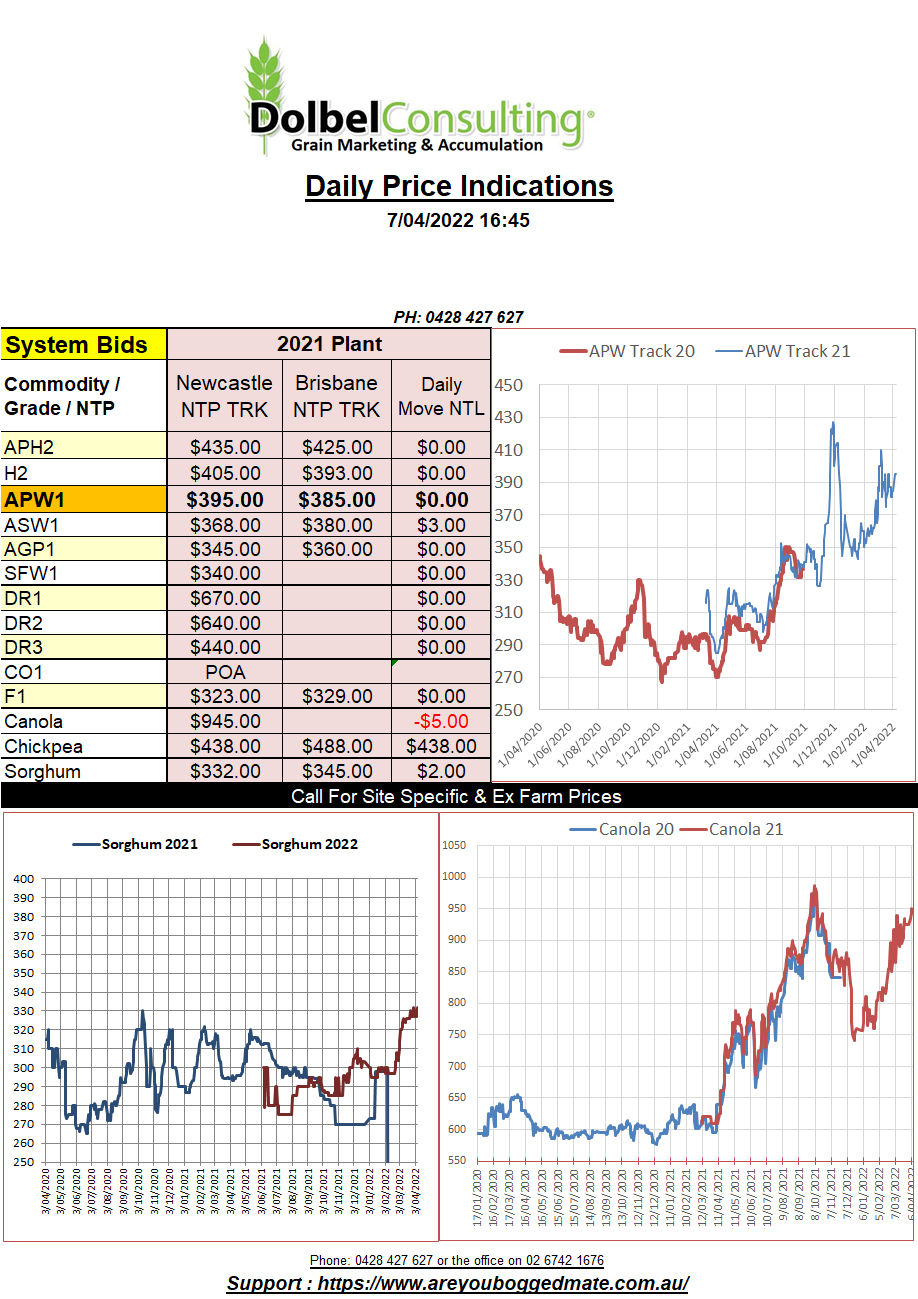

7/4/22 Prices

As the USA cranks up their summer crop planting program for spring wheat, corn and soybeans. The current supply chain and pricing issues around fertilizer, spare parts and chemical supply has a few of the analyst wondering if the US will actually achieve the projected areas sown as suggested in the latest USDA prospective planting report.

Although US wheat prices were lower overnight the sell-off was thought to be basically just technical profit taking after a 60c/bu rally in two days. Fundamentally we still have the Black Sea war, poor crop ratings in the US and the above mentioned input issue continuing to support current prices. The slight decline was evident in most grains, corn and soybeans all back a little, as were soft red winter wheat futures and US spring wheat futures. The poor crop ratings for HRW in Kansas trumped the technical sellers and prices gained a smidge by the end of the session.

Looking at the US futures markets for wheat, where world prices are and where grain is shipping from into recent sales is starting to see the odd analyst ask the question “what is wheat really worth”.

In Australia we have been substantially insulated from the “rally” in “world” values. Local basis was crushed, trading at the lowest discount to US futures I can recall. So the question here is, where are our values compared to where global analyst think wheat prices should be. How does the current price here compare and are we in for less of a rude shock than somewhere else that has seen speculative pricing push wheat values sharply higher without the fundamental increase in export volume one may have expected to see. Russia has continued to export wheat throughout the war with Ukraine, 2.2mt in March, almost average export volume. If the current world value is fundamentally closer to US$300 than current “values”, prices here shouldn’t be devastated (probably lower yes) if the Ukraine / Russia war comes to a halt in May like some have suggested.