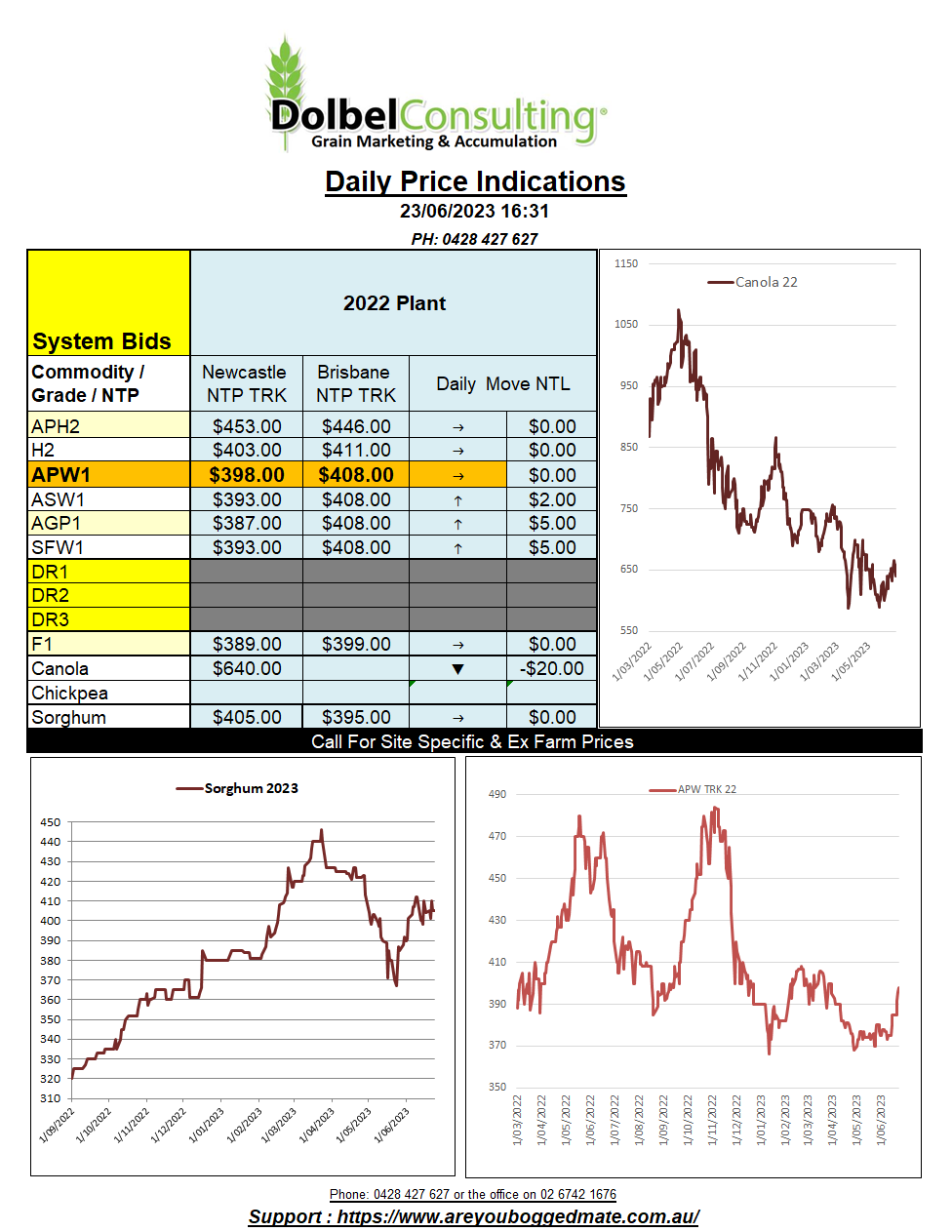

23/6/23 Prices

Corn futures at Chicago took a breather, soybean futures took it one step further and crawled off to the spare room for a nanny nap, leaving the party to the wheat punters. SRWW continued to chug a little higher, less corn potentially equals more SRWW demand, I guess. At the end of the day if the US don’t consume their SRWW at this price level they will eventually price themselves out of the export market. Hard red winter wheat futures and spring wheat futures in the US followed the SRWW market higher in an unconvincing fashion.

The correction in Chicago soybeans rolled through to selling of both Winnipeg in canola and Paris rapeseed. The Feb24 slot at Paris was hit pretty hard, shedding E11.75 per tonne. Taking the AUD/Euro into account, the day-to-day move is worth something close to AUD$16.73 downside here today given a flat basis. There was about AUD$18 worth of new crop basis given back yesterday, good to see, basis is still rubbish and still worse than it was a couple of weeks ago, but it’s good to see the trade were not tempted to push basis back out over $100 under.

Keeping one eye on the US weather forecast and it’s not looking much better for the central corn belt. Iowa should see some good falls across the north of the state towards the end of next week, but Illinois and Indiana are both forecast nothing more than some trace rain, <10mm, for the same time frame.

The spring wheat belt in the US should see some good falls over the next 7 days. It may be a case of too little too late for some, but the crop did go in late for many as fields were too cold and wet to sow early, so there’s average yield potential for many. Saskatchewan will remain mostly dry.

El Nino is on one day, off the next day, it’s almost like the fund managers are paying for the weather forecasts as well these days. The rain across eastern Australia was welcome but by no means enough for many western NSW farmers to contemplate a winter crop program for 2023.