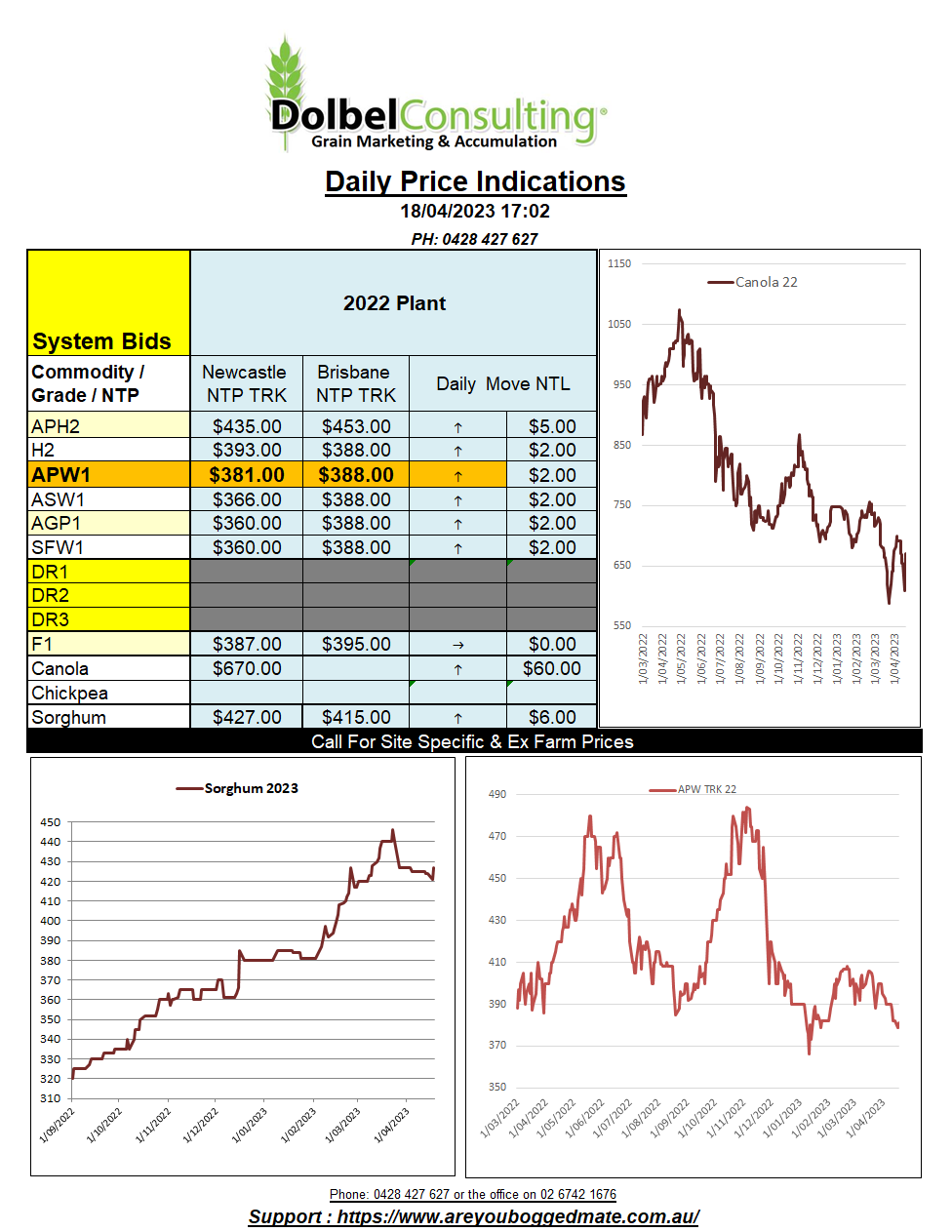

18/4/23 Prices

The international wheat market remains a moving target. The political fundamentals often changing on a daily basis. At the moment the focus is on the banning of Ukrainian wheat from entering Poland, Hungary and Slovakia.

When Ukraine was invaded the Ukraine government stopped Black Sea wheat exports. This was surprising given that during the Russian annexation of Crimea exports were not stopped.

Russian aggression around the main export hubs, the high cost of frieght insurance and access to ships were all big issues prior to the implementation of the Black Sea Grain Corridor agreement. Ukraine began to do a lot of business by road and rail into eastern Europe. The influx of cheap Ukraine grain is blamed for a sharp reduction in local values, which has made farming in the border countries unprofitable for some.

Poland’s Ag Minister recently announced that they will not bear the burden that should be spread over all of Europe. Hungary and Slovakia have now both joined Poland in their effort to sustain profitable domestic production.

Why does this push US and European wheat futures higher. There are two things happening, a reduction of grain flowing into (through) western Europe. So potentially domestic drawdown increases in those countries, and local prices improve. Then there is the restriction of export grain, reducing land-based drawdown without increased sea port throughput means exports are reduced. This is where the export corridor deal becomes more important. Russia claims they will not support an extension of the deal past the expiry of the current 60 days extension which expires late May, (unless blah, blah, blah). This adds speculation that exports may slow further. If there is Russian aggression towards ports and or ships than shipping costs will skyrocket and Ukraine will struggle to find ships to go into the war zone to load, thus reducing nearby supply, but increasing net world carry over longer term.