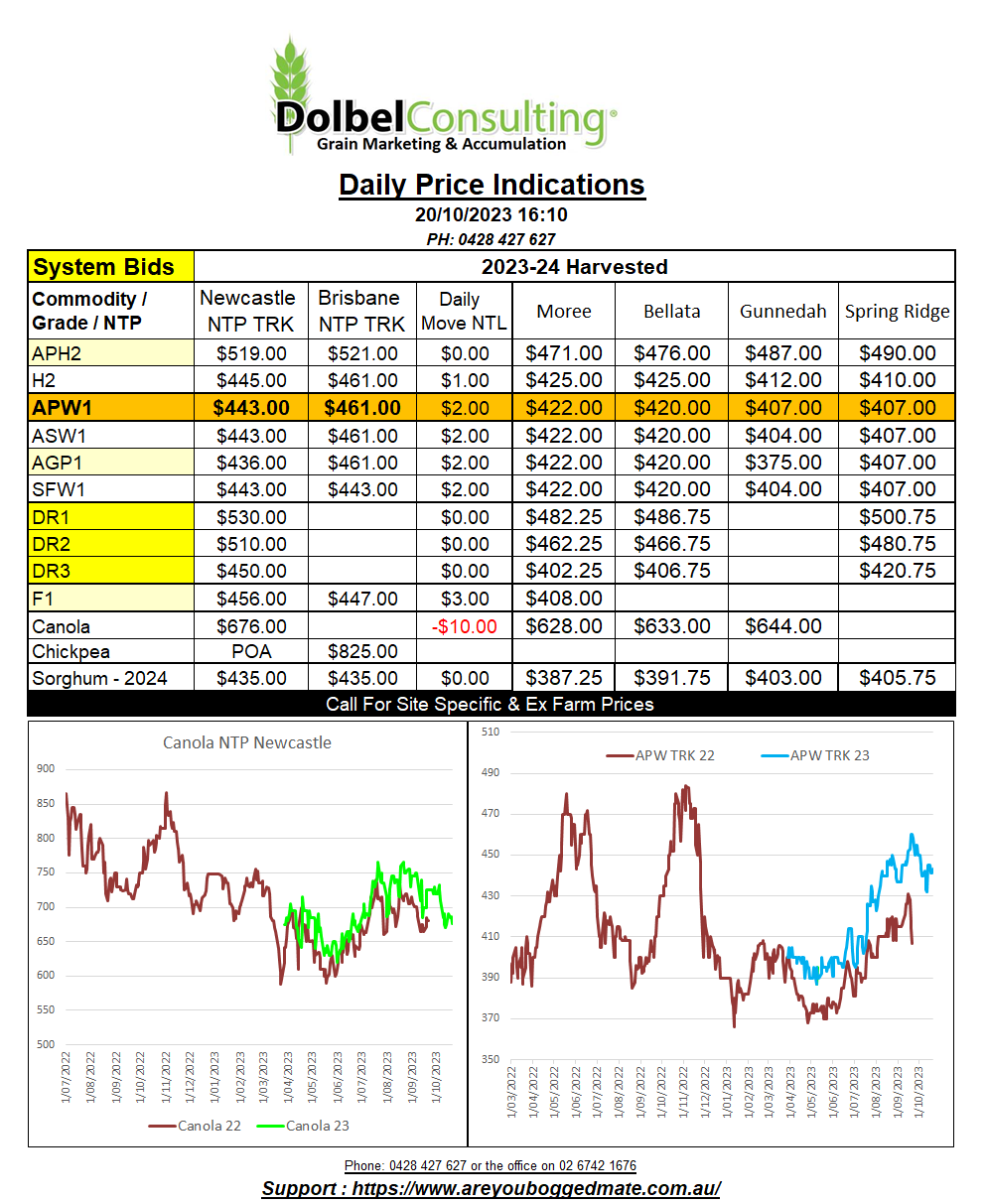

20/10/23 Prices

Both Winnipeg canola and Paris rapeseed were hit pretty hard last night. The weaker AUD against the Euro will limit losses on the conversion somewhat but there is still an equivalent downside of just over AUD$8.00 potentially.

World vegeoil prices were lower, dragging oilseeds like canola and rapeseed lower, although Chicago soybeans did manage to fend of the weakness to close relatively unchanged. Chicago soyoil was lower, Malaysian palm oil was lower. The market also broke away from crude oil which closed a little higher, still a little skittish over the Israel / Hamas conflict and its regional implications.

The International Grains Council had a stab at the numbers in the monthly report. Without paying a subscription fee of US$1650 details right now are limited, I’ll wait for further private analysis of this report. Basically the summary appears to point towards lower world canola production year on year but an increase in exports from the Black Sea.

Current FOB values from other major exporters like Canada and France suggest Australian values are already much lower than their offerings into Asian markets, but could be too expensive to move into the EU markets at current values. Ukraine offerings into China appear to be on par with Aussie values or just a little lower. This would also mean the Ukraine rapeseed would also be cheaper into the EU market than Australian canola, potentially by as much as US$50 but the cost of execution from Ukraine is somewhat….rubbery.

The IGC production number for wheat was a little higher month on month, pegged at 785mt +2mt. Trade and consumption were both 1mt higher thus countering the high production & leaving carry over at 263mt world wide. Major exporter wheat ending stocks were called 56mt, up 1mt on Sept but 9mt lower than last year. The IGC soybean data wasn’t overly bearish month on month but year on year there’s still an increase of 7mt in carry over stocks.