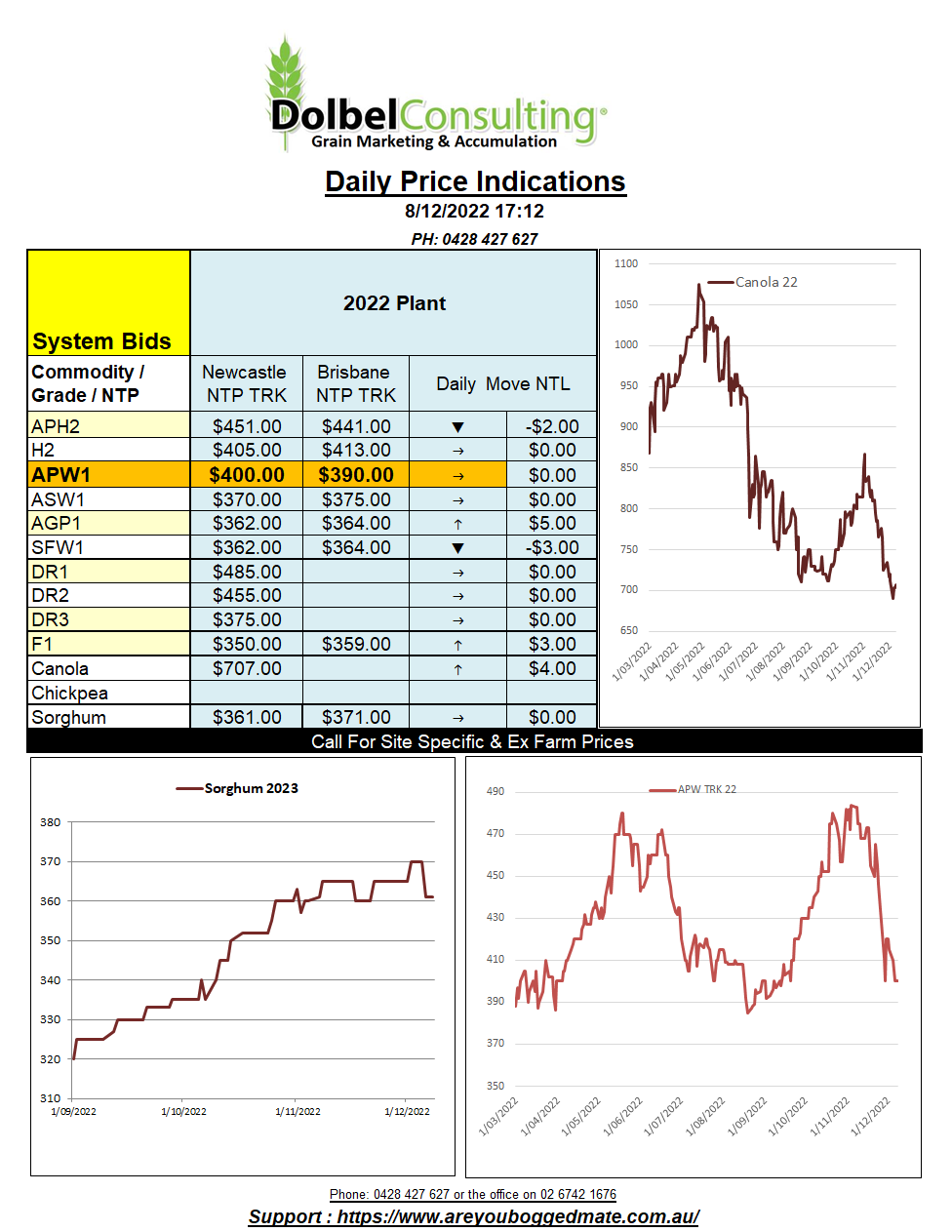

8/12/22 Prices

USDA report out Friday night. Last night’s rally may well have been technical trade ahead of the WASDE data, don’t be surprised if it’s a sell the fact kind of report. Grain markets have been pushed hard lower over the last month with little new fundamental news fuelling the sell off.

Chicago wheat futures took back this week’s losses but closed 10c/bu under Friday’s close, so don’t break out the streamers just yet. Interesting to see the nearby contract for milling wheat at Paris was back E1.25 while the March contract was higher by E5.75, outer month contracts closed higher. Paris corn and London feed wheat futures also closed higher. Paris rapeseed was not as convincing as Winnipeg. Rapeseed futures shed E0.25 on the nearby and May closed the session unchanged. Outer months gained E1.00 to E3.00. Rapeseed futures now seeing a carry through to the Nov 2023 contract. Winnipeg canola still shows a premium for the nearby contract to the March slot.

Cash prices out of SE Saskatchewan for 1CWAD13 durum wheat were firmer, gaining C$2.50 ex farm for a January lift. Cash canola bids ex farm SE Saskatchewan was also higher, reflecting the moves at the Winnipeg futures market, gaining C$14.94 for a January lift.

Hard red winter wheat out of the Pacific Northwest was higher, even with the stronger AUD the move equates to a rally of almost AUD$7.00 / tonne. White wheat cash values out of the PNW were flat, thus the stronger AUD took around AUD$3.00 from the converted price.

The punters are generally expecting to see gains in world wheat production and ending stocks in this week’s USDA World Ag Supply and Demand report. There are expectations of a higher Aussie crop, possibly being countered by a lower Argentine and Canadian crop. Generally, world wheat stocks are ok.