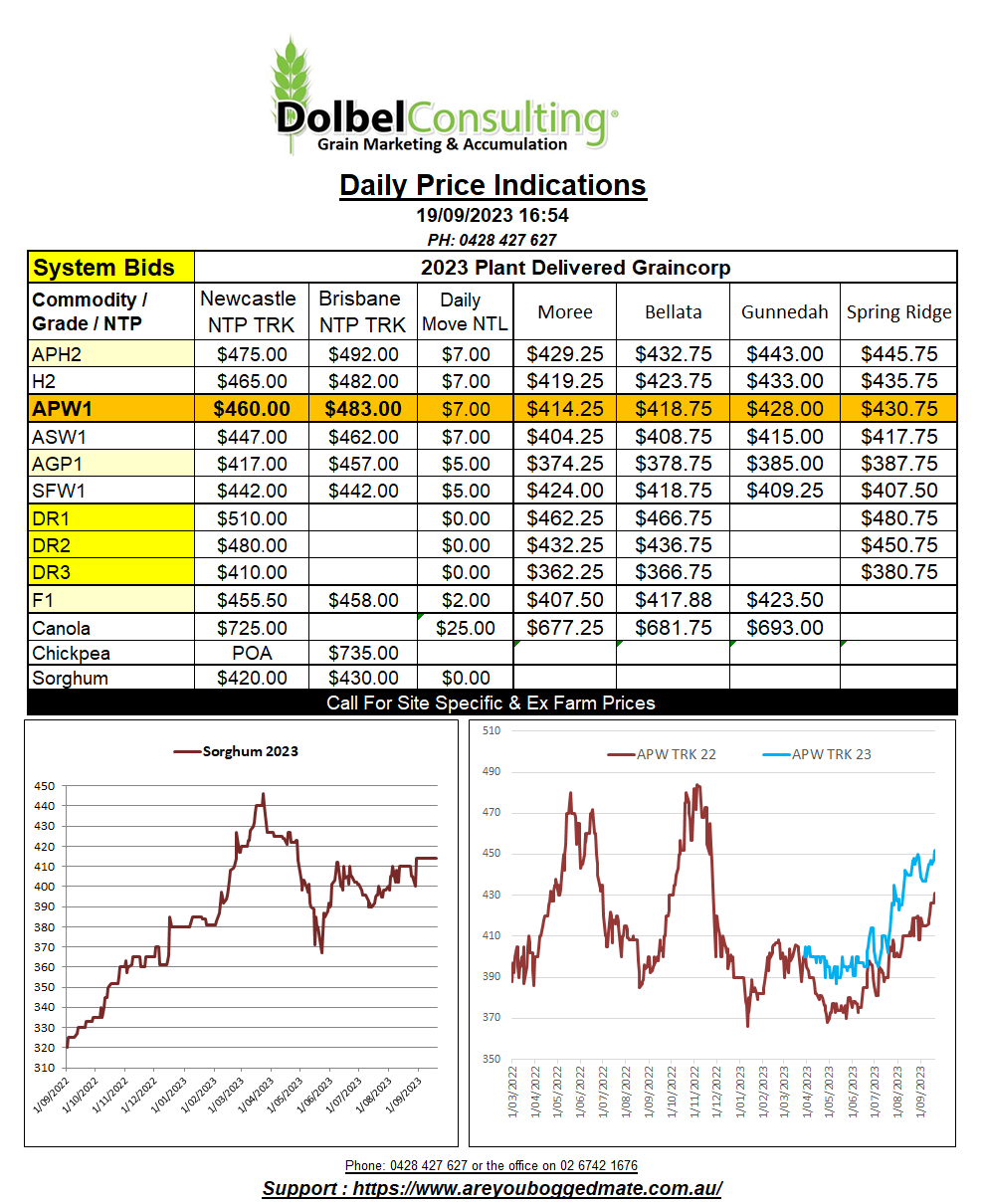

19/9/23 Prices

Domestic wheat prices in Russia continue to fall. This is mostly due to ample production, recent estimates have the Russian crop now around 91mt as opposed to the latest USDA estimate of just 85mt. The other problem is logistics, exports are expected to top out at 49mt. Port capability is now the major bottleneck in getting Russian wheat ending stocks lower. This has lead some analyst to suggest Black Sea values are probably about as low as they expect them to go in the short term. Some expect lower domestic prices leading to higher margins for traders out of the Black Sea.

Comparing Russian milling wheat to Australian milling wheat off the east coast into the Asian market, it is very apparent that east coast Aussie wheat is now some AUD$75 above the Black Sea alternative. When compared to other major exporters (bar Ukraine) this is not necessarily the case but is starting to be much more common. For instance HRWW out of the US Pacific Northwest is now closer to AUD$45 cheaper when using Asia as a consumer base. Other major exporters like France, Argentina, the USA and Canadian spring wheat’s, are all much closer in value than one would imagine given the current weather conditions on the east coast of Australia.

The severity of the drought across NNSW and SQLD has probably been overshadowed somewhat by the stellar season experienced, up until recent frosts, across the south and west of the continent. For example there are parts of the Liverpool Plains that have seen just 200mm of rain this year, this is comparable to the 1-100 year drought experienced a couple of years ago.

International canola and rapeseed futures were sharply lower in overnight trade. The oilseed market was lower, lead down by a fall in Chicago beans. Every rally now facing a headwind from the huge S.American supplies of soybeans. Harvest pressure is playing a role in the US, beans now 5% harvested.