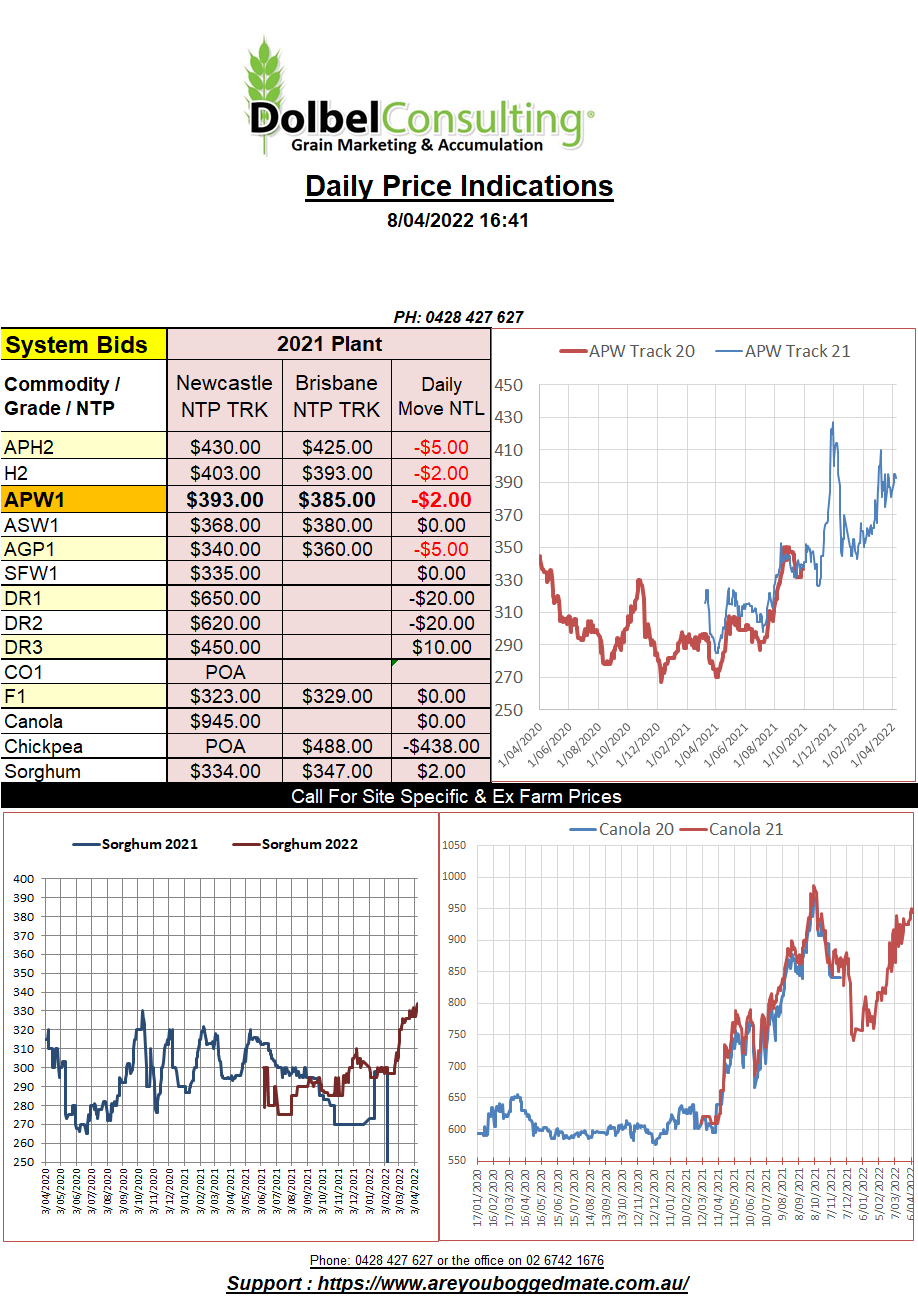

8/4/22 Prices

It’s a strange world out there at present, skimming through headlines is simply an exercise in futility. Today I can look at an analyst report and see one story about Brazil increasing wheat production so as to become a net exporter. While on the same page there’s also a story about how Argentina will sow less wheat as the input costs are too high.

Fundamentally things are pretty much unchanged. Russia continues to disrupt grain flow from the Black Sea, Ukraine continues to struggle to sow spring crops, N.Africa continues to talk about how they will one day become self-sufficient, dry weather persists across the US HRW and spring wheat belt and up into Saskatchewan, France is a little drier than it’d like to be, but the crop ratings are all great. China appears to be having a great run, a little wet in the east and a little dry in the west. Russia is as close to having a dream run as Russia can be. Russia’s economic side probably not as predictable as the agronomic side just yet. Turkey is dry as is much of Iran, Pakistan and India.

Tunisia have increased their domestic values for durum in order to encourage increased sowing. Their aim, like most Middle East and N.African nations, is to become self-sufficient. The agricultural minister has said there will be an increase in the price of durum from AUD$389.50/t to AUD$582 per tonne. The underlying price of barley will also be increased from AUD$300 to AUD$358 per tonne. I’m not sure if the agricultural minister there has looked at input costs of late. Lifting the price of durum is not the only promise made, adjustments to logistics and storage are also suggested, what they are is yet to be confirmed. The initiative is expected to pull another 800kha into durum. What does this mean to Australia, well potentially a better floor price into N.Africa when they have a drought or production issue, potentially narrowing the spread to DR3 as a result, or am I just being optimistic.