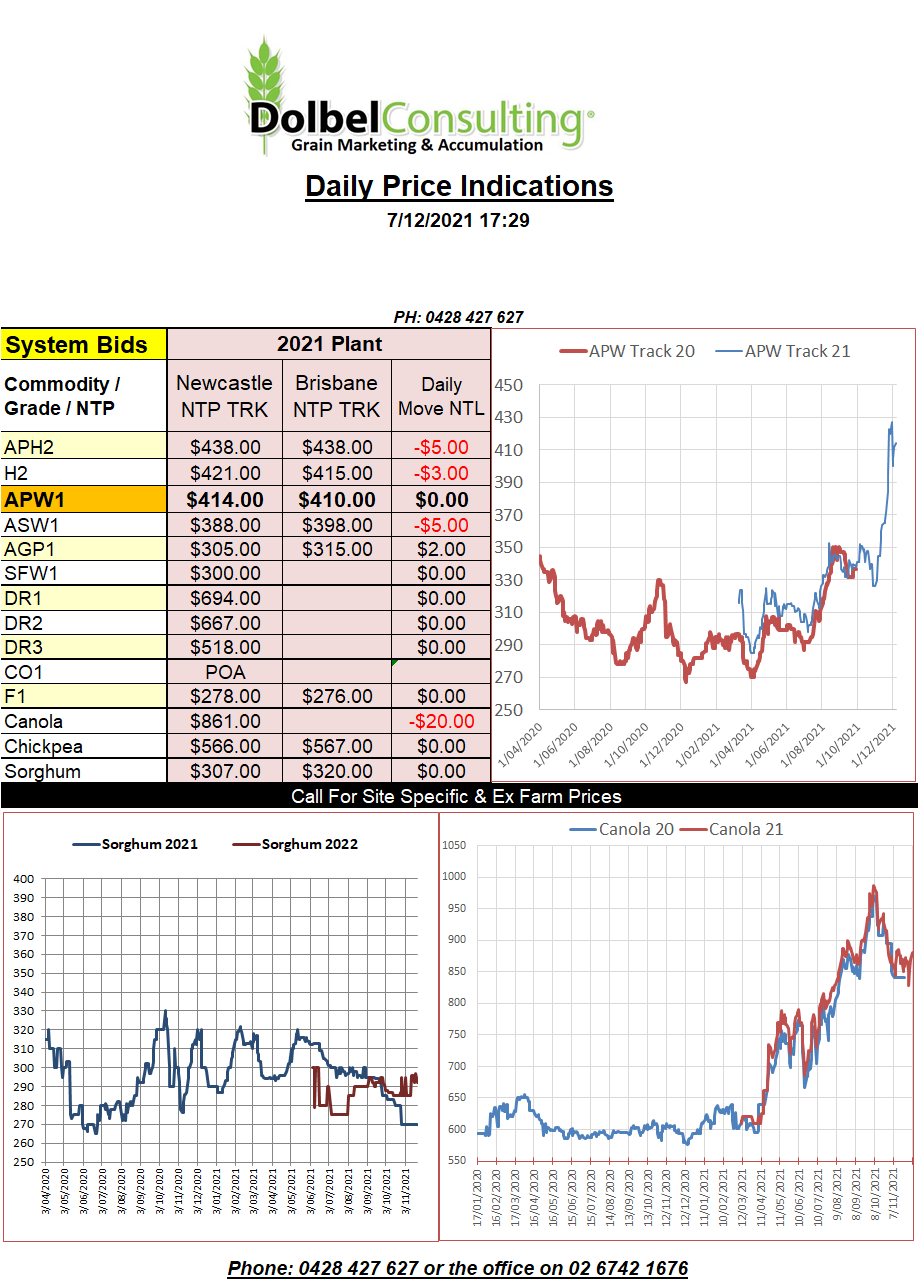

7/12/21 Prices

Saudi Arabia confirmed the purchase of about 689kt of optional origin milling wheat with a delivery period of July 2022. The price paid was said to average about US$365.14 C&F, around US$12 under their previous tender results in early November. Louis Dreyfus featured heavily in the purchase with Olam, Holbud and Cargill also picking up tonnage. Supply can come from a number of ports including Black Sea, EU, America and Australia at the sellers option.

The average price is comparable to an ex farm LPP number somewhere around AUD$380 less trade margin. Currently we see eastern bids for H2 wheat at about AUD$455 delivered Newcastle and APW bid at $425, odds are NSW wheat will not be used in this tender. With WA producers offering at even higher values for WA APW1 wheat, it appears unlikely Australian wheat will feature in the final divide.

US soybean futures finished the session lower after choppy technical trade. The general sentiment was lower with the sellers finally winning out and Chicago soybeans closing the session back just 5.75c/bu on the Jan22 contract. The spill over into canola was minimal with Paris futures slipping E2.75 and Winnipeg canola closing up C$2.70 per tonne. Cash prices for canola around the world were mixed, Canadian FOB offers appeared lower but volume is now small and prices do appear to fluctuate a lot at the port level. Black Sea prices were firmer, probably a better indicator of where the EU market is trading than either Paris or Winnipeg futures and Canadian port price sheets at this stage.

Durum prices into the Mediterranean market were hard to find but what numbers that were public, were generally softer.