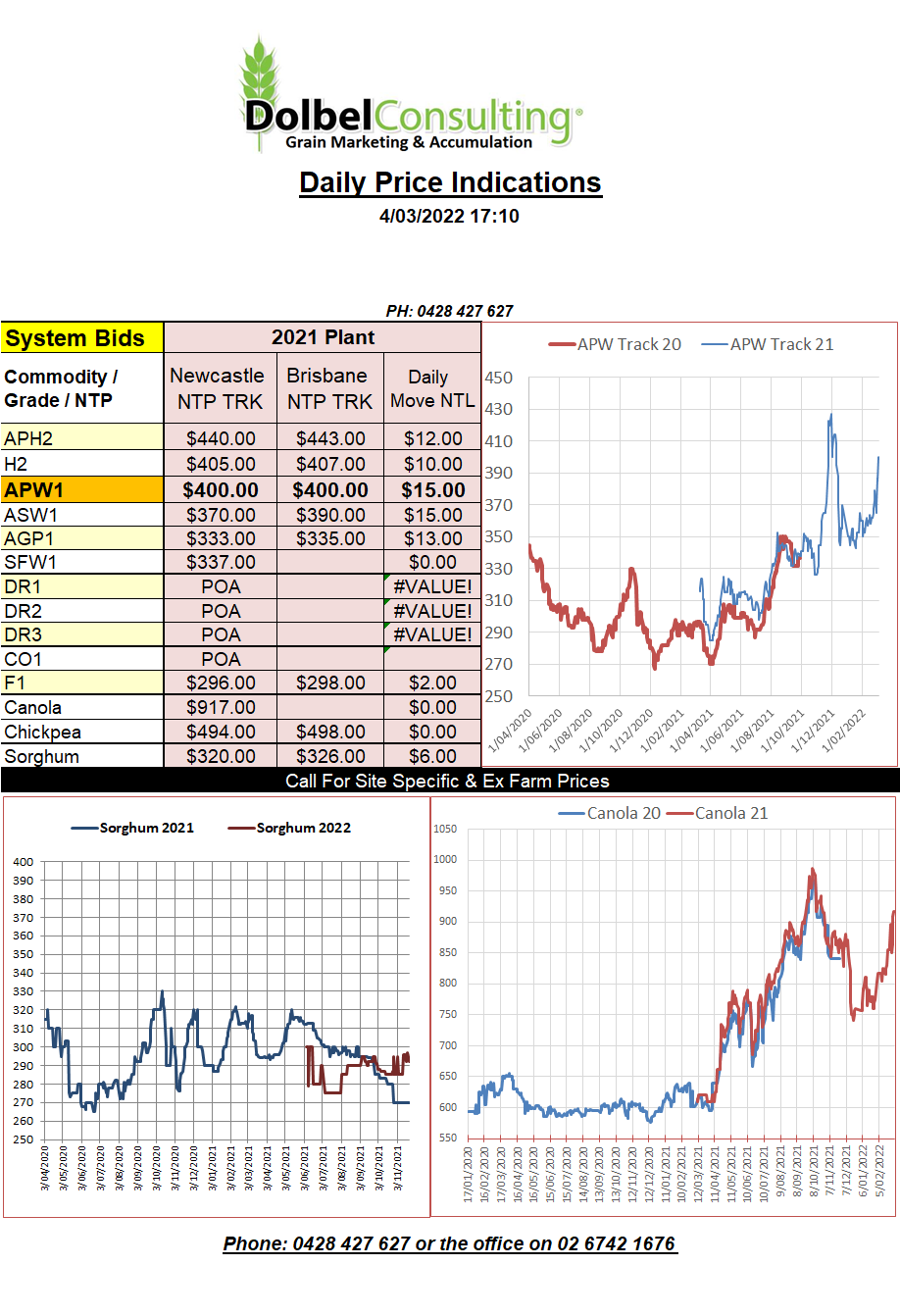

04-04-22 Prices

How would you like to be short a few thousand March 22 Chicago SRWW futures contracts this morning. A 235c/bu move higher might take the edge off the morning coffee (heroin maybe). Short and caught, so this is how grain futures converge with the cash market, mmmm yes, OK, I see.

The May22 contract was only up 75c/bu. We are now at 14 year highs after wheat futures in the US rallied 28% in 4 days. Not a bad return but it makes predicting markets and budgeting for this year’s crop a little difficult. The way input prices are going up you will probably still net the usual 2.5%, don’t ask me of what value though. I guess 2.5% of $500 / tonne is better than 2.5% of $300 though. The worst thing about farming is you could be picking the highest input price at sowing and the then the market tanks itself before harvest.

The US isn’t the only place wheat prices are heading the right direction though. There is talk that Chinese values are also sharply higher at the domestic level. Pushing through Y3000 (AUD$650) per tonne. A quick look at some FOB values for No3 grade Chinese wheat confirms this, Guangzhou priced at Y3177 and Tianjin Y3023. Corn futures at the Dalian commodities exchange closed at Y2885 / tonne (AUD$624) for the May slot yesterday. We also see durum wheat at US$500 C&F Chinese port.

Initially the FOB wheat markets were not responding as quickly as futures markets and many believe that the cash market will not trade to the same values as the futures market but when you see Chinese values creeping up to these levels at the port and internally it does give one hope that there is a little more upside here yet. For instance, if sorghum was to trade at parity to US corn, which is C&F China US$407, it would compare to a price of roughly AUD$470 at the port before costs and margins. Granted traders may need a large buffer in this environment but it tells me AUD sorg is cheap.