saying is there is probably potential for Australia to just this list of major producers reducing estimates as we move through our spring.

The big moves overnight were once again in canola and durum. Looking at the SE Saskatchewan ex farm bid for 1CWAD13 durum of C$538.07 per tonne and using somewhere like Japan as a consumer point we come up with an equivalent delivered Newcastle port number of roughly AUD$640. I’m not saying we will see this number here or better but it certainly indicates just how much strength is in the durum market as Canadian buyers scramble to get coverage.

We also saw Paris rapeseed futures push higher overnight following the lead from both the soybean futures pit at Chicago and ICE canola futures. The Feb 22 Paris contract closed at E536 per tonne. That’s E36 / tonne higher than what it was at the beginning of May.

Looking at US dark northern spring wheat offers out of the Pacific North West we seen the 13% product offered at roughly US$389FOB. If this was to move to Japan and we benchmarked Prime Hard of this price it would come in close to AUD$480 delivered port equivalent.