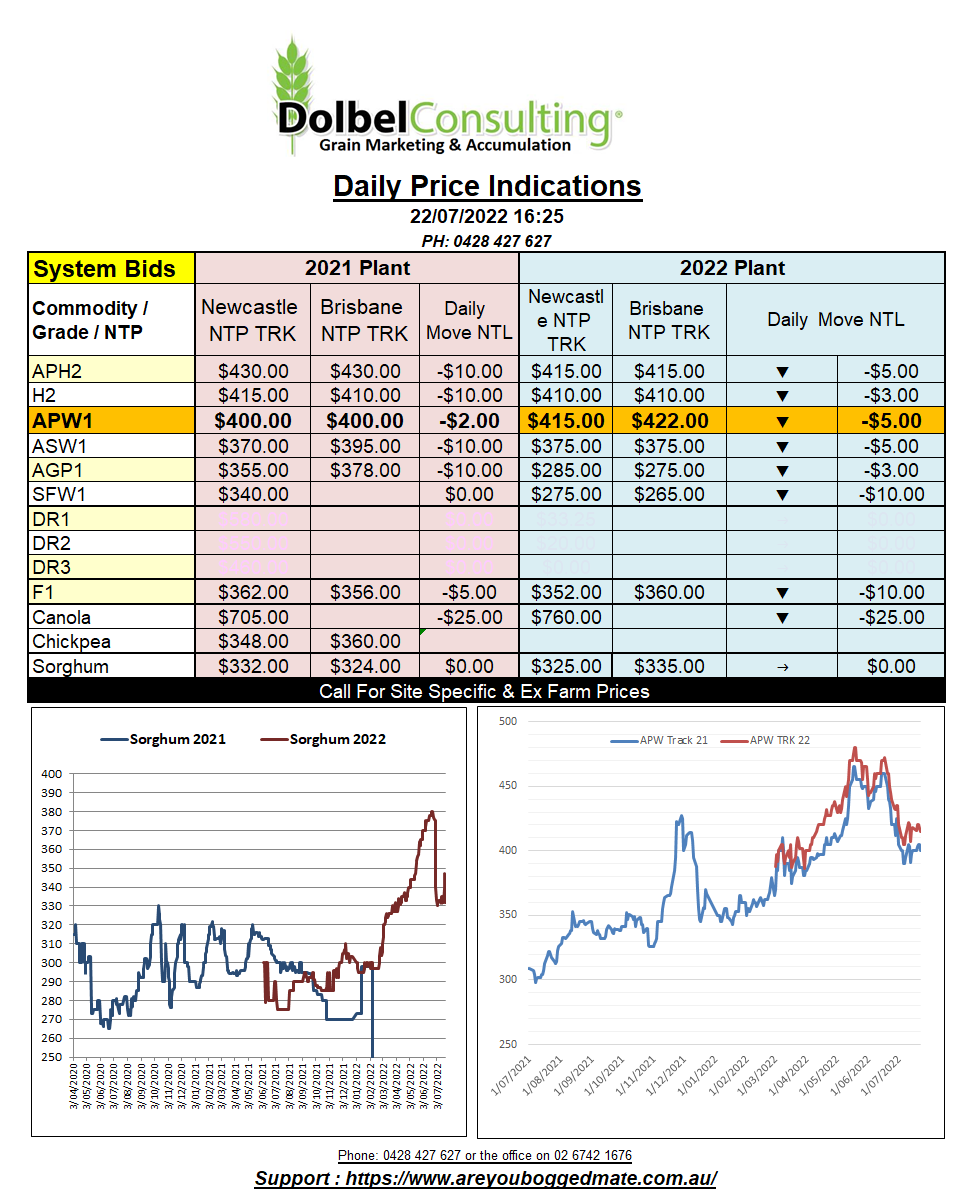

22/7/22 Prices

Soybeans were the biggest loser at Chicago overnight despite the handy US export volume reported. US soybean futures appear torn between reflecting the volume of recent sales and the expected increase in Chinese demand as the hog herd increases, and the increased competition from the S.American suppliers, the weaker Brazilian real making their product much more attractive. The EU also booked some beans off Brazil, confirming their product is still some US$20 cheaper than the US product. Even with ocean rates from the US gulf to China falling and the rates from Brazil to China increasing a smidge. US beans will still need to fall further to become competitive into the Asian / EU market again.

The softer Chicago soybean market continues to pressure both ICE canola and Paris rapeseed futures, both falling considerably overnight. The Paris new crop Feb 23 rapeseed contract slipped AUD$22.85 per tonne while Winnipeg canola future for the January slot, when considering changes to the AUD/CAD, closed back AUD$30.75. This week we have seen Paris rapeseed for the February slot shed AUD$69.

Chicago wheat futures were lower, spill over selling from both the soybean and corn markets not helping. Generally, the fundamentals for wheat were pretty good. Better US export sales volume and the IGC pulled wheat production back 7.9mt over last month’s guestimate. The IGC reduction was significant actually, if it hadn’t of been during the middle of harvest one may have expected the market to have taken a lot more notice. Last month the IGC pegged all wheat production at 781mt, this month 769.3mt. An increase in carry in and a decrease in consumption takes the shine off the number a bit but the net result is still a yearly 9.5mt decrease in ending stocks, and that is what we need to see.

Insurers seem to be the biggest hurdle when considering a Black Sea export corridor, regardless of being guided, something about sea mines is scary.