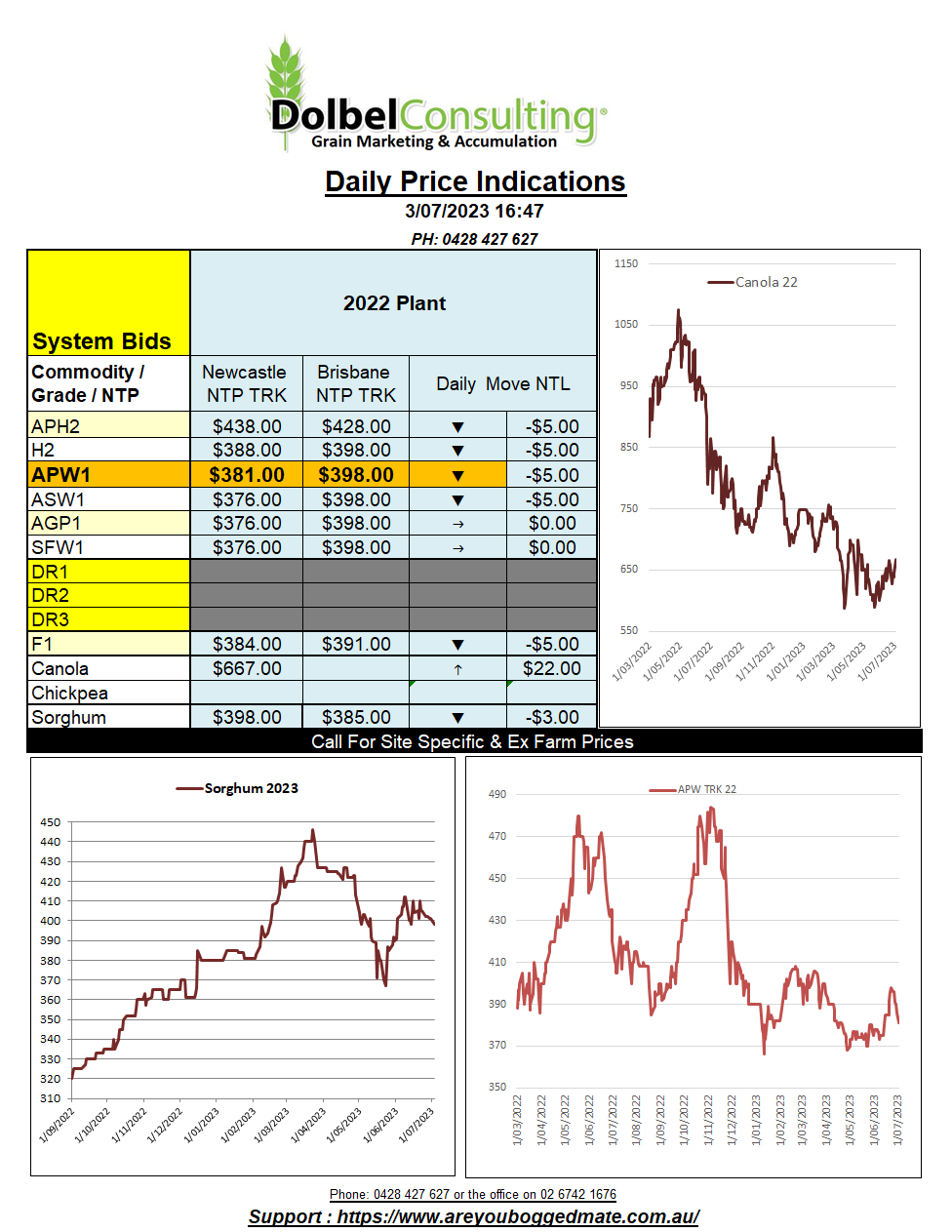

3/7/23 Prices

US grain futures again suffered through another volatile session. Data from the USDA acreage and stocks report set the tone for the session.

Wheat was lower, SRWW futures at Chicago shedding AUD$9.24, while HRWW was mixed. Spring wheat futures at Minneapolis were a tad weaker while values out the of the PNW were also lower, as were white wheat values. An increase in the value of the AUD isn’t helping the AUD conversion per tonne this morning. Weekly US wheat sales for the week ending 22/6/23 were 155.2kt, taking annual sales to 4.2mt, 21% of the USDA projected annual commitments and sales of 19.73mt. The US wheat marketing year is a June 1st > May 31st year.

The big loser was corn, and the big winner was soybeans. Corn found pressure from sown area and rain across the central corn belt. The area sown is pencilled in at 94.1 million acres, the third highest area on record. Soybean area came in below trade estimates, and also lower year on year, at 83.5 million acres. The news crushed corn futures but set a fire under the soybean market which rallied 74.25c/bu (AUD$40.96/t) in both the July and August slots. The strength in the soybeans rolled through to other oilseeds. Winnipeg canola putting on C$26.40 per tonne in the Jan 24 slot, and Paris rapeseed futures putting on E13.00 in the Feb24 slot. The increase in the AUD will hurt the conversion a little here come Monday, but we should see healthy gains in local canola bids. Are we enjoying the volatility yet ??.

Paris milling wheat futures were lower, back around E2.00 in the Dec23 slot. Black Sea values were mostly unchanged so the move in the AUD will see these locations continue to be more competitive for prompt wheat into the Asian markets, further out towards new crop, Aussie wheat remains cheap.