20/9/23 Prices

With around 80% harvested and 84mt of the Russian wheat crop in the bin, the USDA estimate at 85mt is looking a little low. The September WASDE estimate was 85mt. As far out as the USDA estimate sounds the trade appear to have factored a larger estimate of 91mt into their spreadsheets. So adjustments higher in the October WASDE may not have the impact one would assume a 5 or 6mt increase in production may have to the market.

On the other hand we have Eastern Australia to factor in. The USDA may have that one well over estimated too. With many parts of NNSW as dry or drier than in the 2019 drought, wheat crops are surviving, if that, on subsoil moisture left by spring floods in 2022, and in some locations that were lucky, heavy rain in March 2023. There are now reports of producers bailing winter cereal crops east of Moree.

Regions generally associated with higher yields, like the Liverpool Plains are talking possible average wheat yields of 3.0t/ha or worse for wheat crops. Mix into the pot the recent frost event and we may find there are some major adjustments to be made to wheat, barley and canola for much of NSW.

Overnight Paris rapeseed futures pushed higher, putting on E6.50 in the Feb24 slot. This is opposed to the Winnipeg canola market which actually shed C$7.10 in the Jan 24 slot. The Canadian product appears to be seeing some harvest pressure at the moment.

Generally speaking cash wheat bids from the Black Sea, and the US Pacific Northwest were both lower.

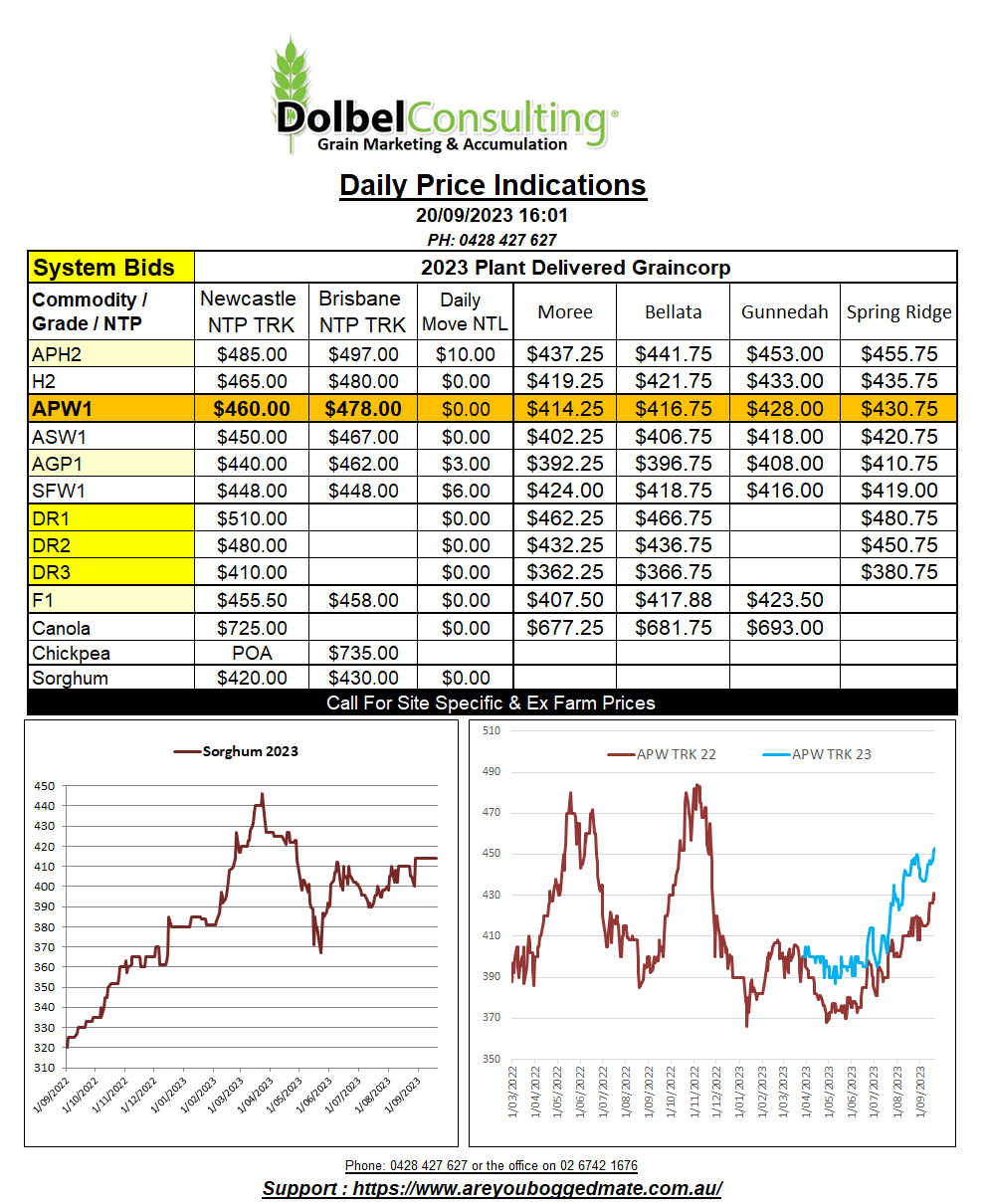

The increase in new crop Newcastle wheat values yesterday now place wheat here well above the export market.

Canadian and French durum values were relatively flat, variations more a function of currency than the cash FOB value.