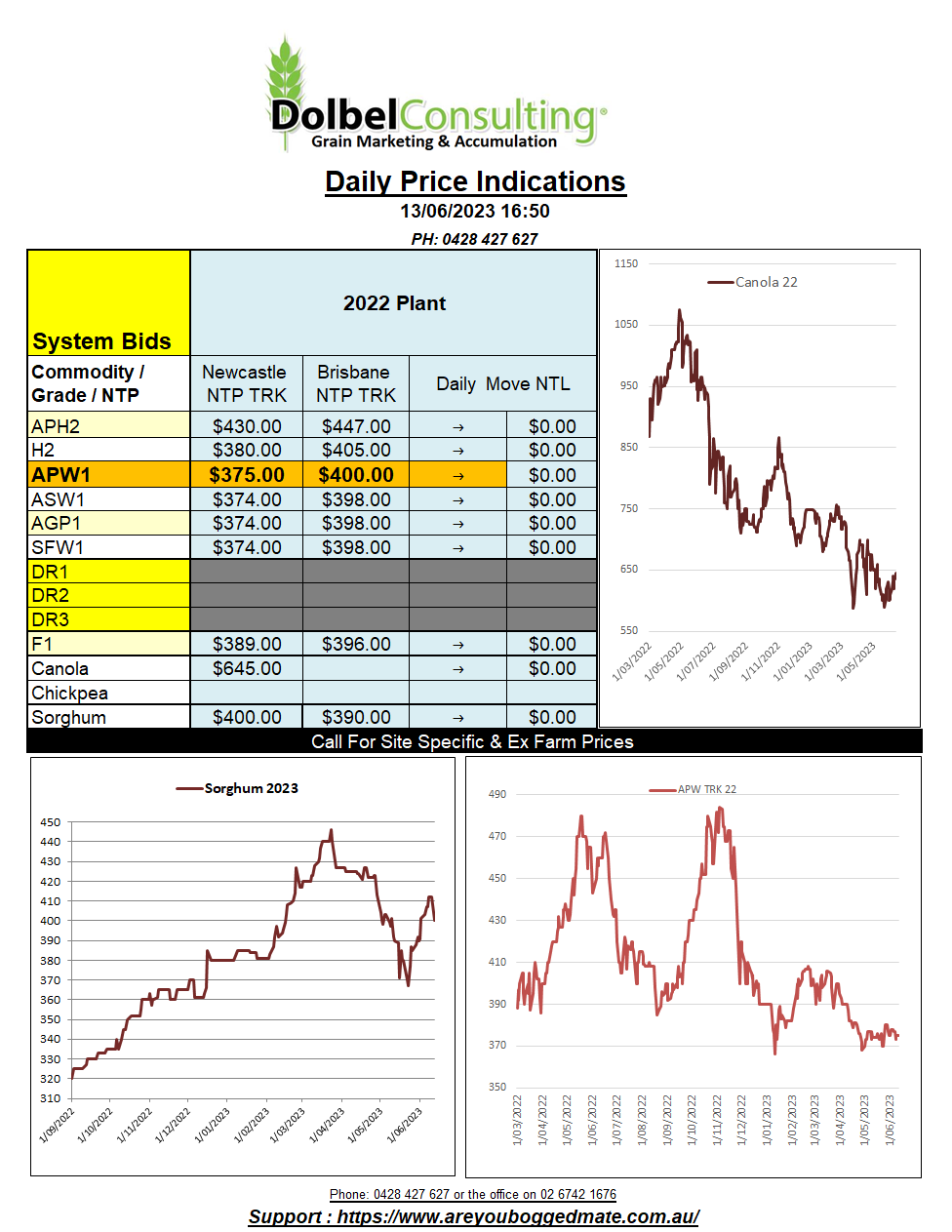

13/6/23 Prices

Tuesday Morning Comments.

A quick look at the weekly USDA crop progress report for the states shows that corn planting is almost complete now, 93% in the ground. The condition rating for corn slipped again, back 3% in the G/E rating, now at 61%.

The ten-year average G/E rating, excluding the drought year of 2012, comes in at about 66% G/E. The ten-year average yield comes in at 170bu/ac. Seeing the current G/E rating at 61% and the USDA still predicting an average yield of 181.5bu/ac does make one a little sceptical of their predictions in the most recent WASDE.

US corn futures were higher in overnight trade and should continue to push higher with this crop condition report being released after the close and potentially considered bullish. The real reason for the move higher in US corn futures continues to be the weather map. Looking at rainfall volume for the central corn belt in the states confirms that the rain that was predicted to fall over the last 7 days has not. Much of the corn belt east of Iowa remains in search of a good fall of rain. The forecast does look better though, with 15-30mm expected towards the end of the 7 days forecast period. Keep an eye on this one.

So far temperatures on the central corn belt in the US have remained mild but the mid-term forecast shows temperatures could start to push onto the mid to high 30C’s from the end of the middle of next week. Without the predicted rain, conditions could deteriorate quickly.

Wheat sowing in Argentina remains well behind the average pace for this time of year. A quick look at the rainfall stats there confirms why. Good falls in early May we not followed up. Late May, and to date June, has seen little to no rain across the major wheat regions. There is nothing in their forecast.

Saturday Morning Comments

The USDA basically delivered what the punters expected, thus will probably be discounted pretty quickly. Let’s look at wheat in this month’s WASDE.

World opening stocks were increased 380kt to 266.66mt. World production is the laughable one, increased 10.43mt to 800.19mt. I don’t know what the USDA guys put in their coffee in the morning but I’m happy to try some, on beach, near no one that will ever take me seriously again.

They managed to increase exports and demand a little to help counter the jump in supply but at the end of the day they are still projecting an ending stocks level of 270.71mt, a year-on-year increase, and an increase over the May estimate of 6.37mt. This keeps world ending stocks well above 30%, so if considered as remotely believable it will continue to put pressure on world wheat values.

Let’s drill down into some of the numbers. I’ll start with Australia, USDA estimated production at 29mt. On Friday Riverina updated their private estimate to 28.356mt, both a little high in my eyes, but you be the judge. Canada unchanged at 37mt, Argentina unchanged at 19.5mt, China unchanged, yes China, who in recent weeks has had some serious weather issues, unchanged at 140mt. The EU, increased 1.5mt, plausible maybe if their acres were out but much of northern France, Germany and Poland have seen little to no rain for the past 14 days, conditions rating there are falling not going up. Russia, well who knows, I mean their acres could be changing on a daily basis couldn’t they, Russia was increased 3.5mt to 85mt, can someone from Russia weigh in on this one. Another one that’s harder to pick than a broken nose, India, production there increased 3.5mt to 113.5mt. I don’t currently have a number for neighbouring Pakistan, which according to World Ag Weather.com is seeing some pretty heavy rain again. That must be scaring the bejezuz out of them after what happened in July / August last year.

So, my spin on the WASDE for wheat, it seems a little too optimistic and maybe the data is now out of date. Chicago and Paris wheat, flat to firmer.