22/2/23 Prices

The market wires at the start of the US session appeared to place little importance on the frost event in Argentina. Instead choosing to concentrate on the returning heat in Argentina. As confusing as that is to anyone who follows fundamentals, either narrative is bullish ish.

I just find it amazing that the main focus was not on a mid-February frost event. I mean if there was a frost in Iowa on August 15th the market would be limit up the next day.

As it was Chicago soybean futures did close in the green, not limit up, but a 21c gain is better than a poke in the eye with a blunt stick and did create some influence over both ICE canola futures at Winnipeg and the Paris rapeseed futures contracts.

The progress of the Brazil soybean harvest is creating a lot of resistance in beans at the moment. Grower selling in Brazil has been well below previous years at this stage of harvest. This has led the trade to think that a larger than average volume will hit the market in the short term.

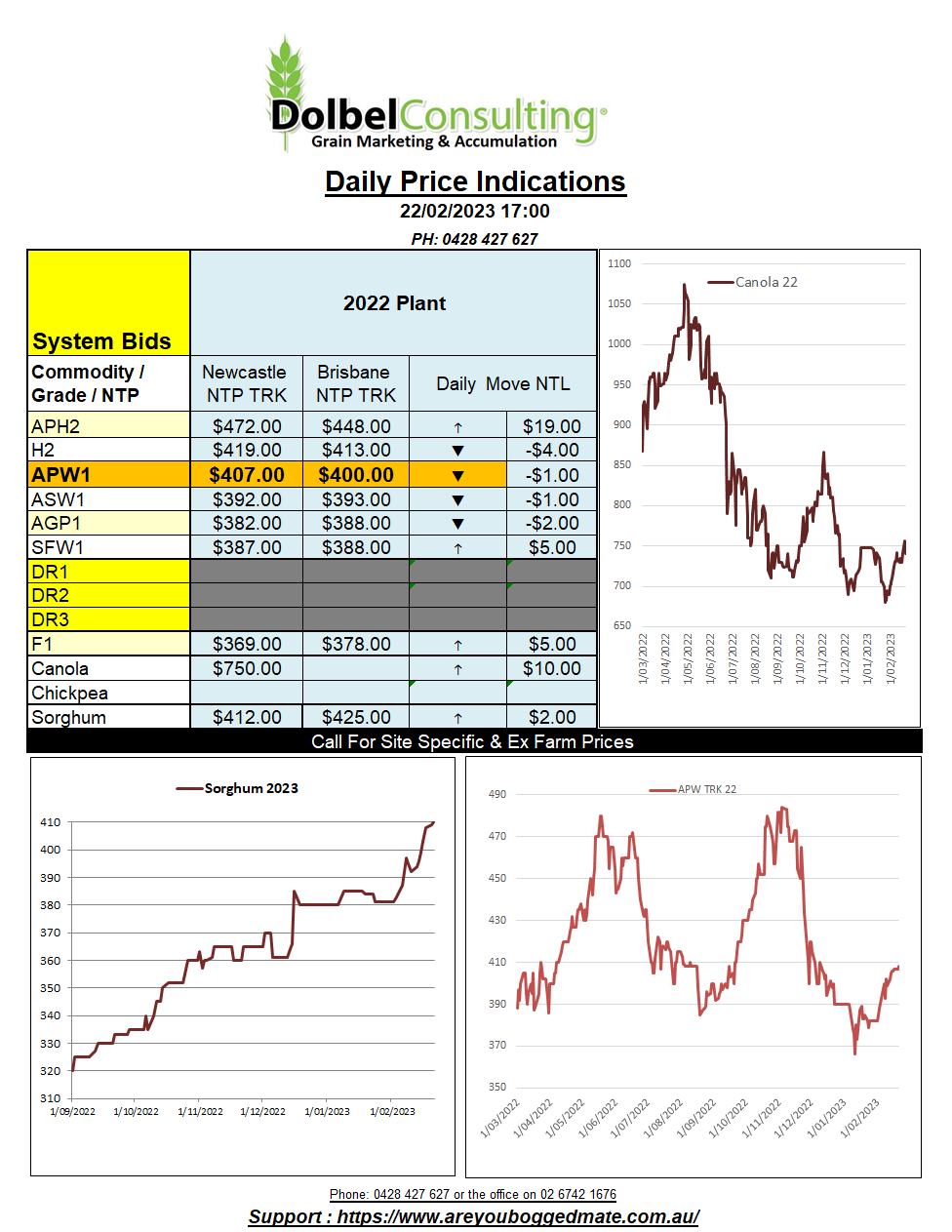

The rally in Paris rapeseed futures is worth about +AUD$10 per tonne today if basis is stable.

US wheat futures were mixed. The more active SRWW contract found selling pressure as the US dollar strengthened, triggering technical selling. HRW futures still appear to be trading on basic fundamentals and found support from, less than ideal weather, in the US HRW belt. Looking around the world winter wheat regions, and potentially spring wheat, it isn’t seeing a dream run. Conditions are cold in Russia, dry in the US, Australia, Argentina, and Canada. There is also increasing concern over soil moisture in France, Spain, Italy, the UK and West Germany. The Maghreb, N.Africa, is also suffering from drought. It’s hard to be bearish wheat at the moment even though prices remain very high by traditional standards.