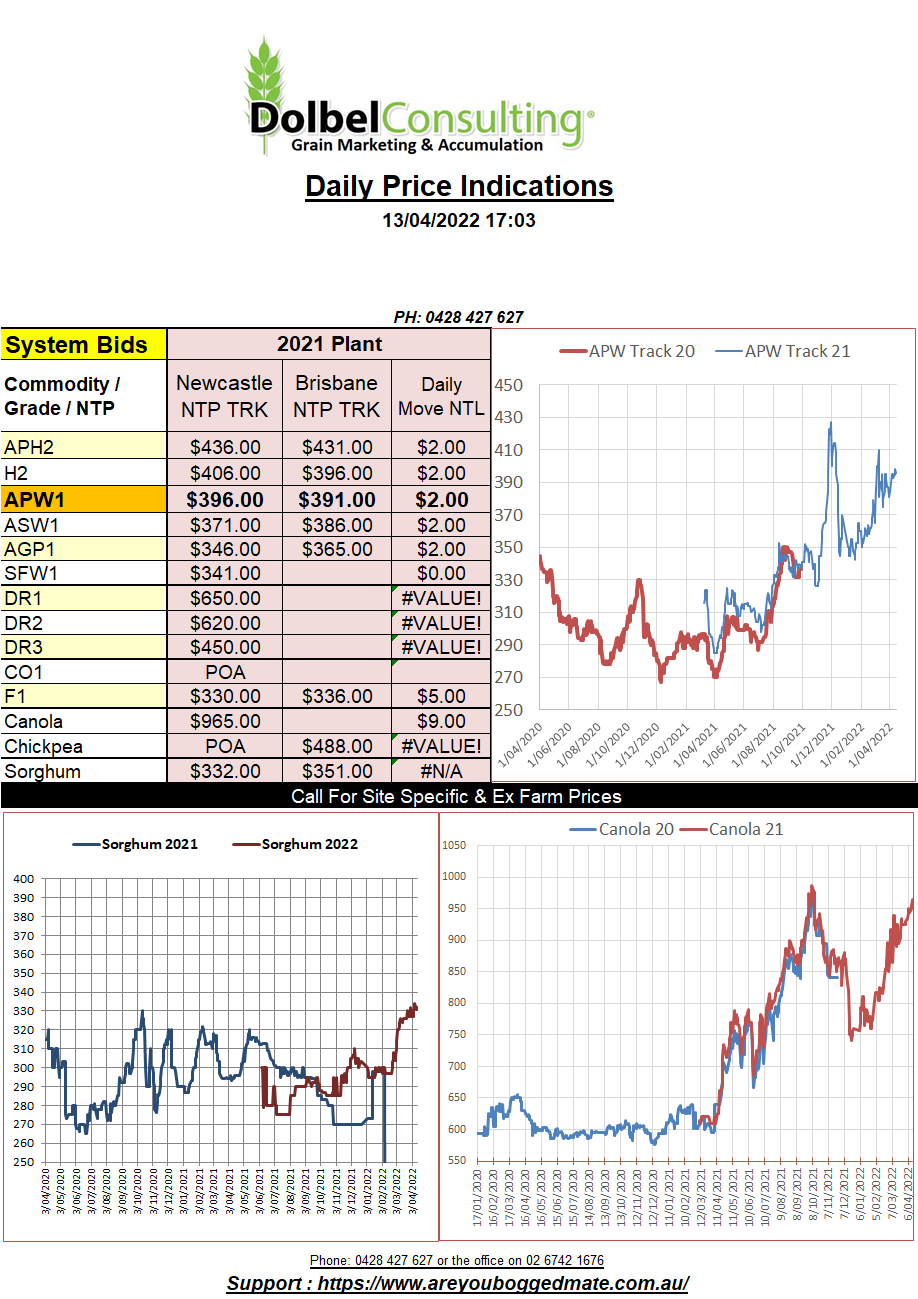

13/4/22 Prices

Hard red winter wheat futures at Chicago closed higher again. Quickly approaching values last seen prior to the sharp selloff back at the beginning of March. The jump in the AUD might take a little of the temptation away to follow US markets higher but the trades ability to make some very healthy basis profit at current cash / futures values shouldn’t hinder the move too much.

Cash values out of the USA Pacific North West followed the futures markets higher. Spring wheat and hard red winter wheat were offered higher at the port. White wheat out of the PNW also pushed higher, now priced at roughly US$443 FOB.

Using Japan as a consumer base we can convert this white wheat price to a rough comparable value here of about AUD$530 ex farm LPP. So it’s probably safe to say that US consumers / producers continue to price white wheat from the PNW out of reach of the international market. US white wheat production was sharply lower due to dry weather in the PNW last year.

Australian wheat into China continues to be the cheapest on offer by a mile. Wheat with 12.5% protein out of WA is offered C&F China at US$298.75. This compares to Russian wheat at US$441 and Argentine wheat at US$515 C&F. Using current HRWW cash bids out of the PNW of the USA into China the US product would be roughly US$510 C&F China. Why Aussie wheat is so cheap when compared to alternative supplies is hard to determine.

Egypt is looking for wheat again after scrapping their last two tenders. The trade are talking about the regular tender system being modified or abandoned as Egypt continues to look for an alternatives to traditional Black Sea supplies. Offers are expected to come from many EU nations, India, Romania and potentially Russia. Current stocks in Egypt will last about 140 days (consume 19mtpa) but their harvest (10mt) will start around the beginning of May.