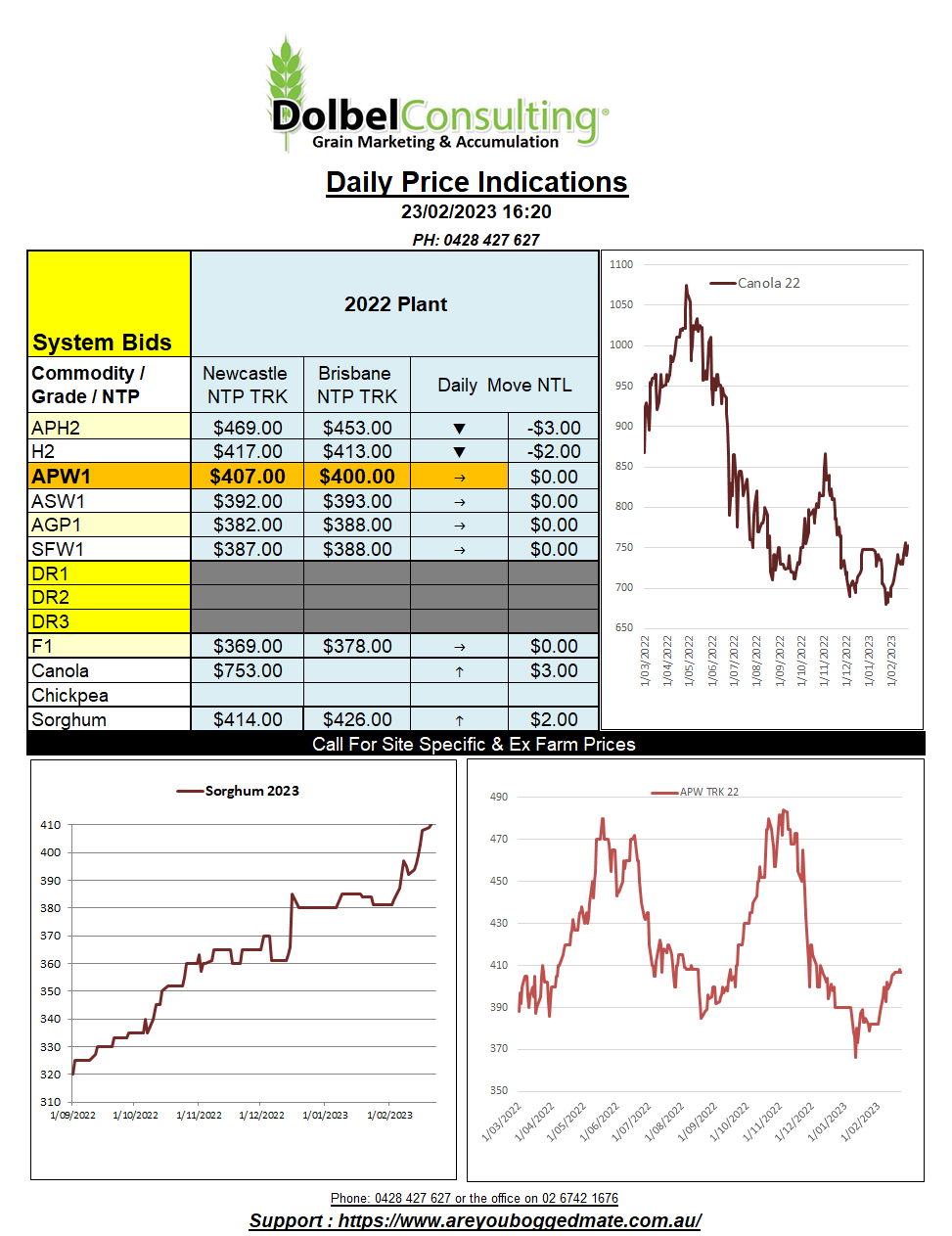

23/2/23 Prices

Conditions across the eastern parts of the US winter wheat belt are improving. The hard red winter wheat belt remains mixed, the contrast between east and west in remarkable. Reports of wind blowing cover crops away in the west opposed to conditions being all but ideal in the east. Temperatures have remained cold across the US HRW belt, thus there is currently little chance of any fields breaking dormancy early.

Chicago futures remain firmly focused on the conditions in the USA and the Black Sea conflict, the unfolding issues in S.America are having little to no impact on US futures contracts. This does not make marketing decisions any easier. The question in the back of one’s mind is, will the US futures markets respond in a surprised manner when the time is right, or will it simply move along as it has, values trending “rangebound” (800 – 850c for HRWW) as we move into the US spring in search of US fundamental impacts.

Historically speaking the price of US wheat remains high. I’ll send out an email outlining the time a value has spent in each price range taking cpi into account from 1994 later today to show you roughly where US wheat futures stand currently from a historical perspective.

Iraq is tendering to buy 200kt of milling wheat. Supply will come from the US, Canada, or Australia. Looking at current FOB values from each country for a milling grade wheat, one could assume Australia is in a good position to be cheapest offer on this tender. The US product into Iraq would, according to FOB values, cost the buyer possibly more that $150 – $200 above Australian values. Canadian wheat would also be more expensive, potentially be $100 to $120 more expensive. We’ve seen the US product make its way into some Asian markets lately, markets where it was indeed much more expensive than alternative suppliers. The wheels of progress no doubt being greased on that level playing field everyone preached about in the 90’s.