19/10/23 Prices

Russia has announced a trade deal with China for the supply of corn and agricultural products worth US$26bn over the next 12 years. There’s not much detail to this announcement, but it doesn’t mention a phyto deal for wheat, so one could assume that for now Russian wheat remains off the Chinese import menu.

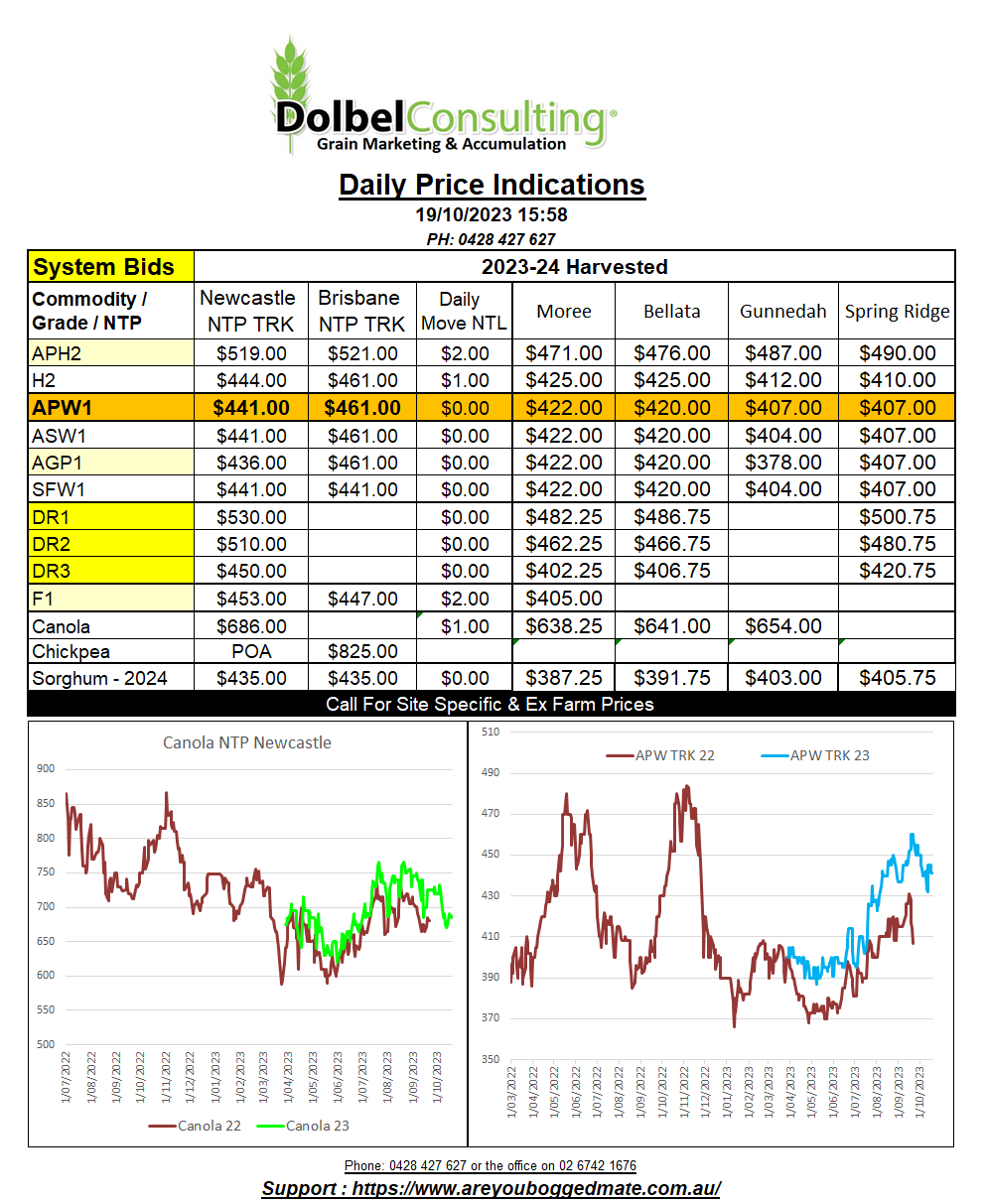

US wheat futures were higher across all grades in overnight trade. The strength in futures led to higher offer values for both US and Canadian wheat out of the Pacific Northwest, thus increasing values for US wheat into the Asian markets. Argie & French milling wheat in the <12% range is now more expensive into the Chinese market than Australian H2 wheat. US and Canadian spring wheat, more comparable to Aussie APH grade is also more expensive into the Chinese market than H2 wheat out of the Newcastle port zone. Aussie APH wheat still remains very expensive compared to other higher protein milling wheat, but quality of east Australian Prime Hard wheat in 2023 will be exceptional.

US HRWW out of the PNW remains well below the value of 11.5% wheat out of NNSW ports. According to the bid / offer platform, CLEAR Grain, the farmer offer to sell H2 out of Geraldton in WA is roughly $460 – $470, that’s even higher than the current port bid here in Newcastle of $443.

Paris rapeseed futures closed higher, the punters appear to be liquidating some short positions both on Paris rapeseed and in Chicago soybeans. Not so in Winnipeg canola though. The move in Paris Feb24 rapeseed futures was E3.50 higher. Taking that move and the move lower in the AUD into account, in theory the move equates to plausible upside here of about AUD$6.31. With the basis to Winnipeg at about $150 under, there’s little reason why Australian markets should reflect a move at Winnipeg. Aussie product is more than cheaper than Canadian canola at the export level already.