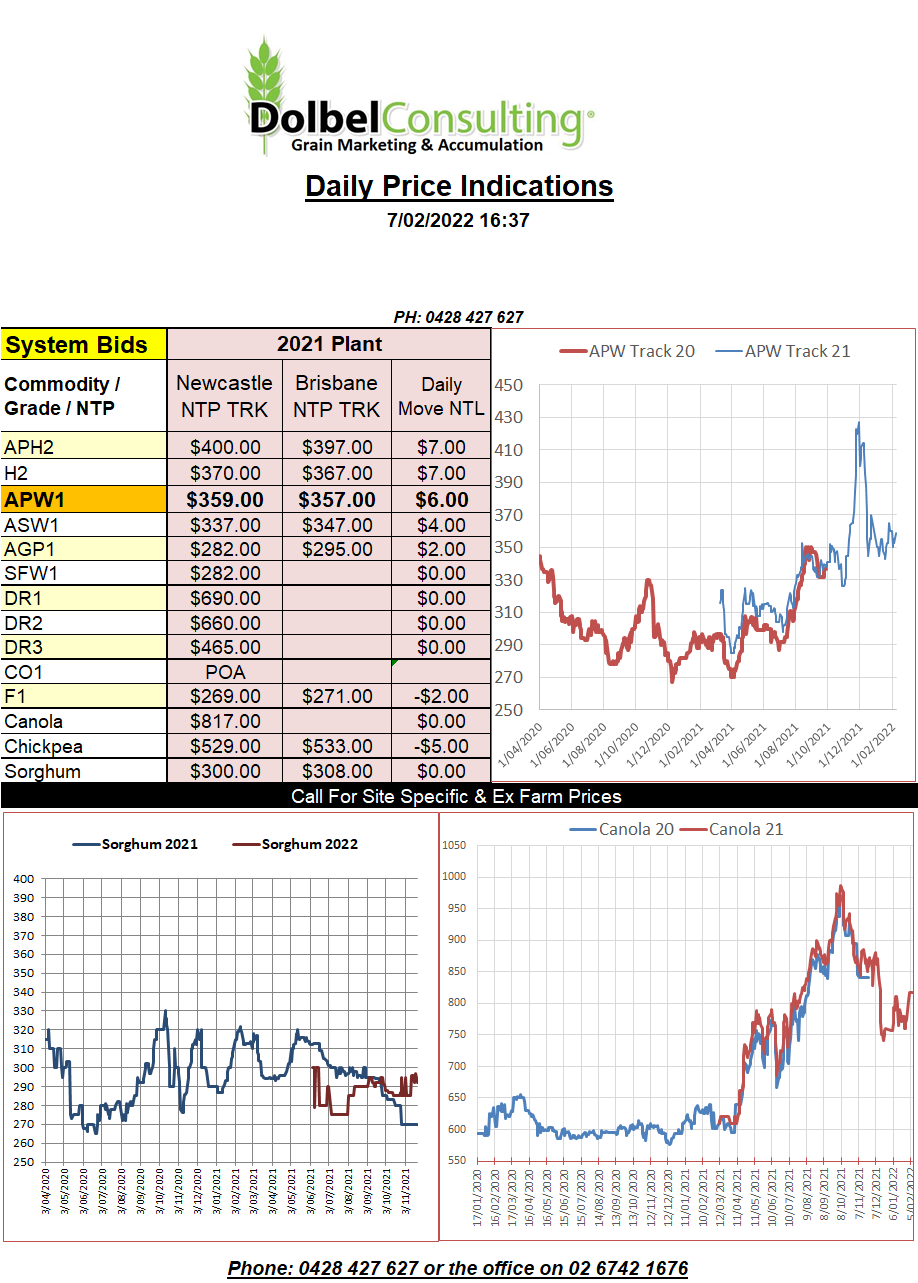

7/2/22 Prices

South Korean Major Feedmill Group, MFG, purchased up 110kt of feed wheat overnight. Reports expect to see supply of 55kt from India and the balance potentially coming from either the US PNW or Australia. I’d be backing the later on the second 55kt. US quality out of the PNW was generally very good given the dry finish. Price was reported as being around US$330 C&F.

This compares roughly to about AUD$370 delivered port for feed wheat out of Newcastle. Locally we are seeing SFW1 values at AUD$265 ex farm LPP or $315 delivered port. The delivery slot for the above sale, if supplied with Australian feed wheat would be 15th April / 15th May. This may be signalling a slightly firmer SFW1 market in the mid-term.

A quick look at World Ag Weather shows weekly US rainfall was a little further to the east than expected. Texas getting some good falls but much of Oklahoma and Kansas seeing little rain. A drying pattern across Nebraska and Iowa is concerning. The Texas panhandle remains exceptionally dry. Argentina is a mixed bag but generally in better shape leading into Autumn that it was leading into summer. There are still a few dry pockets in the NE but much of the major cropping districts have now seen some good rain. Brazil has pockets of above average rainfall, good for soybeans, but also now shows an increasing number of dry regions across the major corn / bean producers.

Europe remains very dry in the west, France, Spain, the UK, Italy and much of west Germany are now very dry. France in particular needs to be watched with many regions showing a 30 days rainfall anomaly of <40%. Russia appears to be having a dream run, Ukraine is a little dry but nothing to be concerned about. China is good apart from some dryness in the far north summer crop country, not a concern at present.