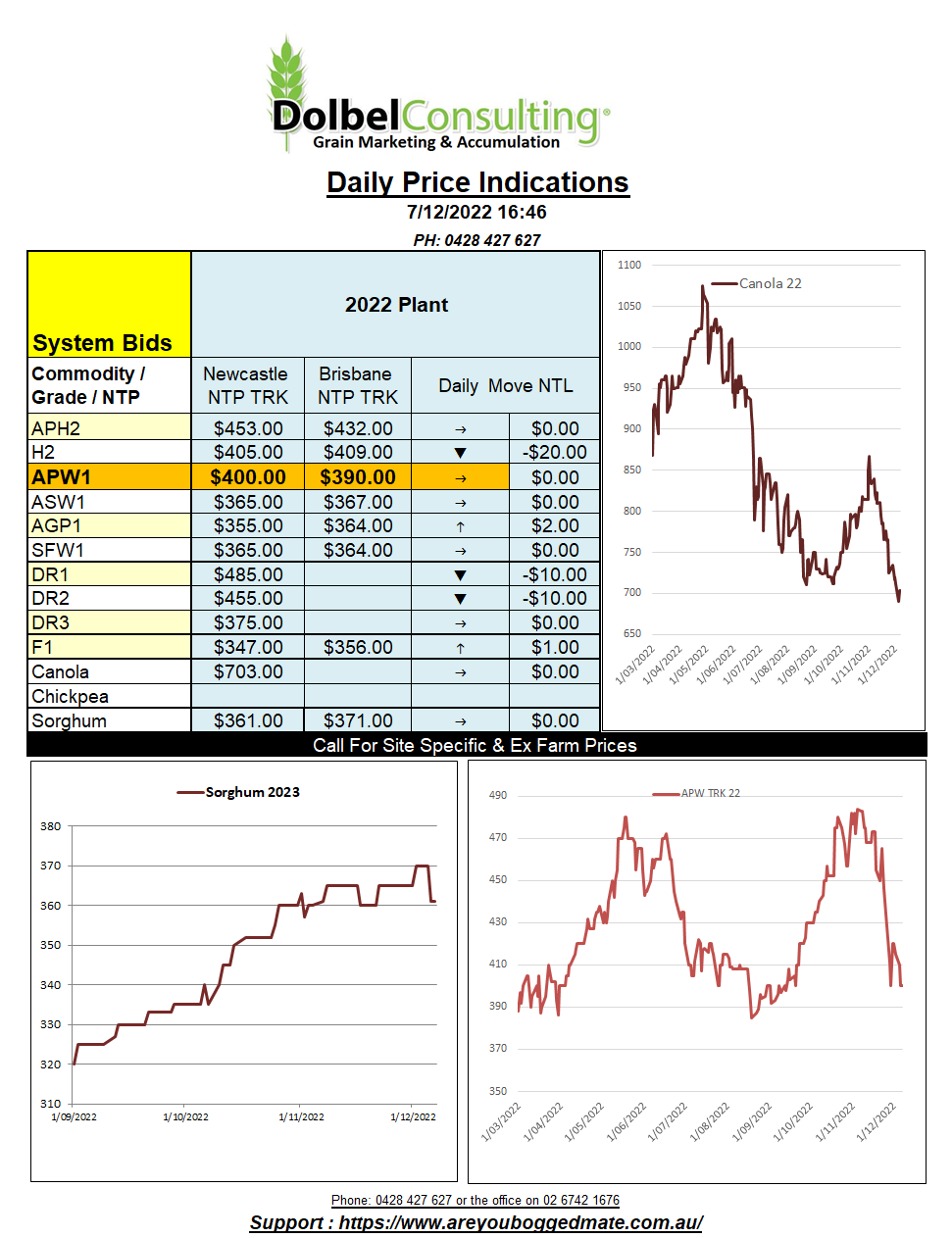

7/12/22 Prices

Reading the wires there are still two camps in the wheat market, those that think wheat will continue to fall as the world slips into a recession after the interest rate hikes “do their job” of curtailing “supply” driven inflation. I’m still a little confused about that policy, but anyway.

Then there is the camp that is firmly entrenched in the “wheat is cheap, why does it keep falling” opinion.

It’s pretty obvious who has been on the right side of the ledger up until now. Chicago SRWW futures have fallen 197c/bu, that’s about AUD$108 per tonne at today’s money, since Nov 1st. During that same time frame Aussie APW1 on the track at Newcastle has fallen AUD$77, that’s handed back AUD$31 worth of CME basis and Australian wheat is still cheaper into Asian markets. When you look at the 950kt of wheat sold into Pakistan earlier in the week you can also conclude that Aussie wheat is cheap enough to work into just about any end user market around the world. US wheat, cannot, does this indicate that there is still potential downside in US futures, probably, but does also indicate that there is probably just as much potential upside in Aussie basis to US futures. If our wheat is already more than competitive into Asian and Middle East markets, than in theory at least, why should it fall further unless European values and Black Sea values fall further. Which brings us to look at the recent fall of the MATIF (Paris) milling wheat futures contract. The nearby December contract was back another E5.00/t last night, that’s a decline of almost E50.00 (AUD$78) since the beginning of November. Russian 11.5% milling wheat out of the Black Sea during the same time frame has fallen just US$14. Make of this what you will but it does point to a couple of plausible conclusions. One being that the futures market and the cash market is not converging or reflecting physical wheat markets, not that that is big news to many, sorry. It could also be indicating that our cash wheat market is now reflecting, much more closely, the EU products rather than the US product, is basis to Chicago becoming irrelevant or is it just a hangover from a Canadian / US drought premium at play.